Bine ați venit pe pagină oficială a Băncii Naționale a Moldovei!

×

Ai vederea bună și dorești să închizi acest instrument?

Bine ați venit pe pagină oficială a Băncii Naționale a Moldovei!

Cele mai populare rapoarte statistice:

Banca Naţională şi membrii organelor de conducere ale acesteia sunt independenţi în exercitarea atribuţiilor stabilite de lege şi nu pot solicita şi nici accepta instrucţiuni de la autorităţile publice sau de la orice altă autoritate.

Banca Naţională informează publicul despre evoluția inflației anuale, strategia de politică monetară,rezultatele analizei macroeconomice, evoluţiei pieţei financiare şi informaţia statistică, inclusiv privind masa monetară, acordarea creditelor, balanţa de plăţi şi situaţia pieţei valutare.

Pentru asigurarea şi menţinerea stabilităţii preţurilor pe termen mediu, Banca Naţională a Moldovei menţine inflaţia (măsurată prin indicele preţurilor de consum) la nivelul de 5.0 la sută anual cu o posibilă abatere de ± 1.5 puncte procentuale, fiind considerat nivelul optim pentru creşterea şi dezvoltarea economică a Republicii Moldova pe termen mediu.

Stabilitatea financiară se realizează prin consolidarea rezilienței sistemului financiar, limitarea efectului de contagiune și diminuarea acumulării de riscuri sistemice, contribuind, astfel, la sustenabilitatea sectorului financiar și creșterea economică.

Banca Naţională a Moldovei, are dreptul exclusiv de a emite pe teritoriul Republicii Moldova bancnote şi monede metalice ca mijloc de plată. BNM pune în circulaţie bancnote şi monede metalice, prin intermediul sistemului bancar.

Banca Naţională este unica instituţie care efectuează licenţierea, supravegherea şi reglementarea activităţii instituţiilor financiare.

Banca Națională supraveghează sistemul de plăţi în Republica Moldova şi promovează funcţionarea stabilă şi eficientă a sistemului automatizat de plăţi interbancare.

Banca Naţională este o persoană juridică publică autonomă şi este responsabilă faţă de Parlament.

BNM publică statistici privind masa monetară, sectorul bancar, balanța de plăți, situația pieței valutare, etc. pentru a asigura transparența în procesul de elaborare și adoptare a deciziilor BNM, a asigura continuitatea în comunicare și predictibilitatea BNM pe piață, pentru sporirea credibilității BNM în calitate de bancă centrală dar și pe piața financiar-bancară din Republica Moldova.

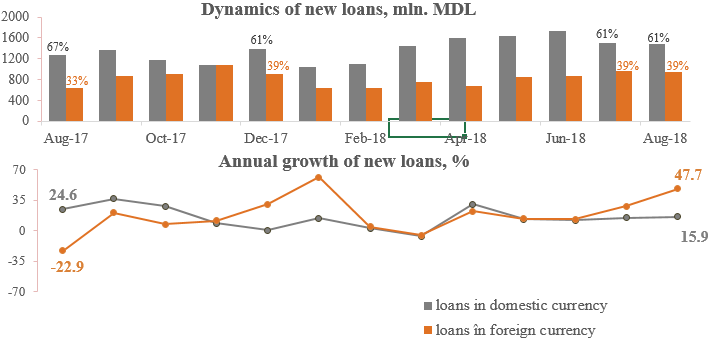

Domestic and foreign currency loans accounted for 61.0% and 39.0%, respectively, of total loans extended.

Domestic currency loans totalled MDL 1,480.7 million (-2.0% compared to the previous month and +15.9% compared to August 2017).

Foreign currency loans2, recalculated in MDL, totalled MDL 946.3 million (-2.4% compared to the previous month and +47.7% compared to August 2017).

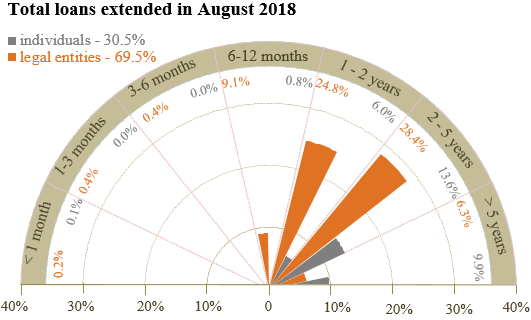

In terms of maturity, loans with maturity ranging from 2 to 5 years recorded the highest demand (42.0% of total loans extended), out of which the largest share of 28.4% was held by legal entities.

