Welcome to the official website of the National Bank of Moldova!

×

Do you have good eyesight and want to turn this tool off?

Welcome to the official website of the National Bank of Moldova!

You can choose one of the most popular reports from the list:

National Bank and the members of its decision-making bodies shall be independent in exercising the tasks conferred upon them by law, and shall neither seek nor take instructions from public authorities or from any other authority.

In order to ensure and maintain price stability over the medium term, the National Bank’s aim will be to keep inflation (measured by Consumer Price Index) at the level of 5.0 percent annually with a possible deviation of ± 1.5 percentage points, considered to be optimal for growth and development of Moldova's economy over the medium-term.

Financial stability is achieved by strengthening the resilience of the financial system, limiting the contagion effect and reducing the accumulation of systemic risks, thus contributing to the sustainability of the financial sector and economic growth.

National Bank shall have the exclusive right to issue on the territory of the Republic of Moldova banknotes and coins as legal tender, as well as commemorative and jubilee banknotes and coins as legal tender and for numismatic purposes.

National Bank is exclusively responsible for the licencing, supervision and regulation of financial institutions activity.

National Bank of Moldova acts as banker and fiscal agent of the State and shall receive from state bodies economic and financial information and documents, which are necessary for carrying out its tasks.

National Bank of Moldova is an autonomous public legal entity and is responsible to the Parliament.

National Bank shall inform the public on the monetary policy strategy on the results of the macroeconomic analysis, the evolution of the financial market and on statistics, including with regard to monetary supply, crediting, balance of payments and the state of the foreign exchange market.

National Bank of Moldova is responsable for the compilation of the balance of payments, international investment position and the statistics of the external debt of the Republic of Moldova.

Pursuant to its commitments to development partners, the National Bank of Moldova continues to reform the banking sector, focusing mostly on the transparency of shareholders and increase of attractiveness for new investors, assessment of bank management sustainability and identification of transactions concluded with the bank’s related parties. These efforts will also be encouraged by the transition from Basel I to Basel III. As a result, the banks will improve their corporate governance system and activity management framework.

At the same time, the National Bank asked banks to carry out exhaustive external IT audit to ensure information security, client/bank protection from potential frauds, and prevention from cyber-attacks.

On 30.06.2017, there were 11 banks licensed by the National Bank of Moldova (the NBM), including 4 subsidiaries of foreign banks and financial groups.

During the first semester of 2017, the assets of the banking sector continued to increase; banks became more resilient, strengthening their capital and maintaining a high level of liquidity and profitability. Also, non-performing loans recorded a slight increase and the lending activity maintained a downward trend (except for June, when the balance of loans recorded an increase).

Pursuant to the finding of some indicators related to shareholders’ non-transparency structure and engagement in high-risk lending operations and to the Law on Financial Institutions, the National Bank of Moldova placed 3 banks under special supervision procedure (BC “MOLDOVA-AGROINDBANK” S.A., B.C. “VICTORIABANK” S.A. and BC “Moldindconbank” S.A.) from 11.06.2015. Due to the amendment of the legislation, special supervisions was replaced by intensive supervision and on 20.10.2016, intensive supervision placed on BC “Moldindconbank” S.A. was replaced by early intervention. It should be noted that these 3 banks hold 65.0 percent of total assets of the banking sector.

In June 2015, the National Bank of Moldova recommended the banks concerned to employ an audit company who would carry out a diagnosis survey. Following the diagnosis survey, the National Bank of Moldova adopted in June 2016 decisions on the elaboration of the Remedial Action Plan for BC “MOLDOVA-AGROINDBANK” S.A. and B.C. “VICTORIABANK” S.A., obliging the banks to remove all identified gaps until the end of 2016. To this end, the banks took a range of measures to improve the main fields of activity, as follow: monitoring of shareholders and bank’s related parties, corporate governance, lending activity, risk management, money laundry activity, IT and etc.

During on-site controls carried out in the first quarter of 2017 at BC “MOLDOVA-AGROINDBANK” S.A. and BC “VICTORIABANK” S.A. it was verified the level of achievement of the Action Plan on removing gaps found following the diagnosis survey. As a result of these controls, the National Bank adopted some decisions (described below) concerning the aforementioned banks.

In June 2017, B.C. “MOLDOVA – AGROINDBANK” S.A., B.C. “VICTORIABANK” S.A. and BC “Moldindconbank” S.A. were asked to hold a competition and to nominate an independent audit company which would identify the transactions concluded with the related parties of the aforementioned banks. The National Bank of Moldova is the receiver of reports concerning the identification of transactions concluded with the related parties of the aforementioned banks. Following the competition and by mutual agreement, the audit company that would identify the transactions concluded with the bank’s related parties was nominated, but the preliminary results of the survey would be completed by late August 2017.

