Welcome to the official website of the National Bank of Moldova!

×

Do you have good eyesight and want to turn this tool off?

Welcome to the official website of the National Bank of Moldova!

You can choose one of the most popular reports from the list:

National Bank and the members of its decision-making bodies shall be independent in exercising the tasks conferred upon them by law, and shall neither seek nor take instructions from public authorities or from any other authority.

In order to ensure and maintain price stability over the medium term, the National Bank’s aim will be to keep inflation (measured by Consumer Price Index) at the level of 5.0 percent annually with a possible deviation of ± 1.5 percentage points, considered to be optimal for growth and development of Moldova's economy over the medium-term.

Financial stability is achieved by strengthening the resilience of the financial system, limiting the contagion effect and reducing the accumulation of systemic risks, thus contributing to the sustainability of the financial sector and economic growth.

National Bank shall have the exclusive right to issue on the territory of the Republic of Moldova banknotes and coins as legal tender, as well as commemorative and jubilee banknotes and coins as legal tender and for numismatic purposes.

National Bank is exclusively responsible for the licencing, supervision and regulation of financial institutions activity.

National Bank of Moldova acts as banker and fiscal agent of the State and shall receive from state bodies economic and financial information and documents, which are necessary for carrying out its tasks.

National Bank of Moldova is an autonomous public legal entity and is responsible to the Parliament.

National Bank shall inform the public on the monetary policy strategy on the results of the macroeconomic analysis, the evolution of the financial market and on statistics, including with regard to monetary supply, crediting, balance of payments and the state of the foreign exchange market.

National Bank of Moldova is responsable for the compilation of the balance of payments, international investment position and the statistics of the external debt of the Republic of Moldova.

The financial situation of the banking sector remains robust, highlighting the ongoing efforts of the National Bank of Moldova (NBM) to strengthen stability and increase confidence in the banking system.

During the 9 months of 2025, according to data presented by banks, the banking sector was characterised by growth in assets, loans, own funds, deposits from individuals, and deposits from legal entities. At the same time, banks have continued to fully comply with prudential requirements, maintaining key indicators at the appropriate level and demonstrating good capacity to adapt and consolidate capital.

As of 30 September 2025, there were 10 licensed banks operating in the Republic of Moldova, following the completion of the reorganisation process through the merger between B.C. "VICTORIABANK" S.A. and Banca Comercială Română Chișinău S.A. (BCR Chișinău S.A.). As a result of this merger, the license of BCR Chișinău S.A. was withdrawn in accordance with Decision No. 71 of 13 March 2025 of the Executive Board of the National Bank of Moldova.

Concurrently, the National Bank of Moldova continued to promote significant reforms in the area of banking regulation and legislative harmonisation, in line with European Union standards and Basel III requirements, contributing to the modernisation of the financial system and the advancement of the European integration process.

As of 30 September 2025, the situation in the banking sector, as reflected in the reports submitted by banks, showed the following trends:

