Welcome to the official website of the National Bank of Moldova!

×

Do you have good eyesight and want to turn this tool off?

Welcome to the official website of the National Bank of Moldova!

You can choose one of the most popular reports from the list:

National Bank and the members of its decision-making bodies shall be independent in exercising the tasks conferred upon them by law, and shall neither seek nor take instructions from public authorities or from any other authority.

In order to ensure and maintain price stability over the medium term, the National Bank’s aim will be to keep inflation (measured by Consumer Price Index) at the level of 5.0 percent annually with a possible deviation of ± 1.5 percentage points, considered to be optimal for growth and development of Moldova's economy over the medium-term.

Financial stability is achieved by strengthening the resilience of the financial system, limiting the contagion effect and reducing the accumulation of systemic risks, thus contributing to the sustainability of the financial sector and economic growth.

National Bank shall have the exclusive right to issue on the territory of the Republic of Moldova banknotes and coins as legal tender, as well as commemorative and jubilee banknotes and coins as legal tender and for numismatic purposes.

National Bank is exclusively responsible for the licencing, supervision and regulation of financial institutions activity.

National Bank of Moldova acts as banker and fiscal agent of the State and shall receive from state bodies economic and financial information and documents, which are necessary for carrying out its tasks.

National Bank of Moldova is an autonomous public legal entity and is responsible to the Parliament.

National Bank shall inform the public on the monetary policy strategy on the results of the macroeconomic analysis, the evolution of the financial market and on statistics, including with regard to monetary supply, crediting, balance of payments and the state of the foreign exchange market.

National Bank of Moldova is responsable for the compilation of the balance of payments, international investment position and the statistics of the external debt of the Republic of Moldova.

In the first semester of 2019, the National Bank of Moldova (NBM) continued its efforts to assure a sound corporative governance, transparency of the banking ownership, with the aim to maintain a stable banking sector and to attract potential investors.

As of 30 June2019, 11 licensed banks by the National Bank of Moldova were operating in the Republic of Moldova. In 2019, significant changes in the shareholders structure of some banks were registered. Thus, on 22 January 2019, the NBM granted preliminary permission to the European investor Doverie United Holding AD to purchase 63.89% of shares of BC ”MOLDINDCONBANK” SA, the second bank in the banking sector considering the amount of assets.

It is worth mentioning that on 4 April 2019 the Regulation on Banking Activity Management Framework entered into force; it will improve the banking regulation and supervision framework, especially in the field of risk management. According to the above-mentioned Regulation, by 30 April 2019, banks had to submit, for the first time, reports on the internal capital adequacy assessment process (ICAAP) effective on 31 December 2018. Through ICAAP, banks asses the risk profile and adequacy degree of the internal capital, while the NBM – within the Supervisory Review and Evaluation Process Methodology (SREP) – shall analyze the ICAAP process and sufficiency of the internal capital estimated by banks.

The National Bank of Moldova has also approved the Supervisory Review and Evaluation Process Methodology (SREP) (hereinafter – methodology), which transposes international standards and best practices in the field of banking sector supervision. . The approval of methodology is a part of the reformation process of the national framework and represents a fundamental step in the implementation of a future-oriented risk-based supervision process using professional reasoning. This approach will provide an overall approach by early detection of bank risks and deficiencies, which will contribute to streamlining supervision, ensuring the viability and stability of the banking sector. The SREP reports of banks shall be elaborated in the second semester of 2019.

In the first semester of 2019, the consolidation of own funds and growth of the loan portfolio in the banking sector continued. It is worth mentioning that the share of non-performing loans in loan portfolios decreased, but remains relatively high. The banking sector has a high level of liquidity. The profit obtained in the first semester of 2019 registered an increase compared to the similar period of the previous year. At the same time, the volume of deposits increased, mainly the deposits of individuals.

BC „MOLDOVA-AGROINDBANK” S.A.

On the 4 April 2019, the Executive Board of the NBM lifted the intensive supervision regime for BC „MOLDOVA-AGROINDBANK” S.A. and revoked the measures prescribed in the period of special supervision.