BC „MOLDOVA – AGROINDBANK” S.A.

According to the finding of the National Bank of Moldova of two groups of shareholders of BC “MOLDOVA-AGROINDBANK” S.A. who acted in concert and purchased a substantial holding in the share capital of the bank amounting to 43.1 percent, without prior permission in writing of the National Bank, they were about to alienate purchased shares within 3 months. Due to the fact that the aforementioned shares had not been alienated in the established deadline, they were cancelled and new ones were issued. Thus, two new unique shares package were put up for sale on Moldova’s Stock Exchange until June 2017. On 20.06.2017, the National Commission of Financial Market extended the deadline for selling the bank’s newly issued shares by 6 months. It should be noted that many potential investors were interested in purchasing these share packages.

Over the first quarter of 2017, BC “MOLDOVA-AGROINDBANK” S.A. underwent an exhaustive control during which the achievement of the Action Plan on removal of gaps found during the diagnosis survey was verified. On 29.06.2017, the Executive Board of the NBM approved the Decision on the results of the exhaustive control, pursuant to which six members of the Management Committee of B.C. “MOLDOVA-AGROINDBANK” S.A. received a warning and a fine while the members of the Board were penalized with a warning.

The penalties were applied following the finding of some violations of the Law on Financial Institutions and the NBM’s regulatory acts, referring mostly to non-compliance by banks with lending-related prudential requirements, risk concentration, assets classification and etc.

Also, the National Bank recommended BC “MOLDOVA - AGROINDBANK” S.A. Management Board and Committee to improve the lending-related internal control system and to develop and apply an action plan on removal of gaps found during the on-site exhaustive control carried out at the bank.

B.C. „VICTORIABANK” S.A.

The NBM pays close attention to shareholders’ transparency and assets classification within the intensive supervision of BC “VICTORIABANK” S.A. To this end, the NBM started the assessment procedure of shareholders with substantial holdings in the capital of B.C. “VICTORIABANK” S.A. As a result, some holders of the share capital of B.C. “VICTORIABANK” S.A. were penalized with fines in March 2017.

In the first quarter of 2017, the exhaustive control of the banks’ activities ended and the NBM’s Executive Board will shortly approve the Decision on the control’s results.

BC „Moldindconbank” S.A.

Currently, BC “Moldindconbank” S.A. is under early intervention supervision which started on 20.10.2016, due to the finding of a concerted activity of a group of persons who purchased and held a substantial holding in the share capital of the bank amounting to 63.89 percent, without prior permission in writing of the NBM, thus violating the provisions of the Law on Financial Institutions.

By the Decision of 20.10.2016, the NBM nominated temporary administrators of BC “Moldindconbank” S.A. It should be noted that by the NBM’s Executive Board Decision of 19.07.2017, the National Bank extended by 3 months the term of office of temporary administrators of BC “Moldindconbank” S.A., up to 20.10.2017.

At the same time, by Decision of 20.10.2016, the NBM asked the bank to employ an audit company who would perform the assessment of assets, debts and own capital. Subsequently, by the Decision of the NBM’s Executive Board of 13.04.2017, it was ordered the update of the aforementioned assessment and submission of the final report to the NBM. The final assessment report will shortly be submitted to the NBM.

Also, as a result of on-site controls carried out over the previous year at BC “Moldindconbank” S.A., the Executive Board of the National Bank decided on 13.04.2017 to penalize with fines 11 former administrators of B.C. “Moldindconbank” S.A. Also, the National Bank obliged BC “Moldindconbank” S.A. to form additional provisions and allowances for a range of assets and contingent liabilities of the bank, to strengthen credit and liquidity risk management, to ensure the maintenance of risk-weighted capital adequacy ratio above 20 percent, to revise bank’s internal regulations aiming to improve them, etc.

The bank’s activity was subject to exhaustive control from April 2017 to June 2017. Currently, the preliminary report on the results of the exhaustive control is being drafted.

