Technical box extracted from:

Inflation Report no.2, May 2013

Yield curves play an important role, both theoretical and practical, in determining the interest rate’s level.

The yield curve is a continuous curve, which describes the functional relationship between yield to maturity and the number of years that occur before maturity for fixed-income securities at a given moment. Equal claims from other points of view (repayment risk, liquidity risk, purchase price, etc.) are also included and represented. Although the yield curves are limited only to certain claims, these are also significant for the entire credit market.

In the U.S. the subject to such representations is the treasury bills, while in the Republic of Moldova - state securities.

According to the current conjuncture, yield curves can have three ways of expression:

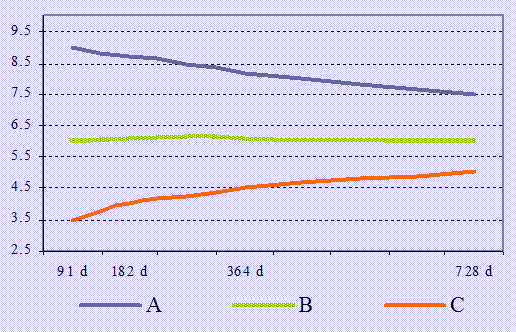

The Flat Yield Curve indicates that the bond yields on short, medium and long term are practically the same and therefore the relationship between supply and demand is balanced on the whole market (Chart no.1, curve B).

The Upward-Sloping Yield Curve shows that long-term securities have a high yield and suggests that the demand for short-term funds is very strong (relative to supply) compared to demand for long-term funds (Chart no.1, curve C).

The Downward-Sloping Yield Curve shows that the short-term securities have a very high yield, which means that the demand for long-term funds is very strong (relative to supply) compared to the demand for short-term funds (Chart no.1, curve A).

For the explanation of the yield curve configurations there were submitted three hypotheses:

-

The liquidity preference hypothesis is explained by the fact that investors give priority to liquidity, or to the ability to quickly convert assets into cash without losses. Since short-term securities are relatively more liquid than long-term securities, they will have a higher price and, therefore, a lower yield than long-term securities. This hypothesis does not take into account the medium and long-term interests of investors, interests that have as orientation the perpetuation of the placement with maximum yield criterion.

-

The segmentation hypothesis contends that there are separate markets for fixed income securities with short, medium and long term and that supply and demand determine the level of yield on each market. Thus, the curve can take various aspects, depending on the yield of the market.

-

The expectations hypothesis states that the investors' expectations regarding the evolution of the interest rate determine the relationship between the yields on short and long term. If investors expect the short-term interest rate to increase, the yield curve will be sloped upward, if the investors expect the short-term interest rate to decrease, the yield curve will be sloped downward and if the investors expect the short-term interest rate to remain at the same level, the yield curve will be flat. This hypothesis does not allow market segmentation, all securities are considered interchangeable. The facts, however, indicate otherwise. There are investors mainly for short-term securities (commercial banks) and other investors specialized in long-term securities (insurance companies).

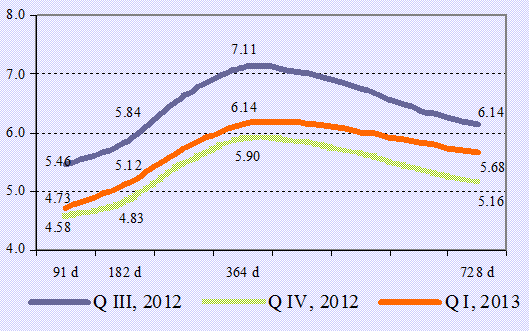

In the Republic of Moldova (Chart no.2), the SS yield curve has a convex shape, which shows that the yields for these maturities are higher. This occurs due to the fact that the state securities market is segmented according to the preferences of investors. Most of them are licensed banks that prefer to invest in SS with lower maturity, which are considered to be more liquid, but also the Ministry of Finance’s offer is mostly oriented towards treasury bills.

Typically, at an auction per month, licensed banks purchase government bonds with a maturity of two years, but both the offer of the Ministry of Finance and the demand are much smaller than for the treasury bills. Thus, the market is segmented as follows: the first segment - treasury bills from 91 days to 364 days and the second segment - government bonds with a maturity of two years. The volume traded on these segments differs, the first segment - about 99.0 percent of all transactions in the securities market, while the volume of bonds with maturity of 2 years - 1.0 percent of the total. In addition, interest rates on bonds of 2 years can be explained by the expectations hypothesis. Most likely, the investors expect a decrease in interest and inflation for this type of SS.

Chart no. 1. The yield curve types

Chart no. 2. The SS yield curve in the Republic of Moldova