Welcome to the official website of the National Bank of Moldova!

×

Do you have good eyesight and want to turn this tool off?

Welcome to the official website of the National Bank of Moldova!

You can choose one of the most popular reports from the list:

National Bank and the members of its decision-making bodies shall be independent in exercising the tasks conferred upon them by law, and shall neither seek nor take instructions from public authorities or from any other authority.

In order to ensure and maintain price stability over the medium term, the National Bank’s aim will be to keep inflation (measured by Consumer Price Index) at the level of 5.0 percent annually with a possible deviation of ± 1.5 percentage points, considered to be optimal for growth and development of Moldova's economy over the medium-term.

Financial stability is achieved by strengthening the resilience of the financial system, limiting the contagion effect and reducing the accumulation of systemic risks, thus contributing to the sustainability of the financial sector and economic growth.

National Bank shall have the exclusive right to issue on the territory of the Republic of Moldova banknotes and coins as legal tender, as well as commemorative and jubilee banknotes and coins as legal tender and for numismatic purposes.

National Bank is exclusively responsible for the licencing, supervision and regulation of financial institutions activity.

National Bank of Moldova acts as banker and fiscal agent of the State and shall receive from state bodies economic and financial information and documents, which are necessary for carrying out its tasks.

National Bank of Moldova is an autonomous public legal entity and is responsible to the Parliament.

National Bank shall inform the public on the monetary policy strategy on the results of the macroeconomic analysis, the evolution of the financial market and on statistics, including with regard to monetary supply, crediting, balance of payments and the state of the foreign exchange market.

National Bank of Moldova is responsable for the compilation of the balance of payments, international investment position and the statistics of the external debt of the Republic of Moldova.

During 2021, the National Bank of Moldova (NBM) continued the process of prudential supervision of banks in the Republic of Moldova, pursuing compliance with legal requirements, to ensure the stability and viability of the banking system.

The banking sector, for the period of 2021, according to the data presented by the banks, is characterized by high liquidity, growth in assets, loans, own funds, deposits of natural and legal persons. Also, the profit for the year compared to the previous year increased to the pre-pandemic size.

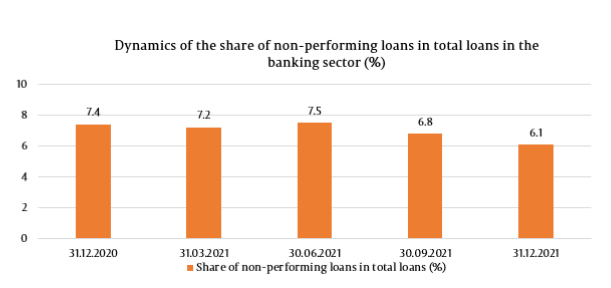

Although there was a slight increase in the amount of non-performing loans, the quality of the loan portfolio improved compared to the end of the previous year, due to the higher growth rate of the loan portfolio compared to non-performing loans and the decrease in the share of expired loans by 1.4 percentage points to 3.1%.

As of 31.12.2021, 11 banks licensed by the National Bank of Moldova were active in the Republic of Moldova. A bank was supervised under the early intervention regime applied on 11.01.2019 as a result of the finding a group of persons acting in concert who acquired and possessed a qualified holding in the bank's share capital in the amount of 52.55% without the approval prior written consent of the NBM. The period for appointing temporary administrators was later extended by NBM Executive Committee Decisions until April 29, 2022.

During 2021, no significant changes were recorded in the shareholding structure of licensed banks in the Republic of Moldova.

As of 31.12.2021, the situation in the banking sector, reflected by the reports submitted by banks, registered the following trends:

Assets and liabilities

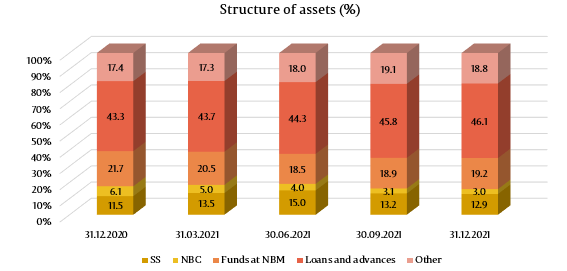

Total assets amounted to 118.5 billion lei, rising by 14.2% (14.7 billion lei) during 2021.