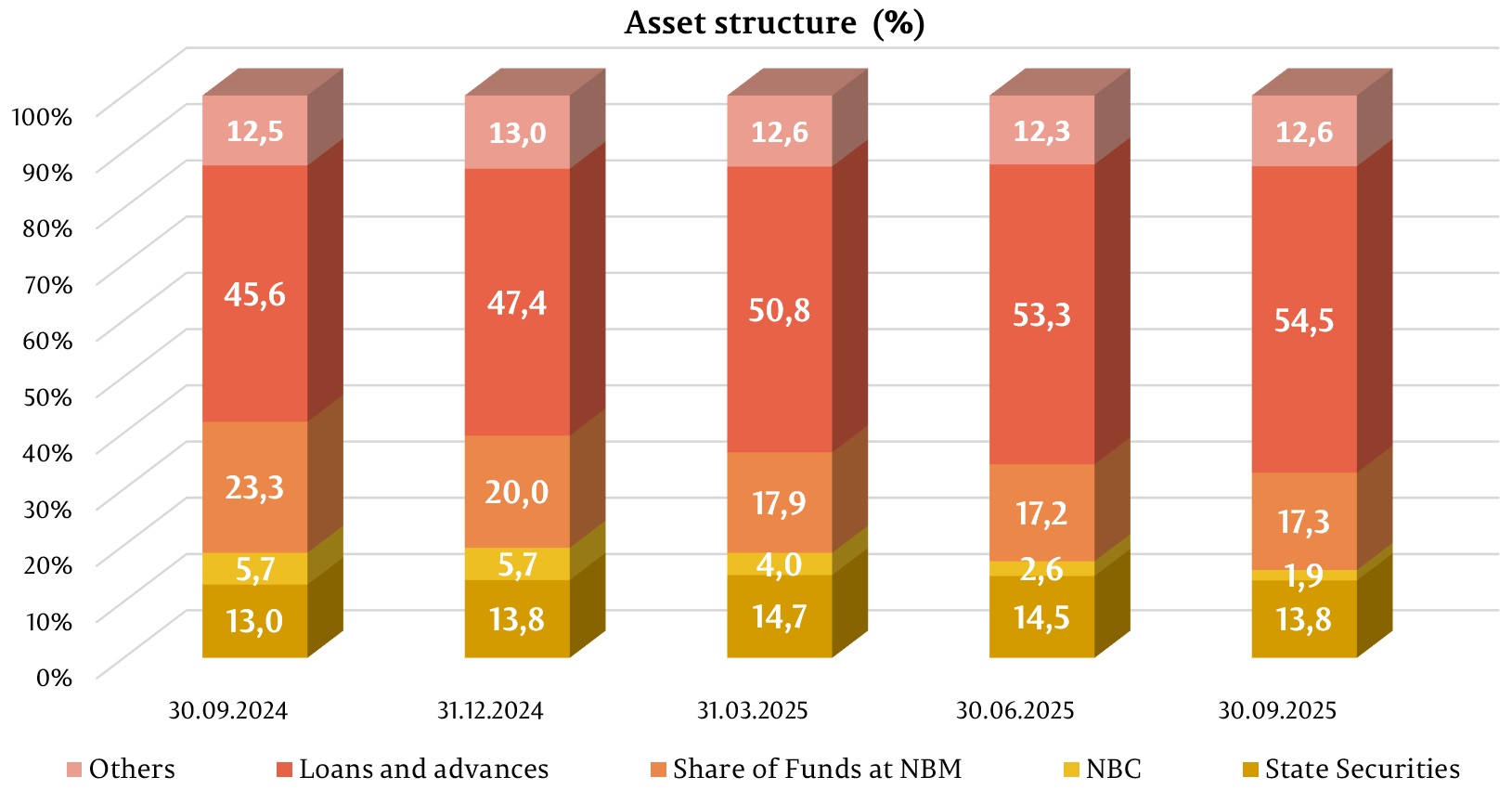

Total assets amounted to MDL 181,071.2 million, increasing by 6.3% (MDL 10,714.9 million) during the first nine months of 2025.

In the asset structure, the largest share was held by loans and advances at amortized cost, which accounted for 54.5% (MDL 98,647.9 million), up by 7.1 percentage points (p.p.) compared to the end of the previous year. The share of funds placed with the NBM was 17.3% (MDL 31,357.4 million), down by 2.7 p.p., while the share of banks' investments in state securities and NBM certificates was 15.7% (MDL 28,281.1 million), down by 3.8 p.p. The remaining assets, which account for 12.6% (MDL 22,784.8 million), are held in other banks in cash, tangible assets, intangible assets, etc. Their share decreased by 0.4 p.p. compared to the end of 2024.

The gross (prudential) balance of loans accounted for 54.8% of total assets, or MDL 99,225.0 million, increasing by 22.8% (MDL 18,400.4 million) during the period under review.

The largest increase was recorded in loans granted for the purchase/construction of real estate, by MDL 5,785.3 million (31.3%), up to MDL 24,392.3 million, in loans granted to trade, by MDL 3,390.5 million (20.1%), up to MDL 20,224.7 million, consumer loans – by MDL 3,706.6 million (25.1%), up to MDL 18,467.4 million, other loans granted – by MDL 1,612.8 million (71.8%), up to MDL 3,857.8 million, and loans granted in the field of services - by MDL 1,018.0 million (35.6%), up to MDL 3,874.8 million.

However, during the first nine months of 2025, the largest decrease was recorded in loans granted to administrative-territorial units/institutions subordinated to administrative-territorial units, by MDL 161.3 million (14.7%), to MDL 934.3 million.

