Welcome to the official website of the National Bank of Moldova!

×

Do you have good eyesight and want to turn this tool off?

Welcome to the official website of the National Bank of Moldova!

You can choose one of the most popular reports from the list:

National Bank and the members of its decision-making bodies shall be independent in exercising the tasks conferred upon them by law, and shall neither seek nor take instructions from public authorities or from any other authority.

In order to ensure and maintain price stability over the medium term, the National Bank’s aim will be to keep inflation (measured by Consumer Price Index) at the level of 5.0 percent annually with a possible deviation of ± 1.5 percentage points, considered to be optimal for growth and development of Moldova's economy over the medium-term.

Financial stability is achieved by strengthening the resilience of the financial system, limiting the contagion effect and reducing the accumulation of systemic risks, thus contributing to the sustainability of the financial sector and economic growth.

National Bank shall have the exclusive right to issue on the territory of the Republic of Moldova banknotes and coins as legal tender, as well as commemorative and jubilee banknotes and coins as legal tender and for numismatic purposes.

National Bank is exclusively responsible for the licencing, supervision and regulation of financial institutions activity.

National Bank of Moldova acts as banker and fiscal agent of the State and shall receive from state bodies economic and financial information and documents, which are necessary for carrying out its tasks.

National Bank of Moldova is an autonomous public legal entity and is responsible to the Parliament.

National Bank shall inform the public on the monetary policy strategy on the results of the macroeconomic analysis, the evolution of the financial market and on statistics, including with regard to monetary supply, crediting, balance of payments and the state of the foreign exchange market.

National Bank of Moldova is responsable for the compilation of the balance of payments, international investment position and the statistics of the external debt of the Republic of Moldova.

Inflation Report no.2, May 2013

Due to the lack of significant resources of oil and oil refineries in the Republic of Moldova, the national economy is dependent on imports of oil derivatives, so the international oil prices fluctuations influence essentially the price developments and the pace of the national economy. The increase in commodity prices on the world market leads to higher prices on imported inputs and, therefore, on goods and services obtained on imported inputs, and could lead to the loss or restriction of markets. This determines the average fixed cost to rise and leads to the attraction of seldom used inputs into the economic circuit, new or qualitative ones, their prices being higher compared to the value of marginal productivity, due to the inefficient allocation of resources. Another consequence of the commodity price increase is the raise of taxes, fees, rents, etc., resulting in increased unit costs due to government policies. These effects are called second-round effects.

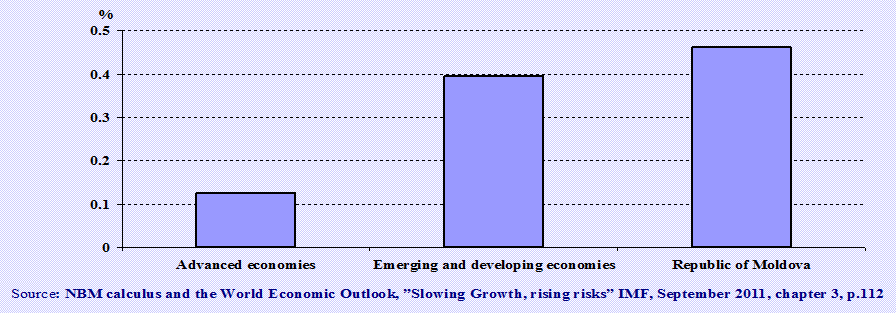

Second-round effects on core inflation are also propagated by the sharp increase in food prices on international markets, reflected in the domestic market by food prices and imports cost. According to the IMF estimates published in the “Slowing Growth, rising risks”[1] work, the impact is greater in developing countries than in advanced economies due to a higher share of food products and a reduced anchoring of inflation expectations. As for the Republic of Moldova, the estimated coefficients, based on a vector autoregression model, are similar to those of developing economies, namely the cumulative impact (until system stabilization) of a 1.0 percent shock of food prices on CPI is 0.46 percent2, while in developing countries, it hardly reaches 0.39 percent.

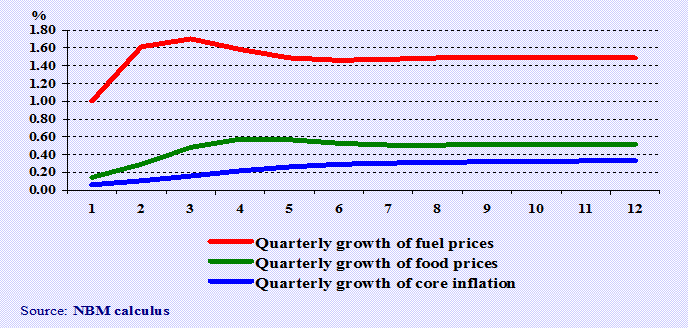

In case of fuel prices increase, the effect on core inflation growth is significant. An increase of 1.0 percent will have a cumulative impact on core inflation in the medium term of 0.33 percent. Food prices are also affected by an increase of 0.50 percentage points.

The estimation of second-round effects due to rising oil prices and food prices on international markets on core inflation are distorted as a result of the effects of intermediate variables (in particular, the nominal effective exchange rate and monetary aggregates). The appreciation of the nominal effective exchange rate would reduce, on one hand, the inflationary pressures in short term and, on the other hand, this appreciation can erode the economy’s external competitiveness, thus amplifying external imbalances. Large external imbalances increase the vulnerability of the economy to changes in investor sentiment or shocks associated with high volatility in external markets, which leads to currency depreciation and ultimately to higher inflation.

In an environment of global financial interdependence and increased uncertainty, the monetary policy regime of inflation targeting is characterized by commitment, dynamic consistency, transparency, accountability, quality evaluation, avoidance of excessive fluctuations and flexibility, a set of attributes that involves inevitably complexity. Thus, the determination and quantification of second-round effects on core inflation is essential. By alleviating these temporary effects, core inflation remains to be a part of inflation that allows trend perception and reflection of persistent sources of inflationary pressures.

[1] World Economic Outlook, ”Slowing Growth, rising risks” IMF, September 2011 chapter 3, p.112

[2] Institute of Economy, Finance and Statistics, “Economics and Sociology”, 2nd edition. 2012, p. 130