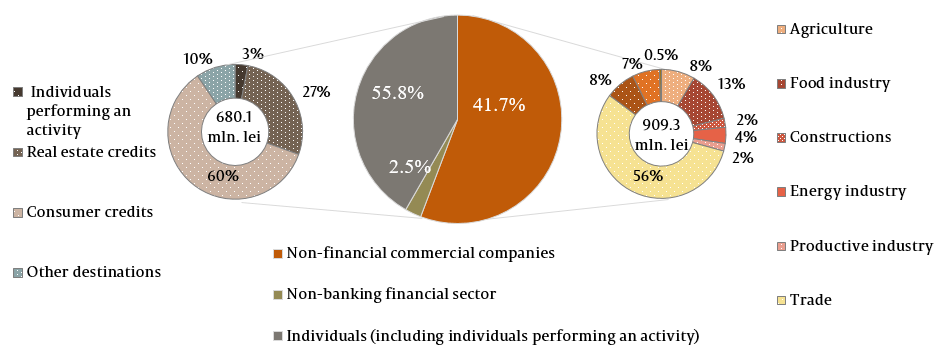

Domestic currency loans were mainly represented by individuals’ loans3 holding a share of 49.0% (consumer loans accounting for 63% of total loans), as well as loans extended to non-financial corporations, holding a share of 45.9% (of which 47% accounted for loans extended to trade companies).

Foreign currency loans were mainly extended to non-financial corporations (95.4%), of which loans extended to trade companies accounted for the largest share (60.7%).

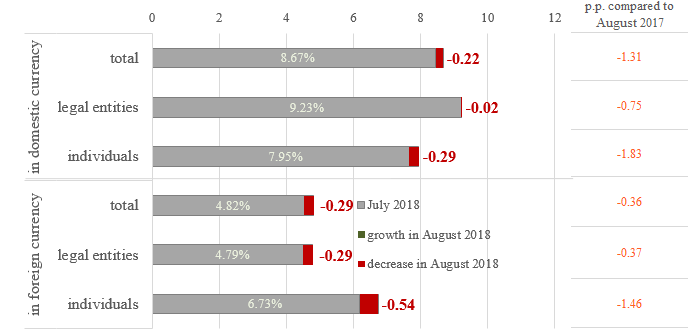

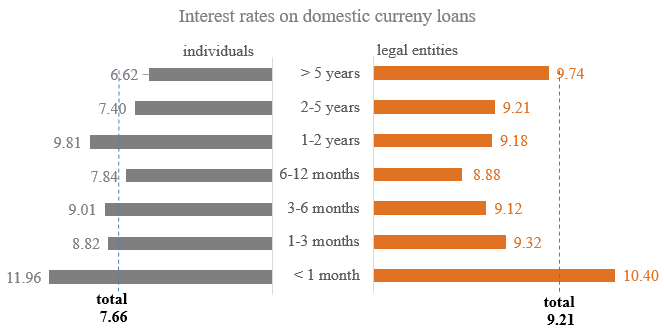

Average interest rate on domestic currency loans decreased by 0.22 pp. compared to July 2018, recording levels of 7.66% (individuals’ loans) and 9.21% (legal entities loans).

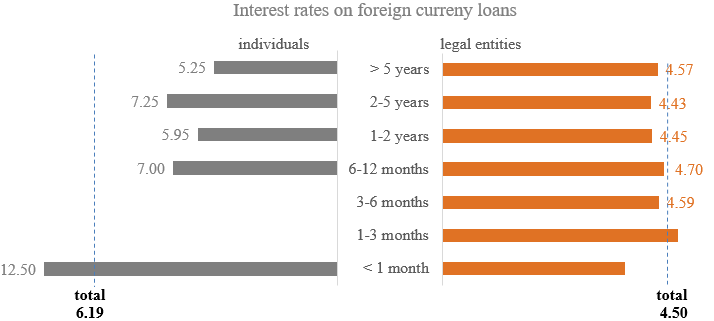

Average interest rate on foreign currency loans fell by 0.29 pp. compared to July 2018, recording levels of 6.19% (individuals’ loans) and 4.50% (legal entities loans).

