Welcome to the official website of the National Bank of Moldova!

×

Do you have good eyesight and want to turn this tool off?

Welcome to the official website of the National Bank of Moldova!

You can choose one of the most popular reports from the list:

National Bank and the members of its decision-making bodies shall be independent in exercising the tasks conferred upon them by law, and shall neither seek nor take instructions from public authorities or from any other authority.

In order to ensure and maintain price stability over the medium term, the National Bank’s aim will be to keep inflation (measured by Consumer Price Index) at the level of 5.0 percent annually with a possible deviation of ± 1.5 percentage points, considered to be optimal for growth and development of Moldova's economy over the medium-term.

Financial stability is achieved by strengthening the resilience of the financial system, limiting the contagion effect and reducing the accumulation of systemic risks, thus contributing to the sustainability of the financial sector and economic growth.

National Bank shall have the exclusive right to issue on the territory of the Republic of Moldova banknotes and coins as legal tender, as well as commemorative and jubilee banknotes and coins as legal tender and for numismatic purposes.

National Bank is exclusively responsible for the licencing, supervision and regulation of financial institutions activity.

National Bank of Moldova acts as banker and fiscal agent of the State and shall receive from state bodies economic and financial information and documents, which are necessary for carrying out its tasks.

National Bank of Moldova is an autonomous public legal entity and is responsible to the Parliament.

National Bank shall inform the public on the monetary policy strategy on the results of the macroeconomic analysis, the evolution of the financial market and on statistics, including with regard to monetary supply, crediting, balance of payments and the state of the foreign exchange market.

National Bank of Moldova is responsable for the compilation of the balance of payments, international investment position and the statistics of the external debt of the Republic of Moldova.

Inflation Report no.4, November 2013

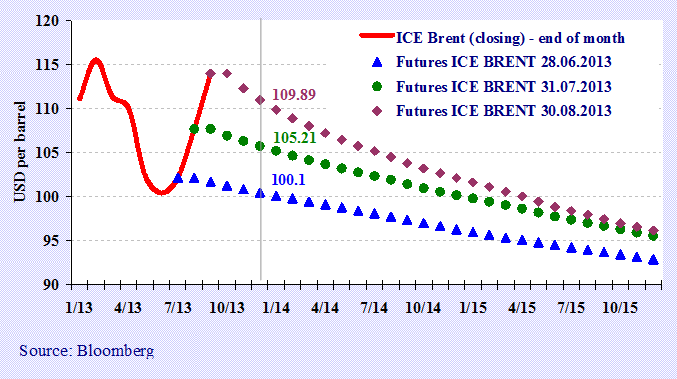

The formula of the open macroeconomic model of most countries involves a significant dependence of the economic developments on the trajectory of the economic variables of international importance. Accordingly, any macroeconomic forecast at the national and international level is based on the assumptions of variables developments of the external macroeconomic environment, the accuracy of estimated values being crucial to obtain accurate forecasts and with a minimum deviation from the actual values. Among these variables, the following can be mentioned: the oil price, exchange rates for major currencies, international commodities prices, stock indexes, shares value, etc. An advantageous option in the forecasting process is the use of forecasted values for the variables listed above on futures contracts.

Futures contracts are standardized contracts between two parties to buy or sell a specified asset of standardized quantity and quality for a price agreed upon today (the futures price or the strike price), with delivery and payment occurring at a specified future date (the delivery date). The contracts are traded on stock exchanges, which act as an intermediary between the two parties. Therefore, besides the name of the asset it is often indicated the stock exchange where the asset is quoted, for example ICE Brent Crude Oil - price in USD per barrel of Brent oil quoted on the electronic platform Intercontinental Exchange or CBOT Wheat - price in cents (U.S.) for a bushel of wheat listed on the Chicago Board of Trade. In many cases, the underlying asset to a futures contract may not be traditional commodities, but financial assets, the underlying element being any financial instrument (currency, bonds). The underlying asset can be an intangible asset or reference asset, such as indexes or interest rates.

When developing macroeconomic forecasts, the need to resort to futures contracts is essential, the primary element being the relatively high frequency of reflection of the listed asset’s response to its factors of influence, i.e. every minute during the working day of the stock exchange concerned. The difference with which the indexes of different stock exchanges reflect the change in the action of factors of influence is due the time zone. Thus, it is unnecessary to develop a macroeconomic model for the forecast of oil, metals, grains prices, etc., given that the futures contracts for those assets reflect last-minute changes of supply and demand for those assets. At the same time, in order to obtain comparable forecasts in the future, it is necessary to maintain in the forecast model a certain frequency of use of the futures contracts values.

Chart no.1 reflects the closing stock market prices of Brent oil in the last days of the months June to August 2013. It can be observed that along with increasing spot price the values for futures contracts for a period of approximately six months is also increasing significantly, which is contrary to the values of futures contracts for the period of over two years - the changes are almost insignificant and this is due to the reduction in the risk premium in the long term.