Welcome to the official website of the National Bank of Moldova!

×

Do you have good eyesight and want to turn this tool off?

Welcome to the official website of the National Bank of Moldova!

You can choose one of the most popular reports from the list:

National Bank and the members of its decision-making bodies shall be independent in exercising the tasks conferred upon them by law, and shall neither seek nor take instructions from public authorities or from any other authority.

In order to ensure and maintain price stability over the medium term, the National Bank’s aim will be to keep inflation (measured by Consumer Price Index) at the level of 5.0 percent annually with a possible deviation of ± 1.5 percentage points, considered to be optimal for growth and development of Moldova's economy over the medium-term.

Financial stability is achieved by strengthening the resilience of the financial system, limiting the contagion effect and reducing the accumulation of systemic risks, thus contributing to the sustainability of the financial sector and economic growth.

National Bank shall have the exclusive right to issue on the territory of the Republic of Moldova banknotes and coins as legal tender, as well as commemorative and jubilee banknotes and coins as legal tender and for numismatic purposes.

National Bank is exclusively responsible for the licencing, supervision and regulation of financial institutions activity.

National Bank of Moldova acts as banker and fiscal agent of the State and shall receive from state bodies economic and financial information and documents, which are necessary for carrying out its tasks.

National Bank of Moldova is an autonomous public legal entity and is responsible to the Parliament.

National Bank shall inform the public on the monetary policy strategy on the results of the macroeconomic analysis, the evolution of the financial market and on statistics, including with regard to monetary supply, crediting, balance of payments and the state of the foreign exchange market.

National Bank of Moldova is responsable for the compilation of the balance of payments, international investment position and the statistics of the external debt of the Republic of Moldova.

The National Bank of Moldova continues to promote the reforms implemented for the development of a stable and transparent banking sector that would assure the basis for the national economic growth.

As of 31.12.2018, 11 banks licensed by the National Bank of Moldova operated in the Republic of Moldova. In accordance with the banking supervision priorities and the commitments assumed towards the development partners in strenthening the transparency of the shareholders structure for the banks, significant changes, related to acquisition of shares in the capital of certain banks by several reputable international groups, were made in 2018. As a result, more than 70% of the banks assets are being managed by international groups with sound reputation.

Therefore, changes in the ownership structure were made at the following banks:

2018 was a year marked by the entry into force, on the 1 January, of the Law on banks’ activity, which modernised the regulation and supervision standards in the banking sector. The above-mentioned law extended the rights and duties of the National Bank of Moldova (NBM) in the process of evaluation and supervision of the banks. At the same time, the law provided improvements in the corporate governance framework of the banks and their obligation to hold adequate share capital in relation to the assumed risks, which allows the harmonization process of the national banking legislation with international principles and standards.

In this context, starting with 30 July 2018, the banks submitted their first COREP reports in accordance with BASEL III requirements. According to these reports, the own funds ratio was within the limits forecasted by the NBM and higher than the minimum of 10% and the buffers combined. Therefore, the new reporting framework provides the calculation of requirements for own funds based on a new methodology that reflects not only the impact of credit risk, but also the market and operational risks. Concomitantly, additional requirements for the own funds that banks must hold to constitute capital buffers had been established, with the aim to prevent and mitigate the macroprudential or the systemic risk.

Aditionally, during the twelve months of 2018, the banking sector continued the trend of consolidation of own funds (previously CNT). At the same time, banks maintained a a high liquidity and profitability level. The assets and deposits also continued to increase. The aggregate loan portfolio of the banking sector faced an increase compared to the end of the previous year and starting with March 2018, monthly increases were recorded. Even though the share of the non-performing loans in the total loan portfolios decreased during 2018, its level is still high.

On 22 August 2018, the NBM Executive Board cancelled the intensive supervision regime against BC „VICTORIABANK” S.A.

The decisions was adopted after it was established that the bank ensured the transparency of the ownership structure following the acquisition of 72.19% of the share capital of the bank by the VB “Investment Holding” B.V., a company owned by Banca Transilvania of Romania, in partnership with the European Bank for Reconstruction and Development (EBRD).

At the same time, BC „MOLDOVA-AGROINDBANK” S.A. continues to be under intensive supervision regime (since 2015), while BC „Moldindconbank” S.A. – under early intervention regime (since 2016).

As of 31.12.2018, BC „MOLDOVA-AGROINDBANK” S.A. and BC „Moldindconbank” S.A. hold together 48.3% of the total assests of the banking sector.