Year-on-year, average interest rates on loans recorded a total decrease of 1.31 pp. (domestic currency loans) and 0.36 pp. (foreign currency loans).

Domestic currency loans with maturity ranging from 2 to 5 years recorded the highest demand in the reporting month and were extended at an average interest rate of 8.36% (9.21% on legal entities loans, 7.40% on individual’s loans).

The highest average interest rate of 11.05% was applied on loans with maturity of up to 1 month (10.40% - on legal entities loans and 11.96% - on individuals’ loans).

Foreign currency loans with maturity ranging between 1 and 2 years recorded the highest demand and were extended at an average interest rate of 4.45% (individuals’ loans – at 5.95%, legal entities loans – at 4.45%).

The highest average interest rate on foreign currency loans was applied on individuals’ loans with maturity of up to 1 month (12.50%) and legal entities loans with maturity ranging between 1 and 3 months (5.00%).

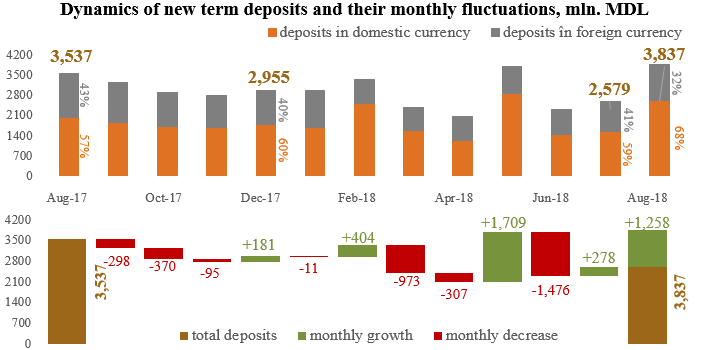

Domestic currency deposits accounted for a share of 67.6%, while foreign currency deposits – 32.4% of total deposits.

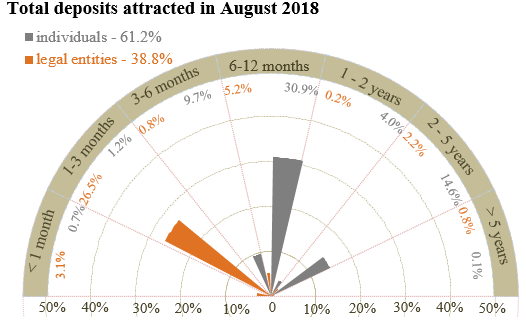

In terms of maturity, the highest demand was recorded for deposits placed for a period ranging from 6 to 12 months (36.1% of total term deposits). The largest share was held by individuals’ deposits (30.9% of total deposits placed).

In August 2018, deposits were mainly represented by individuals’ deposits – 61.2% (of which 31.0% - domestic currency deposits and 30.2% - foreign currency deposits).

Domestic currency deposits totalled MDL 2,593.0 million (+70.5% compared to July 2018 and -27.7% compared to August 2017).

Foreign currency deposits, recalculated in MDL, totalled MDL 1,244.0 million (+17.7% compared to July 2018 and -17.4% compared to August 2017)..

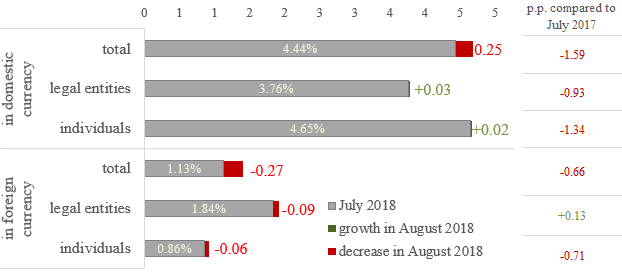

Average interest rate on new term deposits in domestic currency decreased by 0.25 pp. compared to the previous month. Individuals’ deposits were placed at an average interest rate of 4.67%, while legal entities deposits – at 3.79%.

The average interest rate on new term deposits in foreign currency fell by 0.27 pp., compared to July 2018. Individual’s deposits were placed at an average interest rate of 0.80%, while legal entities deposits – at 1.75%.

Year-on-year, average deposit interest rates decreased. Thus, average interest rate on domestic currency deposits decreased by 1.59 pp. (individuals’ deposits - by 1.34 pp., legal entities deposits - by 0.93 pp.). Average interest rate on foreign currency deposits decreased by 0.66 pp. (individuals’ deposits - by 0.71 pp., legal entities deposits - by 0.13 pp.).

