Welcome to the official website of the National Bank of Moldova!

×

Do you have good eyesight and want to turn this tool off?

Welcome to the official website of the National Bank of Moldova!

You can choose one of the most popular reports from the list:

National Bank and the members of its decision-making bodies shall be independent in exercising the tasks conferred upon them by law, and shall neither seek nor take instructions from public authorities or from any other authority.

In order to ensure and maintain price stability over the medium term, the National Bank’s aim will be to keep inflation (measured by Consumer Price Index) at the level of 5.0 percent annually with a possible deviation of ± 1.5 percentage points, considered to be optimal for growth and development of Moldova's economy over the medium-term.

Financial stability is achieved by strengthening the resilience of the financial system, limiting the contagion effect and reducing the accumulation of systemic risks, thus contributing to the sustainability of the financial sector and economic growth.

National Bank shall have the exclusive right to issue on the territory of the Republic of Moldova banknotes and coins as legal tender, as well as commemorative and jubilee banknotes and coins as legal tender and for numismatic purposes.

National Bank is exclusively responsible for the licencing, supervision and regulation of financial institutions activity.

National Bank of Moldova acts as banker and fiscal agent of the State and shall receive from state bodies economic and financial information and documents, which are necessary for carrying out its tasks.

National Bank of Moldova is an autonomous public legal entity and is responsible to the Parliament.

National Bank shall inform the public on the monetary policy strategy on the results of the macroeconomic analysis, the evolution of the financial market and on statistics, including with regard to monetary supply, crediting, balance of payments and the state of the foreign exchange market.

National Bank of Moldova is responsable for the compilation of the balance of payments, international investment position and the statistics of the external debt of the Republic of Moldova.

The National Bank of Moldova (NBM) has continued promoting reforms to strengthen the banking sector and improve the banking regulatory and supervisory framework. An increased attention has been paid to the aspect of shareholders' transparency in order to establish a robust corporate governance in the banking sector, attract investors meeting "fit and proper" requirements, identify bank’s related parties and ensure adequate risk management.

As of June 30, 2018, 11 banks licensed by the National Bank of Moldova, including four subsidiaries of foreign banks and financial groups, operated in the Republic of Moldova.

In the first half of 2018, two new strategic shareholders entered the banking sector of Moldova: Banca Transilvania of Romania became an indirect shareholder of the C.B. "VICTORIABANK" S.A., whereas Intesa Sanpaolo became a sole shareholder of the C.B. "EXIMBANK" S.A, the latter becoming part of the Intesa Sanpaolo Group.

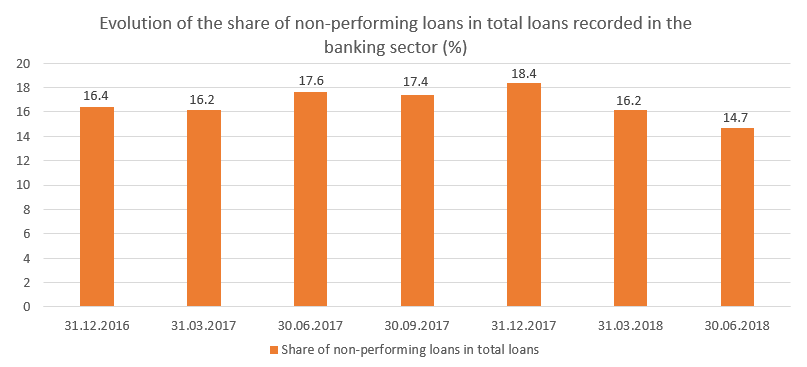

During the reference period, the banking sector has continued to accumulate assets, deposits and capital, thus enabling banks to cover the risks arising from their activity. The banking sector has also recorded high liquidity and profitability. Although, compared to the end of the previous year, the banking sector recorded a decline in the lending activity, the loan portfolio has been increasing monthly since March 2018. The share of non-performing loans in the loan portfolio has diminished, but still records high values; as a result, banks has continued pursuing the strategy of decreasing the share of non-performing loans.