The largest share in total assets went to loans and advances at amortized cost, which amounted to 46.1% (54.6 billion lei), increasing by 2.8 percentage points (pp). The share of funds at the NBM was 19.2% (22.7 billion lei), decreasing by 2.5 pp. The share of banks' investments in state securities and National Bank certificates (NBC) was 15.9% (18.8 billion lei), decreasing by 1.7 pp. The rest of the assets, which account for 18.8% (22.3 billion lei), are kept by banks in other banks, cash, tangible assets, intangible assets, etc. Their share increased by 1.4 pp.

The gross (prudential) loan balance was 47.6% of total assets, or 56.4 billion lei, and increased by 23.5% (10.7 billion lei) during the examined period. At the same time, the volume of new loans granted during 2021 increased by 38.7% compared to the same period of the previous year.

The largest increases in the loan portfolio were recorded in loans granted for the purchase or construction of real estate - by 45.0% (3.5 billion lei) to 11.4 billion lei, and consumer loans - by 40.2% (3.0 billion lei) up to 10.5 billion lei.

During the reference period, the share of non-performing loans (substandard, doubtful, and compromised) in total loans decreased by 1.2 percentage points, amounting to 6.1% on 31.12.2021, with the indicator ranging from 2.1% to 11.3%, depending on the bank.

At the same time, non-performing loans in absolute value increased by 2.7% (90.8 million lei), amounting to 3.5 billion lei.

During the analysed period, the share of expired loans in total loans decreased from 4.5% to 3.1%.

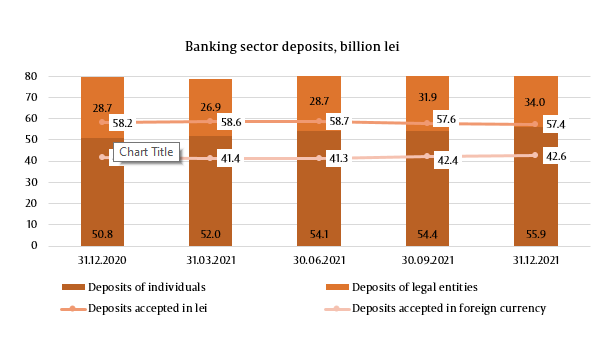

At the same time, the balance of deposits increased during the reference period. According to prudential reports, it increased by 10.4 billion lei, or 13.1%, amounting to 90.1 billion lei (deposits of individuals accounted for 62.1% of total deposits, deposits of legal entities - 37.8%, and deposits of banks - 0.1%), due to the increase in the balance of deposits of individuals by 5.1 billion lei (10.1%), up to 55.9 billion lei, deposits of legal entities - by 5.3 million lei (18.4% ), up to 34.0 billion lei, and deposits of banks - by 0.2 million lei (0.2%) up to 148.1 million lei.

In total deposits, 57.4% went to deposits in lei, their balance increasing by 5.4 billion lei (11.6%) compared to the end of the previous year and amounting to 51.7 billion lei as of 31.12.2021. Foreign currency deposits accounted for 42.6% of total deposits, and their balance increased during the reference period by 5.1 billion lei (15.2%), making up 38.4 billion lei (attracting foreign currency deposits - the equivalent of 5.9 billion lei; total revaluation of foreign currency deposits - (-901.9 million lei)).

Revenues and profits

As of 31.12.2021, the profit in the banking system amounted to 2.3 billion lei, increasing by 53.3% (800.7 million lei) compared to the end of the previous year.

The increase in profit was determined by the increase in interest income by 739.2 million lei (16.9%), income from fees and commissions - by 545.5 million lei (27.6%), and the decrease in depreciation of financial assets that are not valued at fair value through profit or loss in the amount of 386.6 million lei (75.6%).

Total revenues amounted to 9.0 billion lei, increasing compared to the end of the previous year by 1.2 billion lei (15.1%). Of which, interest income accounted for 56.9% (5.1 billion lei) and non-interest income - 43.1% (3.9 billion lei).