In order to avoid the excessive risks, the National Bank of Moldova monitors on a daily basis the activities of banks under intensive supervision and early intervention regimes. Consequently, the financial statements of these banks, their tansactions, and agendas of supervisory and executive boards are being continuously examined.

Following the legislative amendments, by decisions of the NBM Executive Board of 26 April 2018, certain parties have been qualified as related to B.C. „MOLDOVA – AGROINDBANK” S.A., BC „VICTORIABANK” S.A and BC ,,Moldindconbank” S.A., after exceeding the prudential limits for related parties exposure. Subsequently, thesebanks submitted to the National Bank of Moldova their plans for complying with the prudential limits set for related parties exposuresand on improving internal control systems for their identification and monitoring, which have been examined and accepted by the NBM. The banks report on a quarterly basis to the National Bank of Moldova about the undertaken measures. As of 31.12.2018, a bank (BC „MOLDOVA – AGROINDBANK” S.A.) complied with the prudential limits for the related parties exposures.

BC „MOLDOVA – AGROINDBANK” S.A.

In 2016, following the implementation of the monitoring process of the banks’ shareholders transparency, the National Bank of Moldova found two groups of shareholders of BC „MOLDOVA-AGROINDBANK” S.A.who acted in concert and acquired a qualifying holding in the share capital of the bank of 43.1%, without the prior written permission of the National Bank. Due to the fact that the aforementioned shares were not disposed of within the period of three months, they were canceled, and consequently, new shares were issued by the bank. Following their exposure to sale and failure to sell them within the deadline, the term had been extended several times.

In June 2018, the Executive Board of the National Bank of Moldova granted a preliminary permission to an international consortium of investors (EBRD, Invalda INVL, Horizon Capital) to purchase the 41.09% share package of the bank’s share capital. Subsequently, in July 2018, the aforementioned share package was acquired by the Agency for Public Property, and had to be exposed to sale on the regulated market as a single share package within a period of three months via outcry auction.

The single package of new issued shares of BC „MOLDOVA-AGROINDBANK” S.A. was sold on 2 October 2018 to an international investment consortium (EBRD, Invalda INVL, Horizon Capital), which helds now 41.09% of the bank’s share capital.

At the same time, on 22 November 2018, during the shareholders’ general meeting, the new members of the bank’s Supervisory Board have been elected, for a period of four years. The sets of documents of the new Supervisory board members were submitted to the National Bank and are now in the process of examination.

BC „Moldindconbank” S.A.

In October 2016, BC „Moldindconbank” S.A.was set under early intervention regime, after NBM found the concerted activity of a group of persons who acquired and held a qualifying holding of 63.89% in the share capital of the bank, without any prior written permission of the NBM. The early intervention regime still applies to BC „Moldindconbank” S.A.

According to the legislation, the aforementioned shares had to be disposed of within three months. Due to the fact that they were not sold, and consequently canceled in January 2018, the bank issued new shares, amounting to 63.89% of the bank’s share capital, which have been exposed to sale for a period of three months, as a single package, at a price set after the evaluation made by an international audit company. The deadline for sale was extended several times, while the last decision for another three months extension was taken by the NBM Executive Board on 18 January 2019. According to the Law on banks’ activity no 202 of 06.10.2017, the National Bank of Moldova may extend the three months period no more than three times consecutively.

Concomitantly, the National Bank decided to replace the President of BC „Moldindconbank" S.A., Mr. Aureliu Cincilei, a temporary administrator, by the appointing Mr. Victor Cibotaru as a temporary administrator who previously was the Vice president of the bank.

In January 2019, NBM Executive Board adopted the decision on the preliminary permission for acquisition, of more than 50% of the shares of BC „Moldindconbank" S.A., by a potential Bulgarian investor.,

The aforementioned banks operate in normal regime and provide all services, including those related to deposits, lending and settlement operations.

Following the process of making the banking ownership transparent, the NBM Executive Board adopted on 11 January 2019 two decisions on „Banca de Finanţe şi Comerţ” S.A. and BC „ENERGBANK” S.A.

Therefore, with regard to the „Banca de Finanţe şi Comerţ” S.A., the National Bank found that a group of shareholders acted in concert. They purchased and held a qualifying holding of 36.15% in the share capital of the bank, without a prior written permission of the National Bank, violating the provisions of the Law on banks’ activity. As a result, the National Bank suspended the exercise of certain rights for these shareholders (the right to vote, to convoke and organize the general shareholders meeting, to propose topics in the agenda, to nominate candidates for the banks Supervisory board, the executive board and to receive dividends). The respective shareholders shall dispose their shares within the time limits provided by the law.