The decision was adopted after it was found that the bank assures the transparency in the structure of its shareholders, following the acquisition of 41.09% of the bank’s share capital by HEIM PARTNERS LIMITED, a company representing an international consortium of investors: EBRD, Invalda INVL, and Horizon Capital. At the same time, the new Board of the BC „MOLDOVA-AGROINDBANK” S.A., established on 22 November 2018 by the decision of the annual general meetings of the bank’s shareholders, started to exercise its mandate since 21 March 2019. On 14 June 2019, the NBM approved the seventh member of the Board of the bank, its composition becoming full.

BC „MOLDINDCONBANK” S.A.

BC „MOLDINDCONBANK” S.A. continues to be set under an early intervention regime.

For avoiding excessive risks, the activity of the BC „MOLDINDCONBANK” S.A. under early intervention regime is monitored daily by the National Bank. Consequently, the monitoring is done through the examination of financial statements of this bank, its transactions, the agenda of meetings of management bodies, etc.

The early intervention regime on BC „MOLDINDCONBANK” S.A. was set in October 2016, following the finding by the NBM of concerted activities of a group of persons who acquired and held a qualifying holding of 63.89%, without the prior written approval of the NBM.

According to the law, the above-mentioned shares were supposed to be disposed of within the established deadlines. Since they were not sold, in January 2018 they were cancelled, and new shares in amount of 63.89% of the share capital of the bank were issued by the bank, which have been exposed to sale for a period of three months, as a single package, at a price set after the evaluation made by an international audit company. The deadline for sale was extended several times, while the latest three months extension was established by decision of the Executive Board of the National Bank of Moldova on 18 January 2019.

In January 2019, the Executive Board of the NBM adopted the decision on the preliminary approval to acquire more than 50% of the share capital of BC “MOLDINDCONBANK” S.A. by the potential Bulgarian investor “Doverie-Invest” S.A.

In February 2019, the sale-purchase transaction of the new-issued single share package by BC “MOLDINDCONBANK” S.A. was performed, following which, on 21 February 2019 the Agency for Public Property purchased and registered the ownership rights on the package of 3,173,751 shares, which accounts for 63.89% of the share capital of BC “MOLDINDCONBANK” S.A. Subsequently, on 18 March 2019, during the auction conducted on the regulated market of the Stock Exchange, the Bulgarian company “Doverie-Invest” S.A. acquired 3,173,751 shares of B.C. “MOLDINDCONBANK” S.A., as a single package, at the total value of MDL 764.0 million displayed for sale by the Public Property Agency. The registration of ownership rights on the above-mentioned shares was carried out on 22 March 2019, thus, “Doverie-Invest” S.A. became the controlling shareholder with a qualifying holding of 63.89% in the bank’s capital. In addition, following the mandatory offer of taking over the shares, it acquired other 13.73%. At the moment, the company holds 77.62% of the shares issued by BC „MOLDINDCONBANK” S.A.

Subsequently, the Executive Board of the National Bank of Moldova decided to extend for six months, starting with 20 April 2019, the mandate of temporary administrators of BC „MOLDINDCONBANK” S.A. The mandate was extended considering the need to assure a continuous, uninterrupted and prudent management of the bank during the period of designation and approval period, according to its Bylaws and legislation, of its statutory management bodies.

BC „MOLDINDCONBANK” S.A. operates in normal regime, provides all services, including those related to deposit, lending and settlement operations.

Following the process of making the banking ownership transparent, on 11 January 2019, the Executive Board of the NBM adopted two decisions regarding the „Banca de Finanţe şi Comerţ” S.A. and BC „ENERGBANK” S.A.

With regard to the „Banca de Finanțe şi Comerţ” S.A., the National Bank of Moldova found that a group of persons acted in concert, by purchasing and entering a qualifying holding (substantive quote) in the share capital of the bank of 36.15%, without the prior written permission of the National Bank, violating the Law on the banks’ activity. Therefore, the National Bank suspended the exercise of certain rights for these shareholders (right to vote, right to convoke and organize the general meeting of shareholders, right to introduce topics on the agenda, right to propose candidates as members of the Supervisory board and the executive board and the right to receive dividends). The respective shareholders had to dispose their shares within the time limits provided by law.