Having identified signs to indicate the lack of transparency in the banks’ shareholder structures as well as the banks’ engagement in high-risk credit operations, the National Bank of Moldova, in accordance with the provisions of the Law on Financial Institutions, imposed on 11.06.2015 special supervision measures on the activity of the three banks: C.B. "MOLDOVA-AGROINDBANK" S.A., C.B. "VICTORIABANK" S.A. and C.B. "MOLDINDCONBANK" S.A. Once with the implementation of changes in the local legislation, the special supervision was replaced by an intensive supervision, whereas the C.B. "MOLDINDCONBANK" S.A. was moved, on 20.10.2016, from the intensive supervision to an early intervention regime. The above-mentioned banks jointly hold 65.7% of total banking sector assets.

At the same time, to prevent the banks from getting exposed to excessive risks, the activity of banks to which the intensive supervision and early intervention measures were applied has been daily monitored by the NBM. Given the above, the financial situation of these banks, their transactions, the agenda of the management bodies’ meetings, etc. are being constantly reviewed.

It should be mentioned that following an audit carried out by an international audit firm, which identified that the C.B. "MOLDOVA-AGROINDBANK" S.A., C.B. "VICTORIABANK" S.A. and C.B. ,,MOLDINDCONBANK" S.A. had been involved in transactions with their related parties, the NBM’s Executive Board, through its decisions of April 26, 2018, issued a list of entities qualifying as the banks’ related parties. The three banks submitted to the NBM their remedial action plans on the steps to be taken to ensure their compliance with the prudential limits set for exposures to related parties as well as the improvement of their internal control systems for the identification and monitoring of related parties, which were examined and approved by the NBM.

C.B. „VICTORIABANK” S.A.

In the first semester of 2018, a number of changes took place in the shareholding structure of the C.B. "VICTORIABANK" S.A. after two blocks of shares of 39.2% and 5.42% were sold at the auctions that took place on the regulated market of the Stock Exchange of Moldova on 16 January 2018 and 26 April 2018. As a result, Banca Transilvania, the second largest bank of Romania, became VICTORIABANK’s investor through the Dutch company “VB Investment Holding B.V.” Following the transactions, “VB Investment Holding B.V.”, holding a share of 27.56% as VICTORIABANK’s investor since 24.05.2016, in partnership with Banca Transilvania of Romania and the European Bank for Reconstruction and Development, currently own 72.19% of the bank's stock. In addition, changes have also occurred in the composition of the Administrative Board of the bank, four new members of the Board being approved by the NBM.

C.B. „MOLDOVA–AGROINDBANK” S.A.

Earlier, the National Bank of Moldova identified two groups of shareholders of the C.B. "MOLDOVA-AGROINDBANK" S.A., which, by acting in concert, acquired a qualifying holding of 43.1% in the bank's share capital, having received no prior written approval of the NBM for such acquisition. As a result, the shares were to be disposed of within a three-month period. As the shares had not been disposed of within the set time limit, they were cancelled, the new stock being issued instead. Thus, two blocks of shares were put up for sale on the Stock Exchange of Moldova, the sales period being extended several times. On 19.06.2018, the Executive Board of the National Bank of Moldova granted to an international consortium of investors (EBRD, Invalda INVL, Horizon Capital) its prior approval for the acquisition of the 41.09% stake in the bank's share capital. As a result, in June 2018, the Public Property Agency, on behalf of the Government of the Republic of Moldova, signed with the consortium a pre-contract for the sale of 41.09% stake issued by the C.B. ,,MOLDOVA-AGROINDBANK" S.A. The blocks of shares with total value of 450 million lei were purchased on 18.07.2018 by the Public Property Agency. Subsequently, within a three-month period, the Public Property Agency will put up for sale on the regulated market the new stock issued by the bank, to be sold through a public auction as a single block of shares. It should be noted that equal bidding conditions will be ensured for both the proposed acquirer, the signatory of the pre-contract, and other eligible proposed acquirers (to participate in the auction subject to the NBM’s prior permission).

C.B. „MOLDINDCONBANK” S.A.

Currently, the C.B. "MOLDINDCONBANK" S.A. operates under an early intervention regime that was imposed on October 20, 2016 after finding out that a group of persons acting in concert had acquired and became the holder of a qualifying holding of 63.89% in the bank's share capital. No prior written approval was obtained from the NBM for this acquisition, this resulting in the violation of the provisions of the Law on Financial Institutions.