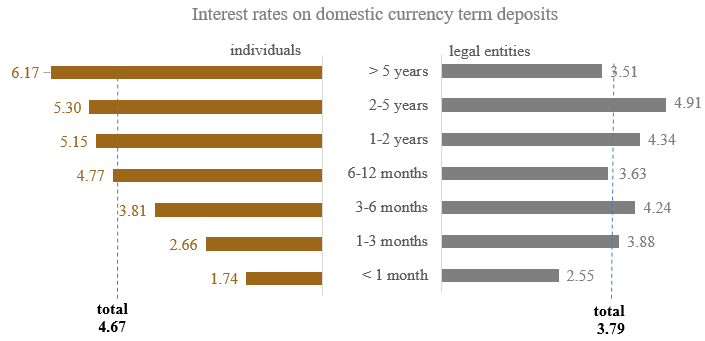

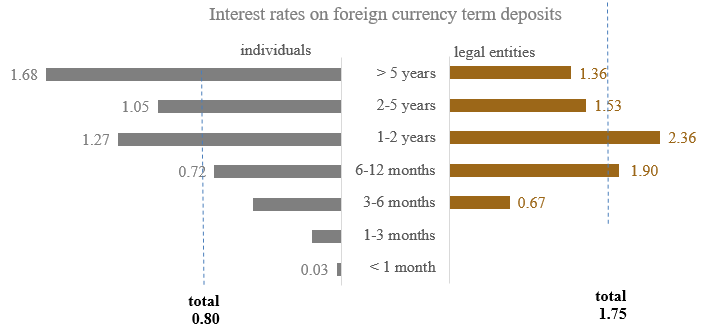

Domestic currency deposits with maturity ranging from 1 to 3 months, which recorded the highest demand in the reporting period, were placed at an average interest rate of 3.85% ( individuals’ deposits – 2.66%, legal entities deposits – 3.88%), whereas in foreign currency segment the highest demand was recorded for deposits with maturity ranging from 6 to 12 months, which were placed at an average interest rate of 0.82% ( individuals’ deposits – 0.72%, legal entities deposits – 1.90%).

The highest average interest rate on domestic currency deposits was recorded for individuals’ deposits with maturity of over 5 years (6.17%) and legal entities deposits with maturity from 2 to 5 years (4.91%).

The highest average interest rate on foreign currency deposits was recorded for individuals’ deposits with maturity of over 5 years (1.68%) and legal entities deposits with maturity from 1 to 2 years (2.36%).

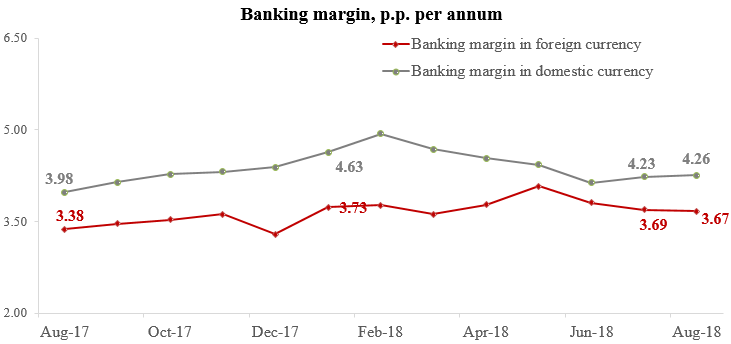

Bank interest margin on domestic currency operations increased by 0.03 pp. compared to the previous month and by 0.28 pp. compared to August 2017.

Bank interest margin on foreign currency operations decreased by 0.02 pp. compared to the previous month and increased by 0.29 pp. compared to August 2017.

1. The data are presented according to the Guidelines on Preparation and Presentation of Reports on Interest Rates applied by banks in the Republic of Moldova, approved by the Decision of the Executive Board of the NBM no. 331 of 01 December 2016, which were published in the Official Monitor of the Republic of Moldova no.441-451 of 16 December 2016, with subsequent amendments and completions.

2. As of January 1, 2018, the foreign currency-linked loans were moved from the class of domestic currency loans to foreign currency loans. According to August 2018 data as compared to August 2017: total in MDL – 8.38%; total in foreign currency - 4.52%.

3. Including individuals performing an activity.