With regard to the B.C. „ENERGBANK” S.A., the National Bank identified, as well, concerted activity of a group of shareholders with qualifying holding of 52.55% in the share capital of the bank, without the prior written permission of the NBM. Thus, the NBM decided on the suspension in the exercise of some rights for the group of shareholders concerned, who had to dispose the shares held in the share capital of the BC „ENERGBANK” S.A. in three months.

On 11 January 2019, following the NBM assessment, the Executive Board of the National Bank of Moldova decided to suspend some rights of a shareholder that held 3.98% of the share capital of BC „ENERGBANK” S.A. The shareholder’s rights were suspended because of failing to comply with the requirements on the financial adequacy and solidity, provided in Article 48 of the Law on banks’ activity no 202 of 06.10.2017. The respective shareholder was supposed to dispose the shares held in the share capital of BC “ENERGBANK” SA within the terms provided by the Law. Therefore, considering the size of the package of shares, which exceeds 50% of the share capital, the NBM decided to apply measures of early intervention for B.C. „ENERGBANK” S.A., based on the Law on bank’s recovery and resolution. Some of the members of the management body of the bank that remained functional were supplemented with temporary administrators, appointed by the NBM, with the purpose to assure a prudential governance of the activity of the bank during the period of solving the deficiencies identified in the banks’ ownership structure.

On 21 February 2019, the Executive Board of the NBM decided to apply measures of suspending the exercise of some rights of the direct shareholder of qualifying holding in amount of 9.6% from the share capital of B.C. „ENERGBANK” S.A. for failure to comply with the requirements on the adequacy and financial soundness, provided by Article 48 of the Law on banks’ activity No 202 of 06.10.2017. Considering the fact that the shareholder did not voluntarily dispose of its shares in the established three months term, in June 2019 the shares were cancelled and new shares were issued and exposed for sale.

Subsequently, in April 2019, the Executive Board of the NBM decided to extend with three months the term of the disposal of shares of B.C. „ENERGBANK” S.A. and „Banca de Finanțe şi Comerţ” S.A. by shareholders.

In the first semester of 2019, several banks (B.C. ”EuroCreditBank” S.A., B.C. ”EXIMBANK” S.A, BC ”ProCredit Bank” S.A.) were sanctioned with warning following the targeted and full scope inspections performed by the NBM. The warnings were applied against B.C. ”EuroCreditBank” S.A. after the targeted inspection for the assessment of adequacy of information systems and continuity of activity, while against the B.C. ”EXIMBANK” S.A. and BC ”ProCredit Bank” S.A. – following the non-compliance with some requirements of the law, as well as the deficiencies established in the management framework etc.

Therefore, banks shall eliminate all the deficiencies identified during the on-site inspections.

As of 30 June 2019, the situation in the banking sector, as it is described in the reports submitted by the licensed banks, registered the following trends:

Assets and Liabilities

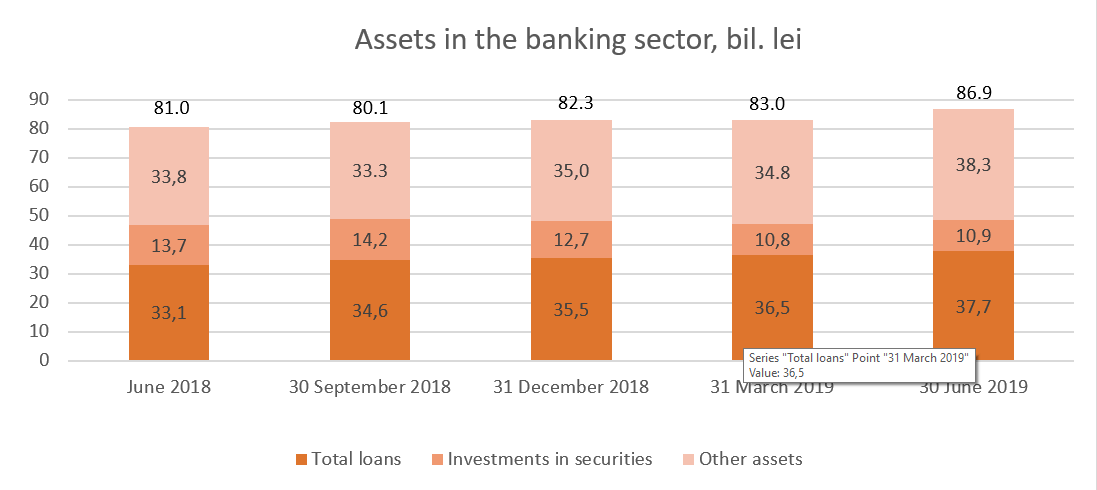

The total assets amounted to MDL 86.9 billion, increasing during the first semester of 2019 by 4.6% (MDL 3.8 billion). In the structure of assets, the most significant rise was registered in credits and advances, by 9.5% (MDL 3.3 billion).

As of 30 June 2019, the balance of the gross loan portfolio accounted for 43.4% of the total assets or MDL 37.7 billion, which represents an increase of 9.4% (MDL 3.3 billion) during the reporting period. In addition, the volume of new loans granted in the first semester of 2019 increased by 22.9% compared to the same period of the previous year.

The largest increases in the loan portfolio were recorded in the loans granted for the purchase/construction of real estate and consumer loans, due to the decrease of interest rate in the analyzed period. At the same time, the National Bank continues to encourage banks to focus their efforts on financing the real economy.

The investments in securities (certificates of the National Bank state securities) recorded a share of 12.5% (MDL 10.9 billion) of the total assets, which represents 2.7 percentage points less compared to the end of 2018.

The rest of assets, which amount to 44.1%, are held by banks in the accounts opened with the National Bank, in other banks and in cash, etc.

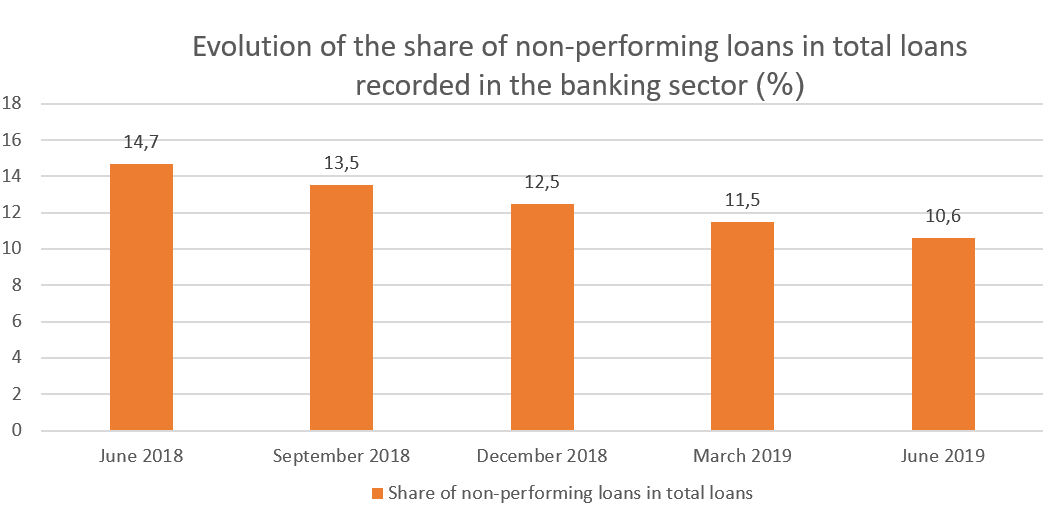

During the referred period, the share of non-performing loans (substandard, doubtful and compromised) in the total loans has decreased by 1.9 percentage points compared to the end of 2018, and represented 10.6% on 30 June 2019. This share diminished at almost all banks with an indicator varying from 4.9% to 26.0%. To a great extent, banks tend to reduce the share of non-performing loans in the total loans.