In January 2018, having cancelled the above-mentioned block of shares, the bank issued and put up for sales the new stock accounting for 63.89% of the bank's share capital, the initial selling price of which was set by an international audit company. The new stock was put up for sale as a single block of shares to be sold during a three-month period. Subsequently, on July 11, 2018, the NBM’s Executive Board decided to extend its sale period for another three months.

Besides, on July 11, 2018, the NBM decided to extend the mandate of the bank’s interim administrators for another three months until 20.10.2018.

Currently, all three banks follow their normal operating routines providing full range of services, including those related to deposits, lending and settlement operations.

Following on-site full-scope inspections carried out by the NBM, the central bank imposed sanctions on several banks. Thus, the NBM’s Executive Board decided to impose a fine on the C.B. "Banca de Finanţe şi Comerţ" SA in the amount of 362.1 thousand lei, to impose a warning on the C.B. "EuroCreditBank" SA, and to impose a fine on the C.B. "COMERTBANK" SA and the members of its Board in a total amount of 2.25 million lei. Since breaches identified have not caused the banks to exceed their prudential limits and do not represent a major risk to their financial stability, they continue to follow their normal operating routines.

Following the assessment conducted by the central bank, the NBM's Executive Board, at its meeting held on March 21, 2018, decided to apply sanctions on the direct holder of a qualifying holding of 4.92% in the share capital of C.B. "ENERGBANK" S.A. for its non-compliance with the requirements regarding a shareholder’s suitability and financial soundness, stipulated in art. 48 of the Law no. 202 of 06.10.2017 on the Banking activity. Given the above, the aforementioned shareholder was informed, in the manner provided by the law, on the incidence of the provisions of art. 52 par. (1) (a), par. (2), (3) of the Law on the Banking activity leading to the suspension of the exercise of its voting rights, the right to convene and hold General Shareholders Meetings, the right to put issues on the agenda, the right to nominate candidates for the members of the management body, attached to the shares held in the share capital of the C.B. "ENERGBANK" S.A.

Following modifications implemented in the legislation in force, whereby the NBM was conferred upon the right to presume banks’ related parties using a set of presumption criteria, the central bank verified, as part of its off-site inspections, banks’ transactions with their related parties. Consequently, in July 2018, the NBM identified in its decision the related parties of four banks, requesting those banks to develop and submit their remedial action plans listing measures to be applied that would improve their related party identification and monitoring processes.

As of 31 March 2018, based on the report data submitted by licensed banks, the situation in the banking sector was characterised by the following trends:

Assets and liabilities

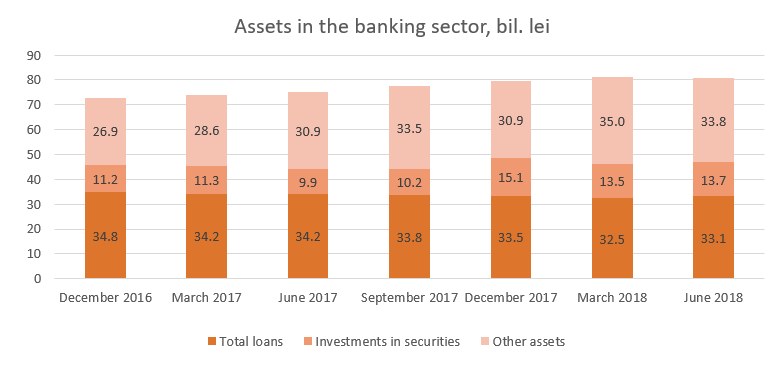

Total assets recorded 80.6 billion lei, increasing by 1.5% (1.2 billion lei) during the first semester of 2018.

As of 30.06.2018, the balance of the gross loan portfolio accounted for 41.1% of total assets or 33.1 billion lei, having decreased by 1.0% (327 million lei) during the first semester of 2018. At the same time, the volume of new loans extended during the reference period increased by 11.6%, year-on-year. against the background of a decrease in lending interest rates as one of the growth factors.

In addition, in March-June 2018, monthly increases in the loan portfolio were recorded, the consumer and real estate loans recording the largest increases.