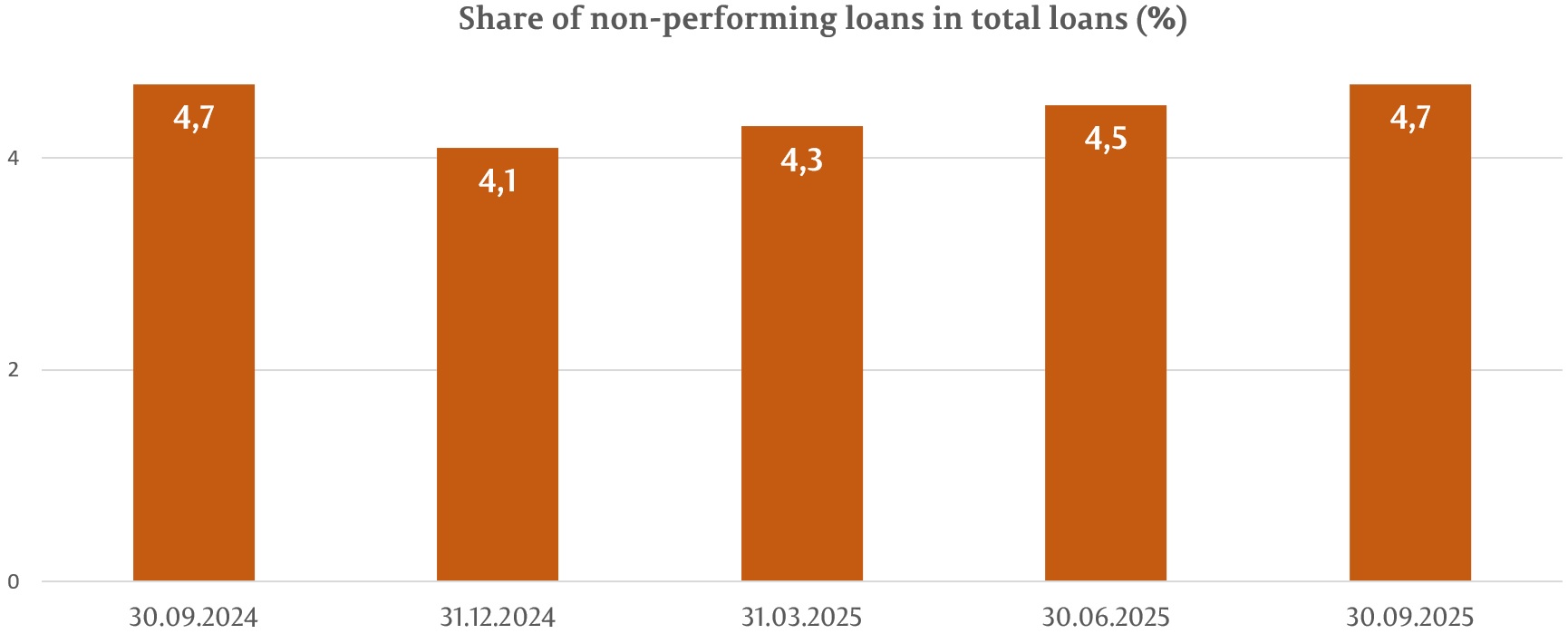

The share of non-performing loans in total loans (prudential) as of 30 September 2025, was 4.7%, up 0.6 p.p. from the end of the previous year, but remaining close to its lowest historical levels. At the same time, during the period under review, the share of expired loans in total loans decreased by 0.5 p.p., accounting for 1.4%.