The decrease in the share of non-performing loans in the total loans was caused mainly by the decrease of the balance of non-performing loans by 7.3% (MDL 323.3 million), simultaneously with the rise in the gross balance of loans by 9.4% (MDL 3.3 million).

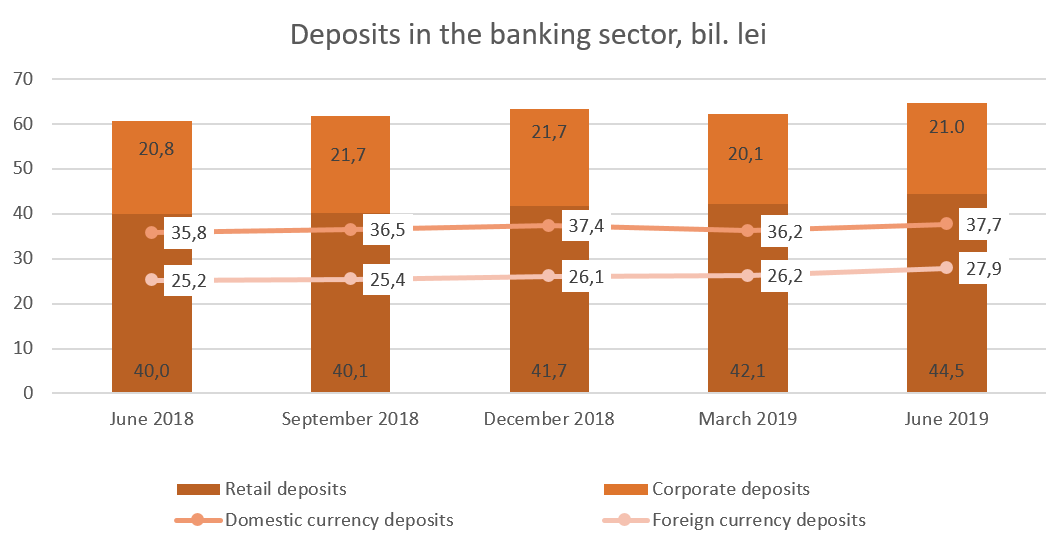

In addition, an increasing trend of the balance of deposits was registered. According to the prudential reports, they increased by 3.5% in the reference period and amounted to MDL 65.7 million (the deposits of individuals constituted 67.7% of the total deposits, the deposits of legal entities – 32.0% and the deposits of banks – 0.3%). The biggest impact on the increase of balance of deposits was brought by the rise in deposits of individuals by MDL 2.8 billion (6.8%), while the balance of deposits of legal entities diminished by MDL 677.3 million (3.1%).

Out of the total deposits, 57.4% are deposits in domestic currency, which balance increased insignificantly by MDL 374.8 million (1.0%), and constituted MDL 37.7 billion on 30 June 2019. The deposits in foreign currency constituted 42.6% of the total deposits, which is an increase for the reference period by MDL 1.9 billion (7.1%), totaling MDL 27.9 billion. Therefore, the sum of deposits attracted in foreign currency represented the equivalent of MDL 331.6 million, while the exchange rate fluctuation represented MDL (+1.5) billion.

Income and rentability

As of 30 June 2019, the profit of the banking system represented MDL 1.2 billion, which is an increase of 30.8% (MDL 271.4 million) compared to the similar period last year.

Total revenues amounted to MDL 3.5 billion, out of which: interest income – 61.3% (MDL 2.2 billion), while the non-interest income – 38.7% (MDL 1.4 billion). At the same time, the total volume of expenditures constituted MDL 2.4 billion, including the expenditure with interest – 28.7% of the total expenditures (MDL 679.6 million), while the non-interest expenditures – 71.3% of the total expenditures (MDL 1.7 billion).

The increase of the profit resulted from the increase of non-interest incomes by 12.7% or by MDL 152.9 million, especially following the rise in incomes from fees and commissions by 15.9% (MDL 122.1 million).