Investments in securities (certificates of the National Bank of Moldova and government securities) accounted for 17.1% of total assets, having decreased by 1.9 pp. compared to the end of 2017.

Other assets accounting for 41.8% are kept by banks in accounts opened with the NBM, with other banks, in cash, etc.

During the first semester of 2018, the share of non-performing loans (substandard, doubtful and compromised) in total loans decreased by 3.7 pp. compared to the end of 2017, recording 14.7% as of 30 June 2018. It should be noted that this indicator varies across the banking sector, ranging from 5.7% to 34.3%. This progress has been achieved through measures that were applied by banks to develop and implement their own strategies to reduce the volume of non-performing loans, to transfer non-performing loans to third parties, to sell collaterals, to cooperate with specialised real estate agencies with a view to identifying potential buyers for pledged / mortgaged assets, etc.

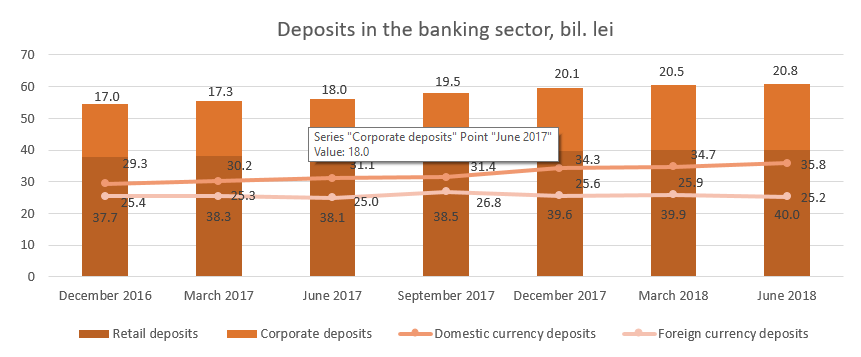

During the first semester of 2018, the banking sector continued to record an upward trend in the balance of deposits. According to prudential reports, it increased by 1.7% in the reference period, amounting to 60.9 billion lei (retail deposits accounting for 65.6% of total deposits, corporate deposits – for 33.8% and deposits of banks – for 0.3%). The increase in corporate deposits by 690.0 million lei (3.4%) had the biggest impact on the growth of the balance of deposits. The balance of retail deposits has also increased by 371.3 million lei (0.9%).

Domestic currency deposits accounted for 58.7% of total deposits, their balance increasing by 1.5 billion lei (4.6%), thus amounting to 35.8 billion lei as of 30.06.2018. Foreign currency deposits accounted for 41.3% of total deposits, their balance growing by 460.9 million lei (1.8%) and totalling 25.2 billion lei.

Compliance with prudential requirements

Banks continue to maintain high liquidity ratios. Thus, the value of the long-term liquidity indicator (1st liquidity principle) recorded 0.6 (with threshold of ≤1), a level equal to the one of the end of 2017. Current liquidity for the sector (2nd liquidity principle) recorded insignificant changes, recording 55.6% (with threshold of ≥20%), meaning that more than a half of the banking sector's assets are liquid. It should be mentioned that the largest shares in total liquid assets are held by deposits with the NBM – 40.3%, liquid securities – 30.8% and net interbank money – 18.9%. During the first semester of 2018, the share of liquid securities decreased by 3.5 pp. whereas the share of net interbank funds fell by 1.4 pp.

All banks comply with the 3rd liquidity principle reflecting the ratio between the actual adjusted liquidity and the required liquidity for each maturity band which should not be less than 1.

The risk-weighted capital adequacy ratio for the banking sector recorded 33.9%, meaning that the threshold set for all banks (≥16%) was complied with, although the ratio varied across the sector ranging between 23.8% and 89.1%.

As of June 30, 2018, the Tier I capital amounted to 11.1 billion lei, recording a 9.0% increase (912.1 million lei) during the reference period. This development was mainly determined by the profit earned in the first semester, amounting to 935.8 million lei. The amount of calculated unreserved losses was decreased for contingent assets and liabilities by 396.3 million lei. At the same time, the transition to IFRS 9 and paying out of dividends by a branch of one foreign bank have had a negative impact over the capital.