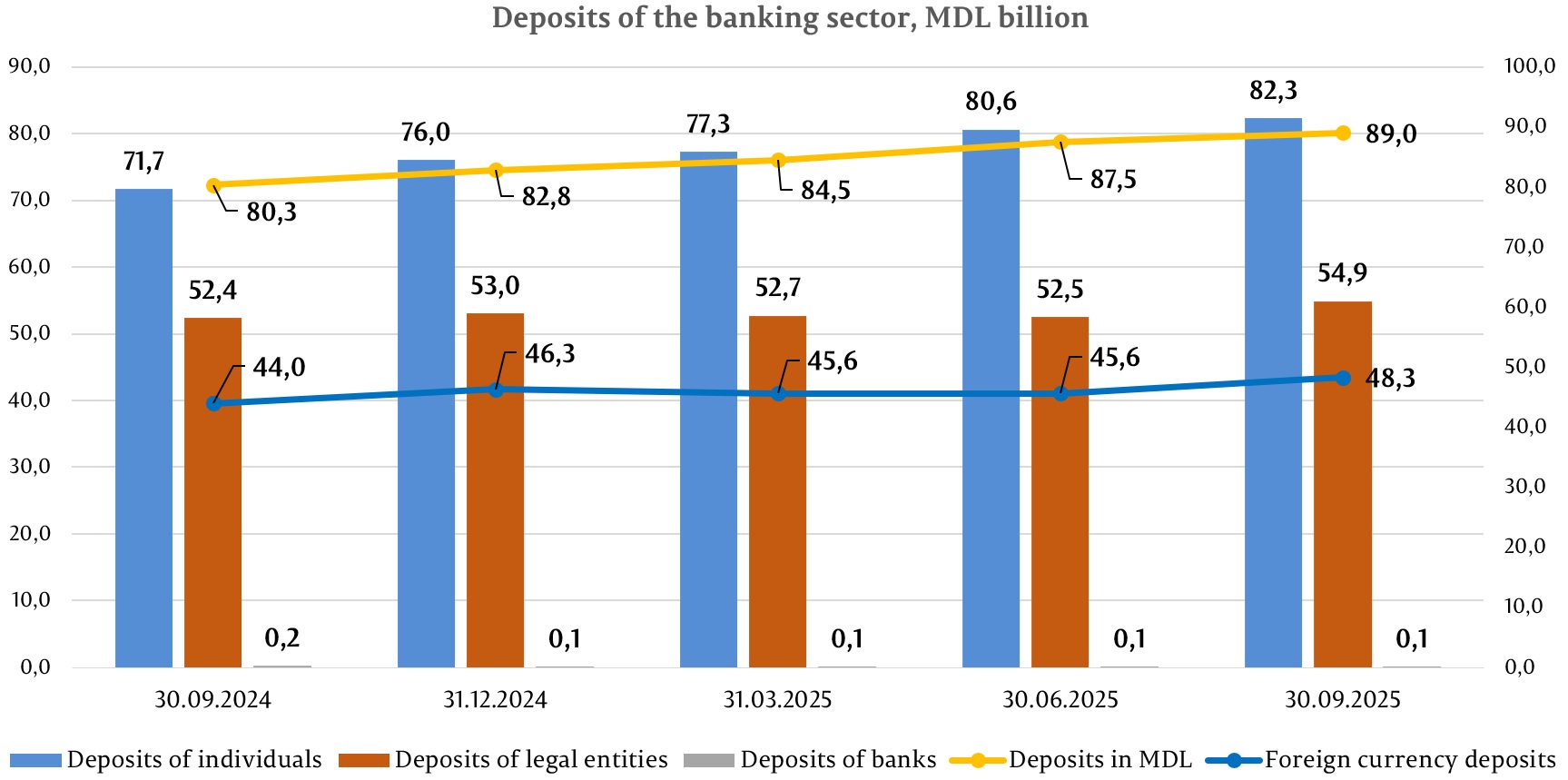

The total balance of deposits increased by MDL 8,235.3 million or 6.4% compared to the end of the previous year, amounting to MDL 137,327.0 million (deposits of individuals accounted for 59.9% of total deposits, deposits of legal entities – 40.0% and bank deposits – 0.1%), as a result of an increase in the balance of deposits of individuals by MDL 6,343.2 million (8.4%) to MDL 82,301.6 million and in the balance of deposits of legal entities by MDL 1,899.0 million (3.6%) to MDL 54,911.0 million.

Of the total deposits, 64.8% were in MDL, with the balance increasing by MDL 6,229.4 million (7.5%) compared to the end of the previous year and amounting to MDL 88,997.2 million as of 30 September 2025. Accordingly, foreign currency deposits accounted for 35.2% of total deposits, their balance also increasing during the reference period by MDL 2,005.9 million (4.3%), amounting to MDL 48,329.8 million.

As of 30 September 2025, according to data provided by banks, the banking sector's profit amounted to MDL 3,403.5 million. Compared to the same period of the previous year, the profit increased by MDL 469.9 million (16.0%), mainly due to an increase in interest income by MDL 1,453.9 million (21.8%) to MDL 8,135.9 million, as a result of an increase in income from lending activities by MDL 1,112.6 million (22.7%) to MDL 6,023.7 million.

Return on assets was 2.5%, and return on equity was 15.8%, both indicators increasing compared to the end of the previous year, by 0.1 p.p. and 1.0 p.p., respectively. Profitability indicators point to a stable and efficient banking sector with solid profitability and good resource utilisation capacity.

During the first nine months of 2025, banks continued to maintain liquidity indicators at a high level, above the regulated limits. Accordingly, all banks comply with prudential liquidity indicators.

It should be noted that, as of 30 September 2025, the net stable funding ratio (NSFR) came into force, which represents the ratio between the bank's available stable funding and the required stable funding, expressed as a percentage. Banks are required to maintain a net stable funding ratio (NSFR) of at least 100%. Thus, on 30 September 2025, the NSFR ratio for the sector was 170.3%, ranging from 151.5% to 318.1%, depending on the bank.

The long-term liquidity ratio (principle I of liquidity) was 0.79 (limit ≤1), ranging from 0.64 to 0.86, depending on the bank.