Expenditures with interest decreased by 10.9% or by MDL 83.1 million. The insignificant increase of interest rate revenues by 0.5% or by MDL 11.2 million was caused by the decrease in the average interest rate of loans.

As of 30 June 2019, the return on assets and capital constituted 2.6% and 15.5% respectively, increasing by 0.9 percentage points and 5.2 percentage points, compared to the end of the previous year.

Compliance with prudential requirements

Banks continue to maintain the indicators of liquidity at a high level. Thus, the value the long-term liquidity indicator (principle I of liquidity) amounted to 0.7 (limit ≤1), being at the same level as at the end of the last year.

The current liquidity of the banking sector (principle II of liquidity) diminished by 3.1 percentage points and constituted 51.6% (limit ≥20%), more than half of the assets of banking sector being concentrated in liquid assets. It is worth mentioning that the largest share in liquid assets belongs to NBM deposits – 42.7%, followed by liquid securities 24.4% and net interbank funds – 21.8%. In the first semester of 2019, the share of net interbank funds increased by 4.2 percentage points. At the same time, the share of liquid securities decreased by 3.6 percentage points, and the share of NBM deposits – by 0.6 percentage points, the share of cash having the same level as at the end of the previous year.

Principle III of liquidity, which represents the ratio between the adjusted effective liquidity and the necessary liquidity on each maturity band, and which should not be lower than 1 per each maturity band, was respected by all banks.

According to the reports submitted by banks on 30 June 2019, the total own funds rate in the banking sector constituted 26.5%, which is similar to the rate at the end of the previous year. The regulated limit is respected by each bank and varies between 19.2% to 65.7%.

As of 30 June 2019, the total own funds constituted MDL 11.5 billion and recorded an increase of 4.8% (MDL 522.4 million) during the mentioned period. The increase in the own funds was caused mainly by the eligible profit reflected by the bank after the organization of the general meeting of the shareholders.

On 19 June 2019, the new amendments to the Regulation on large exposures and the Regulation on bank’s transactions with related parties entered into force. These regulations changed the modality of calculation of large exposures and exposures towards related parties, which provides the calculation of exposures considering the diminishing effect of the credit risk (decrease caused by drops in exposures), as well as preserving the total own funds for the surplus established by regulation. In addition, the requirement for the inclusion in the calculation of large exposures of funds registered in the “Nostro” accounts of placements from banks which hold credit rating level 3. Therefore, starting with 19 June 2019, the placements in banks with BBB-/Baa3 rating assigned by at least one of the agencies Standard&Poor’s, Moody’s and Fitch-IBCA, are considered at the calculation of large exposures. According to the mentioned amendments, four banks exceed the prudential limit of maximum exposure towards a client or a group of connected clients, established by the NBM at 15% of the eligible capital.

With regard to the Regulation on banks’ transactions with its related parties, a bank exceeds the prudential limit of 10% of the ratio of maximum exposure towards a related person and/or group of connected clients and the eligible capital. Also, two banks exceed the prudential limit of 20% of the indicator related to the aggregate amount of bank’s exposure towards the related persons and/or groups of connected clients and the eligible capital.

The National Bank closely monitors these excesses and cooperates with banks to assure an adequate regulatory basis that will assure an efficient risk management.

Moreover, at two banks the ratio between the indicator of the aggregate amount of exposures from credits for clients or groups of connected clients, which constitute by size the first ten exposures from credits, and the total credit portfolio is bigger than the prudential limit of 30%. Considering that banks maintain the additional requirement for own funds for the respective surplus, exceeding the 30% limit is not a violation.

In April 2019, following the entry into force of the Law No 202/2017 on banks’ activity, the National Bank of Moldova:

The National Bank of Moldova will continue to elaborate regulatory acts for the execution of the Law No 202/2017 on the banks’ activity.

Aligning the banking legislation of the Republic of Moldova to international standards by improving the quantitative and qualitative bank management mechanisms will contribute to the promotion of a secure and stable banking sector, increase of transparency, trust and attractiveness of the domestic banking sector for potential investors and creditors of banks, as well as for depositors and clients. It will also contribute to the development of new financial products and services.