Regarding the Regulation on large exposures, it should be noted that one bank still does not comply with the prudential limit of 15% of the total regulatory capital, set by the NBM. However, the bank has developed the exposure reduction plan and meets the milestones set therein.

In addition, there is one bank that continues to breach the prudential limit of 30% set for the indicator “Report of ten largest net debts on credit and total credit portfolio and contingent liabilities included in the ten largest debts” as a result of a significant reduction of the loan portfolio of a bank. The bank was requested to develop a plan to address this issue and ensure compliance with applicable regulatory requirements.

Following the NBM’s presumption of banks’ related parties in accordance with relevant legislative changes, it was found that five banks have breached the prudential limit of 20% of the Tier I capital set for total exposure to related parties and groups of persons linked together with related parties, including three banks that breached the limit of 10% of the total regulatory capital set for the maximum exposure to a related party. Based on the NBM’s decision, the aforementioned banks submitted their remedial action plans containing measures to be applied that would ensure the banks’ compliance with applicable prudential limits as well as the improvement of their related party identification and monitoring processes. The plans were examined and approved by the NBM.

Income and profitability

As of June 30, 2018, the profits earned totalled 935.8 million lei, having increased by 2.2% compared to the same period of the previous year.

Total income amounted to 3.5 billion lei, of which interest income accounted for 62.1% (lei 2.2 billion), and non-interest income - 37.9% (1.3 billion lei). At the same time, total expenditure amounted to 2.5 billion lei, including interest expenses - 30.2% (762.7 million lei) and non-interest expenses - 69.8% (1.8 billion lei).

The decrease in profits was determined by the decrease in the interest income by 11.7% or by 285.7 million lei due to the lowering of interest rates and the reduced loan portfolio, as well as by the rise of non-interest expenses by 8.0% or by 130.6 million lei. At the same time, non-interest income increased by 14.5% or 166.5 million lei. Significant shares in non-interest income are held by income from fees and charges - 58.0%, income from foreign exchange differences - 28.9% (income from foreign currency trading and revaluation), other operating income - 13.0%.

Interest expense decreased by 23.1% or 228.9 million lei as a result of the decrease in the average deposit rate.

As of 30 June 2018, return on assets and return on capital recorded 2.2% and 13.4%, increasing by 0.3 pp. and 2.0 pp., respectively, compared to the end of the previous year.

In the first semester of 2018, once with the enactment of the Law on Banking Activity on January 1, 2018, the National Bank of Moldova approved nine regulatory acts to regulate such aspects of banking activity as banks' own funds and capital requirements, capital buffers, banks’ credit risk treatment using the standardised approach, credit risk mitigation techniques used by banks, banks’ treatment of operational risk using the basic indicator approach and the standardised approach, market risk treatment using the standardised approach, banks’ treatment of settlement / delivery risks, banks’ calculation of specific and general adjustments for credit risk, as well as the regulation on external auditing of banks. New regulations are expected to enhance lending to small and medium-sized businesses. Thus, for exposures to SMEs, the regulations provide for reduced capital requirements by establishing a 75% risk weighting factor and a deduction factor of 0.7619.

At the same time, the National Bank of Moldova approved the Guidelines on the submission by banks of COREP reports for supervisory purposes, which sets forth uniform requirements for reporting for supervisory purposes as well as specific requirements for reporting of data on own funds and risk exposures. The first reports meeting new requirements are to be submitted by banks in August 2018 and will cover own funds and capital requirements, capital buffers, etc.

The aforementioned regulations on own funds and bank’s treatment of various risks were developed under the Twinning project of the European Union aiming to strengthen the NBM’s capacity in the field of banking regulation and supervision, in cooperation with the Central Bank of the Netherlands and the National Bank of Romania.

The National Bank of Moldova continues developing regulatory acts to ensure full application of the provisions of the Law on Banking Activity no. 202 of 6 October 2017.

The alignment of the banking legislation of the Republic of Moldova with international standards by means of improving the quantitative and qualitative mechanisms of banks’ management will contribute to the promotion of a secure and stable banking sector, to an increased transparency, trust and attractiveness of the domestic banking sector for banks’ potential investors and creditors, as well as for depositors. The new framework favours the development of new financial products and services by creating a stable financial environment that ensures the financial soundness of banks and of the entire system.