Bine ați venit pe pagină oficială a Băncii Naționale a Moldovei!

×

Ai vederea bună și dorești să închizi acest instrument?

Bine ați venit pe pagină oficială a Băncii Naționale a Moldovei!

Cele mai populare rapoarte statistice:

Banca Naţională şi membrii organelor de conducere ale acesteia sunt independenţi în exercitarea atribuţiilor stabilite de lege şi nu pot solicita şi nici accepta instrucţiuni de la autorităţile publice sau de la orice altă autoritate.

Banca Naţională informează publicul despre evoluția inflației anuale, strategia de politică monetară,rezultatele analizei macroeconomice, evoluţiei pieţei financiare şi informaţia statistică, inclusiv privind masa monetară, acordarea creditelor, balanţa de plăţi şi situaţia pieţei valutare.

Pentru asigurarea şi menţinerea stabilităţii preţurilor pe termen mediu, Banca Naţională a Moldovei menţine inflaţia (măsurată prin indicele preţurilor de consum) la nivelul de 5.0 la sută anual cu o posibilă abatere de ± 1.5 puncte procentuale, fiind considerat nivelul optim pentru creşterea şi dezvoltarea economică a Republicii Moldova pe termen mediu.

Stabilitatea financiară se realizează prin consolidarea rezilienței sistemului financiar, limitarea efectului de contagiune și diminuarea acumulării de riscuri sistemice, contribuind, astfel, la sustenabilitatea sectorului financiar și creșterea economică.

Banca Naţională a Moldovei, are dreptul exclusiv de a emite pe teritoriul Republicii Moldova bancnote şi monede metalice ca mijloc de plată. BNM pune în circulaţie bancnote şi monede metalice, prin intermediul sistemului bancar.

Banca Naţională este unica instituţie care efectuează licenţierea, supravegherea şi reglementarea activităţii instituţiilor financiare.

Banca Națională supraveghează sistemul de plăţi în Republica Moldova şi promovează funcţionarea stabilă şi eficientă a sistemului automatizat de plăţi interbancare.

Banca Naţională este o persoană juridică publică autonomă şi este responsabilă faţă de Parlament.

BNM publică statistici privind masa monetară, sectorul bancar, balanța de plăți, situația pieței valutare, etc. pentru a asigura transparența în procesul de elaborare și adoptare a deciziilor BNM, a asigura continuitatea în comunicare și predictibilitatea BNM pe piață, pentru sporirea credibilității BNM în calitate de bancă centrală dar și pe piața financiar-bancară din Republica Moldova.

Inflation Report no.4, November 2013

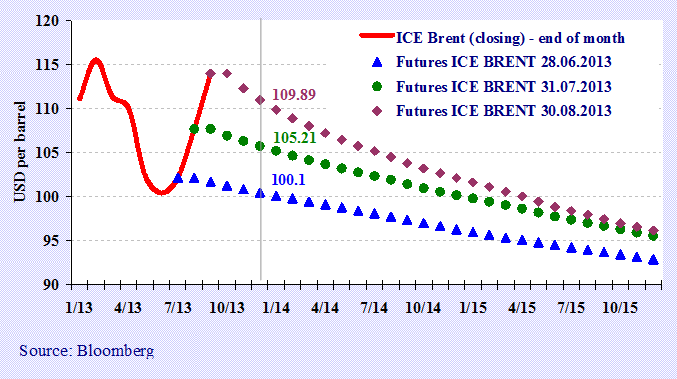

The formula of the open macroeconomic model of most countries involves a significant dependence of the economic developments on the trajectory of the economic variables of international importance. Accordingly, any macroeconomic forecast at the national and international level is based on the assumptions of variables developments of the external macroeconomic environment, the accuracy of estimated values being crucial to obtain accurate forecasts and with a minimum deviation from the actual values. Among these variables, the following can be mentioned: the oil price, exchange rates for major currencies, international commodities prices, stock indexes, shares value, etc. An advantageous option in the forecasting process is the use of forecasted values for the variables listed above on futures contracts.

Futures contracts are standardized contracts between two parties to buy or sell a specified asset of standardized quantity and quality for a price agreed upon today (the futures price or the strike price), with delivery and payment occurring at a specified future date (the delivery date). The contracts are traded on stock exchanges, which act as an intermediary between the two parties. Therefore, besides the name of the asset it is often indicated the stock exchange where the asset is quoted, for example ICE Brent Crude Oil - price in USD per barrel of Brent oil quoted on the electronic platform Intercontinental Exchange or CBOT Wheat - price in cents (U.S.) for a bushel of wheat listed on the Chicago Board of Trade. In many cases, the underlying asset to a futures contract may not be traditional commodities, but financial assets, the underlying element being any financial instrument (currency, bonds). The underlying asset can be an intangible asset or reference asset, such as indexes or interest rates.

When developing macroeconomic forecasts, the need to resort to futures contracts is essential, the primary element being the relatively high frequency of reflection of the listed asset’s response to its factors of influence, i.e. every minute during the working day of the stock exchange concerned. The difference with which the indexes of different stock exchanges reflect the change in the action of factors of influence is due the time zone. Thus, it is unnecessary to develop a macroeconomic model for the forecast of oil, metals, grains prices, etc., given that the futures contracts for those assets reflect last-minute changes of supply and demand for those assets. At the same time, in order to obtain comparable forecasts in the future, it is necessary to maintain in the forecast model a certain frequency of use of the futures contracts values.

Chart no.1 reflects the closing stock market prices of Brent oil in the last days of the months June to August 2013. It can be observed that along with increasing spot price the values for futures contracts for a period of approximately six months is also increasing significantly, which is contrary to the values of futures contracts for the period of over two years - the changes are almost insignificant and this is due to the reduction in the risk premium in the long term.