As at 30.06.2017, the situation of the banking sector, based on the reports submitted by licensed banks, recorded the following trends:

Assets and liabilities

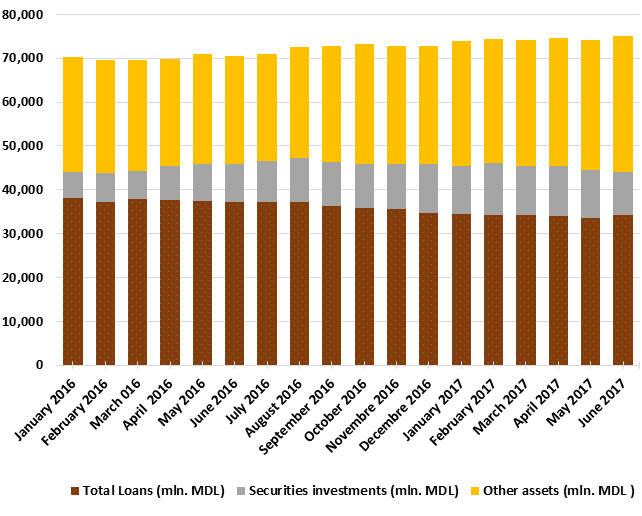

Total assets made up MDL 75 billion, increasing by 3 percent (MDL 2.2 billion) over the first semester of 2017, mostly, on the account of the increase in liquid assets.

As at 30.06.2017, gross loan portfolio accounted for 45.6 percent of total assets or MDL 34.2 billion, decreasing by 1.6 percent (MDL 544.7 million) over the first semester of 2017. The banks shall emphasize their role of leader on the real economy’s financing, paying special attention to SMMs, agriculture, industry and innovation.

Investments in securities (certificates of the National Bank and state securities) recorded a share of 13.2 percent of total assets, by 2.1 percentage points less than in late 2016 due to the decrease of the base rate from 9 percent to 8.0 percent on the certificates of the National Bank.

The rest of assets, which makes up 41.2 percent, is maintained by banks in accounts opened with the National Bank, other banks, in cash and etc.

Over the first semester of 2017, the share of non-performing loans (substandard, doubtful and compromised) in total loans increased by 1.2 percentage points compared with late 2016, making up 17.6 percent on 30.06.2017. This indicator varies among banks and the highest one amounts to 32.5 percent.

Most non-performing loans were influenced by two banks under intensive supervision, predominantly, as a result of reclassification of loans by categories of non-performing risk following the NBM controls and the external audit.

At the same time, the National Bank of Moldova requested banks to elaborate strategies on the decrease of non-performing assets and their ongoing monitoring to reduce the level of non-performing loans.

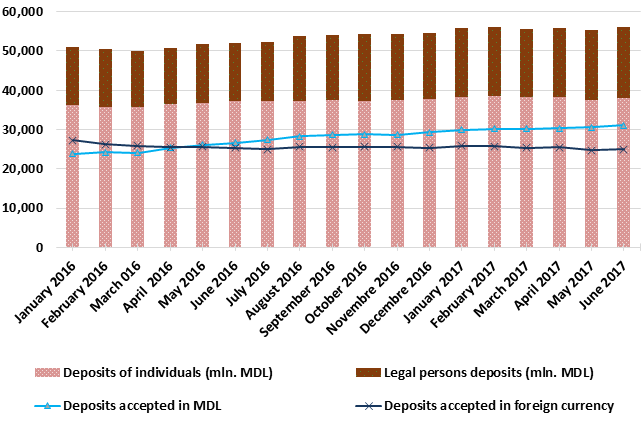

In the first semester of 2017, the balance of deposits in the banking sector continued to increase. According to prudential reports, it increased by 2.4 percent in the reference period, accounting for MDL 56.2 billion (deposits of individuals accounted for 67.8 percent of total deposits, deposits of legal entities made up 32 percent and deposits of banks – 0.2 percent). The increase by MDL 956.6 million (5.6 percent) of deposits of legal entities and deposits of individuals by MDL 461.5 million (1.2 percent) had the biggest impact on the increase of deposits. At the same time, the balance of bank deposits decreased by MDL 77.3 million (45 percent).

Compliance with prudential requirements

The banks maintained the liquidity indicators at a high level. Thus, the long-term liquidity indicator value (principle I of liquidity) accounted for 0.6, keeping almost to the level recorded in late 2016. Current sector liquidity (principle II of liquidity) increased by 2.0 percentage points, amounting to 51.3 percent. Thus, more than half of banking sector assets are concentrated in liquid assets. It should be noted that the biggest increase of liquid assets over the first semester of 2017 of 30.5 percent and 18.3 percent respectively was recorded for cash and accounts opened with the NBM, following the increase of required reserves ratio.

High level of risk-weighted capital adequacy ratio (average per sector - 29 percent, regulated limit for each bank ≥16 percent) allowed banks to absorb losses related to the worsening of loan quality. Also, all banks comply with the regulated limit, which varies from 21.6 percent to 118.1 percent; for some banks, capital consolidation is still a priority.

