Добро пожаловать на официальный сайт Национального банка Молдовы!

×

У вас хорошее зрение, и вы хотите отключить этот инструмент?

Добро пожаловать на официальный сайт Национального банка Молдовы!

Вы можете выбрать один из наиболее востребованных отчетов из списка:

Национальный банк и члены его руководящих органов независимы в осуществлении своих функций, установленных настоящим законом, и не могут обращаться за указаниями и получать таковые от органов публичной власти или какого-либо иного органа.

Стратегия денежной политики НБМ на среднесрочный период предусматривает поддержание количественного объектива инфляции на уровне 5.0% с возможным отклонением ± 1.5 процентных пункта – оптимальный уровень для устойчивого экономического роста и развития Республики Молдова на среднесрочный период.

Национальный банк обладает исключительным правом эмиссии на территории Республики Молдова банкнот и монет в качестве платежного средства.

Национальный банк обладает исключительным правом лицензирования, осуществления надзора и регулирования деятельности финансовых учреждений.

Национальный банк имеет право покупать, продавать и негоциировать иностранную валюту, используя активы, покупать и продавать казначейские обязательства и другие ценные бумаги, выпущенные или гарантированные правительствами иностранных государств и международными финансовыми публичными организациями.

Национальный банк осуществляет надзор за системой платежей в республике и способствует стабильному и эффективному функционированию автоматизированной системы межбанковских платежей.

Национальный банк является самостоятельным публичным юридическим лицом и несет ответственность перед Парламентом.

Национальный банк информирует общественность о динамике годовой инфляции, о стратегии денежной политике, результаты макроэкономического анализа, анализа развития финансового рынка и статистическую информацию, в том числе относительно денежной массы, предоставления кредитов, платежного баланса и положения на валютном рынке.

Национальный банк проводит экономический и денежный анализ, составляет платежный баланс, международную инвестиционную позицию и разрабатывает статистику внешнего долга Республики Молдова.

Inflation Report no.2, May 2013

Due to the lack of significant resources of oil and oil refineries in the Republic of Moldova, the national economy is dependent on imports of oil derivatives, so the international oil prices fluctuations influence essentially the price developments and the pace of the national economy. The increase in commodity prices on the world market leads to higher prices on imported inputs and, therefore, on goods and services obtained on imported inputs, and could lead to the loss or restriction of markets. This determines the average fixed cost to rise and leads to the attraction of seldom used inputs into the economic circuit, new or qualitative ones, their prices being higher compared to the value of marginal productivity, due to the inefficient allocation of resources. Another consequence of the commodity price increase is the raise of taxes, fees, rents, etc., resulting in increased unit costs due to government policies. These effects are called second-round effects.

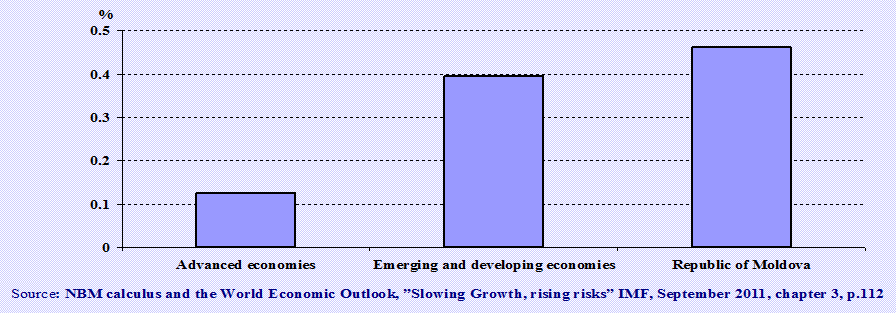

Second-round effects on core inflation are also propagated by the sharp increase in food prices on international markets, reflected in the domestic market by food prices and imports cost. According to the IMF estimates published in the “Slowing Growth, rising risks”[1] work, the impact is greater in developing countries than in advanced economies due to a higher share of food products and a reduced anchoring of inflation expectations. As for the Republic of Moldova, the estimated coefficients, based on a vector autoregression model, are similar to those of developing economies, namely the cumulative impact (until system stabilization) of a 1.0 percent shock of food prices on CPI is 0.46 percent2, while in developing countries, it hardly reaches 0.39 percent.

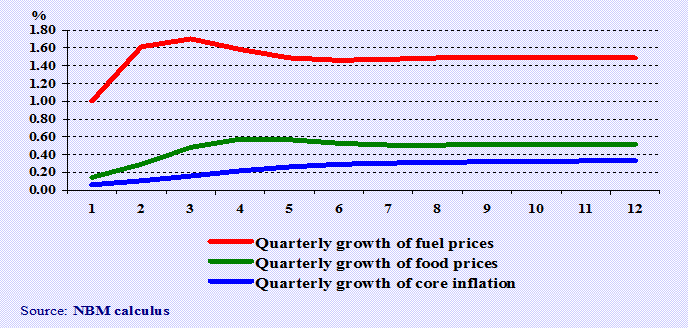

In case of fuel prices increase, the effect on core inflation growth is significant. An increase of 1.0 percent will have a cumulative impact on core inflation in the medium term of 0.33 percent. Food prices are also affected by an increase of 0.50 percentage points.

The estimation of second-round effects due to rising oil prices and food prices on international markets on core inflation are distorted as a result of the effects of intermediate variables (in particular, the nominal effective exchange rate and monetary aggregates). The appreciation of the nominal effective exchange rate would reduce, on one hand, the inflationary pressures in short term and, on the other hand, this appreciation can erode the economy’s external competitiveness, thus amplifying external imbalances. Large external imbalances increase the vulnerability of the economy to changes in investor sentiment or shocks associated with high volatility in external markets, which leads to currency depreciation and ultimately to higher inflation.

In an environment of global financial interdependence and increased uncertainty, the monetary policy regime of inflation targeting is characterized by commitment, dynamic consistency, transparency, accountability, quality evaluation, avoidance of excessive fluctuations and flexibility, a set of attributes that involves inevitably complexity. Thus, the determination and quantification of second-round effects on core inflation is essential. By alleviating these temporary effects, core inflation remains to be a part of inflation that allows trend perception and reflection of persistent sources of inflationary pressures.

[1] World Economic Outlook, ”Slowing Growth, rising risks” IMF, September 2011 chapter 3, p.112

[2] Institute of Economy, Finance and Statistics, “Economics and Sociology”, 2nd edition. 2012, p. 130