Technical box extracted from:

Inflation Report no.4, November 2013

In 2010, to ensure its basic objective of maintaining and ensuring price stability, the NBM began to set quantitative targets for annual inflation, which was a necessary precondition of transition to the inflation targeting regime. Thus, according to the monetary policy strategy of the National Bank of Moldova for 2010-2012, for 2010 it aimed to steer inflation to the level of 5.0 percent with a possible deviation of ± 1.0 percentage points. In the period 2011 - 2012, NBM aimed to ensure the inflation rate within the mid-single digit range. The actual transition to the regime of direct inflation targeting came with the publication of the Medium-term monetary policy strategy (approved by Decision of the Council of Administration no.303 of December 27, 2012). According to this strategy, NBM sets its inflation target of 5.0 percent annually, calculated based on the consumer price index, with a possible deviation of ± 1.5 percentage points.

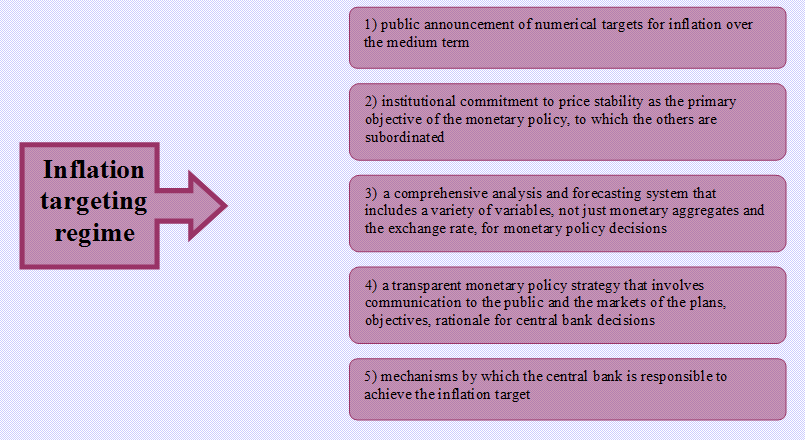

Inflation targeting is a monetary policy regime that involves five main elements:

In other words, inflation targeting does not only mean communication to the public of numerical values of inflation for the next year. The efficiency of such a monetary policy strategy is determined by the existence of the other four criteria and the assurance of their sustainability.

Thus, besides the fact that the numerical value of the medium-term inflation is communicated in the monetary policy strategy for the medium term, the other aforementioned elements are also met in the Republic of Moldova. The institutional commitment to ensure price stability is provided by the amendments to the Law on the National Bank of Moldova made in 2006. At the same time, the NBM has developed a comprehensive system of analysis and forecast of key macroeconomic variables in the short and medium term that includes a suite of techniques and econometric models and a dynamic general equilibrium model which are continuously re-estimated and recalibrated. The transparency criterion is ensured by publishing monthly releases on monetary policy decisions, press conferences and quarterly inflation reports showing the inflation evolution and forecast in the Republic of Moldova. At the same time, the NBM explains in its reports the main factors that determine the actual inflation deviation from the forecast, showing its accountability for the undertaken commitment.

The adoption of this strategy can be justified by the advantages it possesses compared to targeting the exchange rate or monetary aggregates. Thus, inflation targeting enables monetary policy to focus on domestic situation and react to both external and domestic shocks. Inflation targeting enables the monetary authority to make use of all the information, not just the information contained in several indicators, to determine the time and intensity of its actions. At the same time, the monetary policy regime has the advantage of being easier to understand by the public and, thus, being more transparent.

|

|

Year of adoption of the inflation targeting regime

|

The inflation target for 2012, %

|

Average inflation

in 2012, %

|

|

Moldova

|

2010establishment of the quantitative inflation target/2013

|

5.0 ±1.5 percentage points

|

4.6

|

|

Romania

|

2005

|

3.0 ±1.0 percentage points

|

3.33

|

|

Czech Republic

|

1997

|

2.0 ±1.0 percentage points

|

3.3

|

|

Poland

|

1998

|

2.5 ±1.5 percentage points

|

3.7

|

|

Hungary

|

2001

|

3.0

|

5.7

|

Although NBM has recently switched to this monetary policy regime and has less experience than other countries in the region (see table), it has managed to develop the main elements of this regime and through its instruments to direct the inflation towards its target in the medium term. Thus, in the last three years, the NBM managed to ensure the disinflation trajectory of the annual CPI rate, so that starting with February 2012 until now, it always has fallen within the range of ± 1.5 percentage points from the target of 5.0 percent as stipulated in the Medium-term monetary policy strategy.