At the same time, total expenses amounted to 6.7 billion lei, increasing compared to the end of the previous year by 378.6 million lei (6.0%). Of which, interest expenses accounted for 18.6% (1.2 billion lei) of total expenses, and non-interest expenses - 81.4% (5.4 billion lei) of total expenses.

As of 31.12.2021, return on assets and return on capital accounted for 2.0% and 12.3%, having increased by 0.5 pp. and 3.6 pp, respectively, compared to the end of the previous year.

Compliance with prudential requirements

Throughout 2021, banks continued to keep liquidity indicators high above regulated limits.

Thus, the value of the long-term liquidity indicator (liquidity principle I) was 0.74 (limit ≤1), ranging from 0.35 to 0.89 and being practically at the same level as at the end of 2020.

Liquid assets amounted to 57.6 billion lei, and current liquidity in the sector (liquidity principle II) amounted to 48.6% (limit ≥20%), ranging from 34.6% to 63.3%, decreasing by 2.1 percentage points compared to the end of the previous year.

In the structure of liquid assets in the banking sector, the largest share went to deposits with the NBM - 39.5%, followed by liquid securities - 30.1%, current net interbank funds - 20.3%, and cash and other monetary values - 10.1%.

The share of deposits with the NBM decreased by 3.4 percentage points compared to the end of the previous year, due to a decrease in the required reserves held by banks from 32% to 26%; the share of liquid securities decreased by 1.3 percentage points; and the share of cash decreased by 1.3 percentage points. At the same time, the share of net interbank funds increased by 6.0 pp.

Liquidity principle III, which is the ratio between the adjusted actual liquidity and the required liquidity on each maturity band and which should not be less than 1 on each maturity band, has also been complied with by all banks, ranging from 1.69 on the maturity band up to one month inclusive up to 120.89 on the maturity band between one month and three months inclusive.

The liquidity coverage ratio in the sector amounted to 358.5% (limit ≥ 70% - starting with January 1, 2021) and ranged from 187.1% to 792.7%, increasing by 40.5 pp compared to the end of the previous year.

According to the reports presented by banks as of 31.12.2021, the total capital ratio in the banking sector registered a value of 25.9%, decreasing by 1.4 pp compared to the end of the previous year and ranged between 18.9% and 46.9%. All banks observed the total capital ratio (≥10%).

Also, all banks observed the total capital ratio, considering capital buffers. At the same time, in two banks (as of 31.03.2021 and 31.07.2021 - one bank, and as of 30.04.2021 and 31.05.2021 - one bank), the total capital ratio, including buffers, was lower than the OCR requirement (overall capital requirement, consisting of the sum of the total SREP capital requirement (TSCR) and capital buffer requirements). The temporary use of the capital conservation buffer at the respective dates is not considered a breach, according to Decision of the Executive Board of the NBM No. 91 of April 3, 2020.

As of 31.12.2021, the total own funds amounted to 15.2 billion lei and increased by 11.2% (1.5 billion lei), mainly due to the inclusion of eligible profit in the calculation of own funds by some banks.

As of 31.12.2021, banks complied with prudential indicators regarding large exposures and exposures to their affiliates.

At the same time, in one bank, the ratio between the aggregate value indicator of credit exposures to customers or a group of related customers, which is the first ten credit exposures by size, and the total loan portfolio is higher than the prudential limit of 30%. As long as the bank complies with the additional own funds requirement for that surplus, exceeding the 30% limit is not a breach.

During 2021, to apply the provisions of Law No 202/2017 on the activity of banks, the National Bank of Moldova amended the following acts:

- Regulation No. 109/2018 on own funds of banks and capital requirements. The changes aimed at specifying some aspects related to the inclusion of intermediate or end-of-year profits in the common equity Tier 1 capital. Thus, it was specified that, for the intermediate and non-audited year-end profits, the results of the audit should be recorded in an audit report on the financial statements showing that the given profits were adequately reflected by the bank in accordance with the accounting framework principles.