Principle III of liquidity, which represents the ratio between adjusted effective liquidity and required liquidity for each maturity band and which must not be less than 1 for each maturity band, ranging from 1.07 on the maturity band up to and including one month to 80.35 on the maturity band between one month and three months inclusive.

The liquidity coverage ratio (LCR) indicator by sector stood at 269.7% (limit ≥ 100%), ranging from 162.5% to 1,064.6%, depending on the bank.

According to the reports submitted by banks as of 30 September 2025, the total own funds ratio for the banking sector was 25.2%, ranging from 20.7% to 39.6%, depending on the bank. All banks complied with the "Total own funds ratio" indicator (limit ≥ 10%).

Banks also complied with the requirement for the "Total own funds ratio" indicator, taking into account capital buffers.

As of 30 September 2025, total own funds amounted to MDL 24,421.4 million, up by 8.7% (MDL 1,954.1 million). The increase in own funds was determined by the reflection by certain banks of eligible profits after the general meetings of shareholders and after obtaining the permission of the NBM to include the profits obtained in own funds. At the same time, seven banks distributed dividends in accordance with the decisions of the shareholders.

As of 30 September 2025, banks complied with prudential indicators regarding large exposures and exposures to their affiliated persons.

During the reporting period, banks complied with the limit on the dominant position in the banking market, remaining below the 35% limit for this indicator regarding the size of assets and deposits of individuals, with the exception of one bank, which exceeded the 35% limit for the dominant position based on asset size, accounting for 35.3%, and the dominant position in the banking market in terms of deposits of individuals was 35.7%.

During the third quarter of 2025, the National Bank of Moldova continued to develop and update secondary legislation for the implementation of Law No 202/2017 on Banking Activity, promoting Basel III requirements, and best practices in the sector.

In this regard, by Decision No 177/2025 of the Executive Board of the NBM, amendments were made to Regulation No 109/2019 on large exposures. The amendments were aimed at supplementing the regulation with specific provisions for determining indirect exposures to a client arising from derivative contracts, by transposing Delegated Regulation (EU) 2022/1011 supplementing Regulation (EU) No 575/2013 with regard to regulatory technical standards specifying how to determine indirect exposures to a client arising from derivative contracts and credit derivative contracts, where the contracts are not entered into directly with that client, but the underlying debt or equity instrument has been issued by that client.

At the same time, by Decision of the Executive Board of the NBM No 218/2025, amendments were made to Regulation No 292/2018 on the requirements for members of the management body of a bank, financial holding company or mixed holding company, managers of a branch of a bank in another country, persons holding key positions and the liquidator of a bank in the process of liquidation. Thus, the regulation has been supplemented with provisions related to streamlining the process of assessing/reassessing members of the management body of banks, managers of branches of banks in other countries, and persons holding key positions, and optimizing the process of monitoring persons for their compliance with the criteria established by the regulatory framework. In addition, the amendments aim to improve corporate governance in the private sector by specifying, clarifying, and improving certain aspects, namely, refining the mechanism for assessing/reassessing persons nominated for management positions and persons holding key positions.

Furthermore, by Decision No 219/2025 of the Executive Board of the NBM, Regulation No 322/2018 on the framework for the administration of banking activities was supplemented with provisions aimed at updating, improving, and strengthening corporate governance in banks by aligning it with the international regulatory framework in this sector, including the rules prescribed within the EU. The main changes include provisions concerning the development of elements that need to be taken into account when assessing whether members of the management body devote sufficient time to performing their duties; compliance with gender neutrality in the development and implementation of remuneration policy; policies on conflicts of interest of employees arising from previous relationships; supplementing the policy on the appointment of members of the management body and persons holding key functions with a succession plan, a policy to promote diversity within the management body, and a policy for the induction and training of members of the management body and persons holding key functions, etc.

By Decision No 220/2025 of the Executive Board of the NBM, the Regulation on the treatment of counterparty credit risk for banks was approved, which is intended to introduce new treatment in relation to risk management regulation, namely with regard to the treatment applicable to counterparty credit risk, in particular by introducing own funds requirements and new methods for determining the exposure value for bilateral contracts with derivative financial instruments, repurchase transactions, securities or commodities lending or borrowing transactions, long settlement transactions, and margin lending transactions.

In the context of the National Bank of Moldova's commitment to align the banking legislation of the Republic of Moldova with the European Union acquis, by Decision No 221/2025 of the NBM Executive Board, the Regulation on the prudential treatment of securitisations was approved, which represents the secondary regulatory framework for the prudential treatment of securitisations.