As at 30.06.2017, Tier I capital accounted for MDL 9.5 billion and over the first semester of 2017 it recorded an increase of 2.3 percent (MDL 217.4 million). The increase of Tier I capital was mostly driven by the profit of MDL 956.7 million. At the same time, the following factors had a negative influence on the capital increase: increase by MDL 335.3 million of calculated but unreserved value for losses on assets and contingent liabilities; formation by the bank of additional allowances to assets in the amount of MDL 191.9 million following the external audits and the NBM controls; decrease by MDL 50.9 million of undistributed profit by a bank following free assignment of treasury shares to some shareholders; distribution by a bank (subsidiary of a foreign bank) of dividends amounting to MDL 163.2 million.

It should be noted that the NBM requested banks to adopt a more prudent and conservative policy concerning distribution of dividends.

According to the reports submitted as at 30.06.2017, the banks comply with the Regulation on bank’s related parties. Also, it should be noted that two banks exceed the limit set by the NBM in relation with the Regulation on “large” exposures. One bank is still violating the 15 percent limit of total regulatory capital related to maximum exposure; however, this bank has a plan of exposure mitigation, in compliance with the deadlines set out in the plan. Another bank violates the exposure ratio to shareholders who manage, directly or indirectly, less than 1% of the share capital of the bank, including their related parties, in total regulatory capital of the bank (regulated limit ≤20%, reported from 30.06.2017).

Income and profitability

On 30.06.2017, the financial exercise-related profit summed up MDL 956.7 million, increasing by 12.0 percent compared with the same period of the previous year. The obtaining of profit and its increase during the referenced period will allow banks to incur additional expenses related to Basel III implementation.

Profit increase is driven by the decrease by 39.9 percent of expenses on interest (from deposits), decrease by 76.6 percent of allowances on financial assets and the increase by 5.4 percent of interest non-related income (mostly, due to fees and taxes by 11.8 percent).

On 30.06.2017, assets and capital profitability accounted for 2.4 percent and 14.6 percent respectively (up by 0.6 and 3.5 percentage points respectively).

On 13 July 2017, the Parliament passed the draft Law on banks’ activity in first reading, which will strengthen banking regulation and supervision framework, by alignment to European standards (transition from Basel I to Basel III).

In the first semester of 2017, following public consultation, the draft Law on banks’ activity was subjected to compatibility testing with the community’s legislation, anticorruption and legal examination, and was approved by the Government. The approval of the draft law in final reading by the Parliament is scheduled for autumn session (October/November 2017) and entry into force – for 01 January 2018 (however, it will gradually be implemented until 2020). Once the new banking law and the secondary regulatory framework, based on which the provisions of the law will be implemented (more than 20 regulations), enter into force, the conditions set forth in the Association Agreement between the RM and EU will be complied with.

All aforementioned regulations have been developed within the Twinning project on the NBM’s capacity building for banking regulation and supervision, financed by the EU. The NBM, together with the Central Banks of Romania and the Netherlands, has aligned the legislation of the Republic of Moldova to the provisions of Directive 2013/36/EU and Regulation 575/2013 (CRD IV).

Proper implementation of the new requirements and the modern and efficient prudential regulation and supervision framework will strengthen banking sector’s resistance, will reduce bank’s likelihood of bankruptcy, protecting the interests of depositors.

It should be noted that the new regulatory framework will keep some current prudential provisions and will focus, predominantly, on building internal corporate governance and risk management practices in banks. Also, there will be introduced new approaches on the calculation of regulated capital, risk-weighted capital adequacy (which, will include, besides loan risk, other risks too – operational, market and other risks related to the banking activity) and liquidity ratios. Additionally, banks shall have the possibility to choose the approach for calculating capital adequacy rate (standard or advanced). Also, there will be new elements, such as the leverage rate, the capital depreciation, the internal capital adequacy assessment process (ICAAP) and the internal liquidity adequacy assessment process (ILAP), disclosure requirements.

With the implementation of the law, the National Bank of Moldova will carry out a fundamental review of the banking supervision system, using the supervisor’s arguments based on risk, provisioning and approach (SREP). The NBM will have more instruments to apply the supervision and remedial measures. Prudential supervision will be carried out based on a strong and tight cooperation with foreign supervisors (including participation in supervision panels) and other competent authorities.

The National Bank approved the new Regulation on administration framework of bank’s activity, thus ensuring a gradual transition to the new Basel III framework. In this regard, licensed banks developed Basel III implementation plans (some even contracted international advisors asking for their assistance). It should be noted that the National Bank of Moldova improves its supervision practices aiming to align them to new standards.

At the same time, Basel III standards-based framework will allow the alignment of the legislation in field of the Republic of Moldova with international applicable standards, will contribute to the attractiveness to foreign investors, development of new financial products and services, having more safe and strong banks playing a leading role in the country’s economy.

In conclusion, the new legislation will make banking system stronger and will ensure financial stability in the Republic of Moldova.