At the same time, the provisions regarding the approval of the NBM in the context of distributions were adjusted, namely the need to obtain approval for profit distributions to shareholders and/or payment of interest to holders of additional Tier 1 own funds instruments if the NBM considers that this will not lead to non-compliance with own funds requirements or other prudential indicators or to jeopardizing the bank's stability.

- Regulation No. 322/2018 on the banking activity management framework, approved by the Decision of the Executive Board of the National Bank of Moldova.

These changes were determined by the need to establish a comprehensive regulatory framework for the implementation of the Internal Liquidity Adequacy Assessment Process (ILAAP) in banks, the establishment of provisions for the calculation methodology for potential changes in the economic value of the bank as a result of the change in interest rates (IRRBB), as well as the establishment of the method of informing the National Bank of Moldova on the convocation of the general meeting of shareholders.

Aligning the banking legislation of the Republic of Moldova with international standards by improving the quantitative and qualitative mechanisms of bank management contributes to promoting a secure and stable banking sector, increasing the transparency, trust, and attractiveness of the domestic banking sector for potential investors and creditors of banks, customers, including depositors, as well as the development of new financial products and services.

- Regulation No. 127/2013 on holdings in bank equity and Regulation No. 292/2018 on requirements regarding the members of the governing body of the bank, of financial holding company or mixed holding, heads of a branch of a bank from another state, persons holding key positions, and the liquidator of the bank in the liquidation process.

These amendments concern the way the NBM’s approval is obtained for the acquisition of shares in a bank or the appointment by the bank of members of the bank's governing body, heads of a branch of a bank from another state, and persons holding key positions. Thus, the respective approvals can be obtained not only on paper but also in electronic form, through the Web portal of the NBM Information System.

According to the Law on electronic signature and electronic document, if the applicant possesses a public key certificate, he or she may submit the documents required to obtain NBM approvals in electronic form. To obtain the right to submit the application, and necessary documents and information, the applicant or the authorized person must register as a user on the NBM Web portal in accordance with the User’s Guides to the NBM Information System Web portal.

The possibility to obtain, in electronic form, the NBM’s approvals for the acquisition of shares in a bank as well as for the appointment by the bank or the branch from another state of members of the bank's governing body, heads of the branch of the bank from another state, and persons holding key positions will reduce costs, effort, and time, and streamline the process for both the applicant and the NBM.

The electronic application form will make the process more environmentally friendly and will also provide enhanced measures to protect the health of NBM applicants and employees in pandemic conditions.

- Regulation No. 46/2020 on outsourcing of bank’s activities and operations and Regulation No. 118/2018 on external audit of banks.

Changes were determined by the need to increase efficiency of the audit of outsourced activities of material importance related to the processing of payments with payment cards (p.44(4) of Regulation No. 46/2020 on outsourcing of bank’s activities and operations, adjustment of the normative acts of the National Bank of Moldova to the rule in Art.50(7) of Law No. 271/2017 on audits of financial statements and of Regulation No 118/2018 on external audit of banks to the rule in Art.88(6) of Law No. 1134/1997 on joint stock companies.

Thus, the changes made included:

- changes related to criteria for the approval of the audit company during the annual audit of payment processing activities with payment cards in the context of p. 44(4) of Regulation No. 46/2020;

- adjustment of the normative acts of the National Bank of Moldova in the context of Art. 50(7) of Law No. 271/2017 on audits of financial statements, in respect of the exclusion of qualification certificates of the auditor of financial institutions (repeal of the Regulation on issuing the qualification certificate of the auditor of financial institutions and p. 5(3)(b)) of Regulation No. 118/2018);

- adjustment of Regulation No. 118/2018 (amendment of p.23 of the Regulation) in the context of Art.88(6) of Law No. 1134/1997 on joint stock companies, in respect of the limitation of audit companies that carry out the audit of annual financial statements of the bank to conclude other contracts with the bank regarding the audit for other purposes;

- additions to Regulation No. 118/2018, relating to the facilitation by the bank of the audit company’s timely submission to the National Bank of Moldova of complete documents and information after the performance of the annual financial audit at the bank.