With regard to the BC ”ENERGBANK” S.A., the National Bank established that a group of shareholders acted in concert and held 52.77% in the share capital of the bank, without a prior written permission of the NBM. Following these findings, the decision on the suspension of certain rights of these shareholders was adopted. Moreover, according to the law, these shareholders shall dispose their shares held in the share capital of BC „ENERGBANK” S.A.

Moreover, considering that the size of the package of suspended shares exceeded 50% of the bank’s capital, NBM has also decided to apply measures of early intervention on BC “ENERGBANK” S.A., in accordance with the Law on banks’ recovery and resolution. Supervisory and Executive Boards of the bank remained functional, however these were supplemented with temporary administrators, appointed by the NBM, to assure a prudent governance of the bank during the period of solving the deficiencies identified in the bank's ownership structure.

Following the NBM assessment, on 11.01.2019, the Executive Board of the National Bank of Moldova decided to suspend some rights of a shareholder that held 3.98% of the share capital of BC „ENERGBANK” S.A., for failing to comply with the requirements on the financial adequacy and solidity, provided in Article 48 of the Law on banks’ activity no 202 of 06.10.2017. The respective shareholder shall dispose the shares held in the share capital of BC “ENERGBANK” SA within a three months period from the date of issuence of NBM’s decision.

The aforementioned banks operate in normal regime and provide all range of services, including those related to deposits, lending and settlement operations.

Previously, pecuniary penalties have been applied towards a direct shareholder that holds 1.81% of the share capital of the BC “EuroCreditBank” S.A. and towards a direct shareholder that holds 4.92% of the share capital of BC “ENERGBANK” S.A., for failing to comply with the requirements on the financial adequacy and solidity, stipulated in Article 48 of the Law on banks’ activity no 202 of 06.10.2017. Moreover, the NBM decided to apply a penalty of MDL 179.5 thousand against two shareholders of „Banca de Finanțe și Comerț" S.A. for failing to submit the information requested by the NBM requested for assessing the quality of shareholders.

Following the verification of transactions with related parties during the off-site inspections of the banks, according to the new legislative modifications, in July 2018, the National Bank decided to qualify certain persons as related parties for four banks („Banca de Finanțe și Comerț" S.A., B.C. „COMERȚBANK” S.A., BC „EuroCreditBank” S.A., BC „ENERGBANK” S.A.) and requested action plans for the improvement of the process of identification and monitoring of related parties. Fortwo of these banks, the NBM required plans for complying with the prudential limits of exposures to related parties. As of 31.12.2018, the aforementioned banks complied to the prudential limits of exposures to the related parties.

At the same time, following the full-scope inspection conducted in 2018, the National Bank of Moldova decided to apply different sanctions against the „Banca de Finanțe și Comerț" S.A., B.C. „COMERȚBANK” S.A., some members of the executive bodies of these banks, as well as sanctions against the BC „EuroCreditBank” S.A.

Concomitantly, a warning was issued against BC "MOBIASBANCĂ-Groupe Societe Generale" S.A., in connection with the detection of some deficiencies related to the failure to comply with certain legal requirements regarding the integrity of certain data related to the performed transactions, as well as deficiencies related to the internal control system of the bank and the management framework. Therefore, the banks shall eliminate all the deficiencies that were found during the on-site controls.

As of 31.12.2018, the situation in the banking sector, which is described in the reports of the licensed banks, showed the following trends:

Assests and liabilities

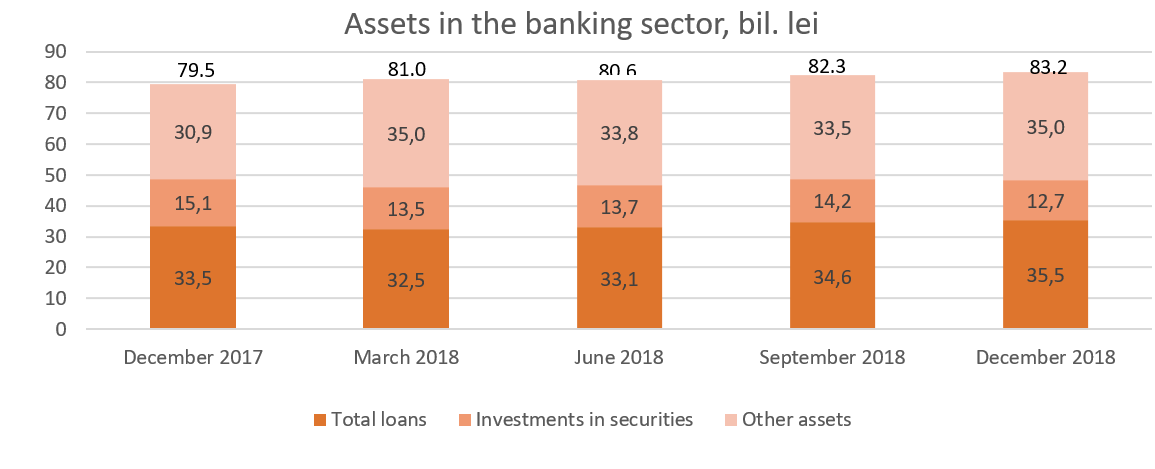

The total assets amounted to MDL 83.2 billion, increased by 4.6% in 2018 (MDL 3.7 billion ).

As of 31.12.2018, the balance of the gross loan portfolio accounted for 42.6% of the total assets or 35.5 billion, increasing by 5.9% (MDL 2.0 billion ) during 2018. At the same time, the volume of new loans granted in 2018 increased by 17.8%, compared to the same period of the previous year.

Aditionally, starting from March 2018, a monthly increase of the loan portfolio has been recorded. The highest increase in 2018 was in consumer loans and real estate loans. One of the factors that triggered this increase was the decrease of the interest rate. The National Bank of Moldova encourages banks to make more effort in financing the real economy..

The investments in securities (certificates of the National Bank and State securities) recorded a share of 15.3% of the total assets, which represents 3.7% less compared to the end of 2017.

The rest of assets, which amount to 42.1%, are held by banks in the accounts opened with the National Bank, other banks, in cash, etc.

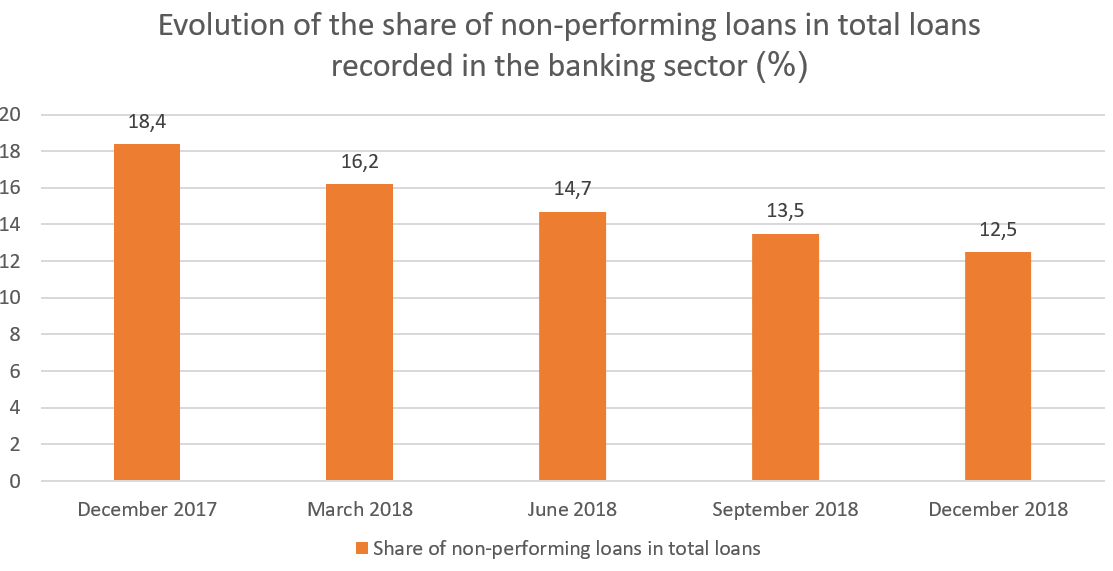

During the refered period, the share of non-performing loans (substandard, doubtful and compromised) in the total loan portfolio has decreased by 5.8% compared to the end of 2017, and represented 12.5% as of 31.12.2018. This share diminished at almost all banks with the aforementioned indicator varying from 4.9% to 31.2% from bank to bank. The progress recorded in reducing the share of non-performing loans in the total loan portfolio happened as a result of the measures taken by banks in elaborating and implementing own strategies for diminishing the volume of non-performing loans, among which the sale of the collaterals, collaboration with real estate companies in order to identify potential buyers for the collaterals, etc.

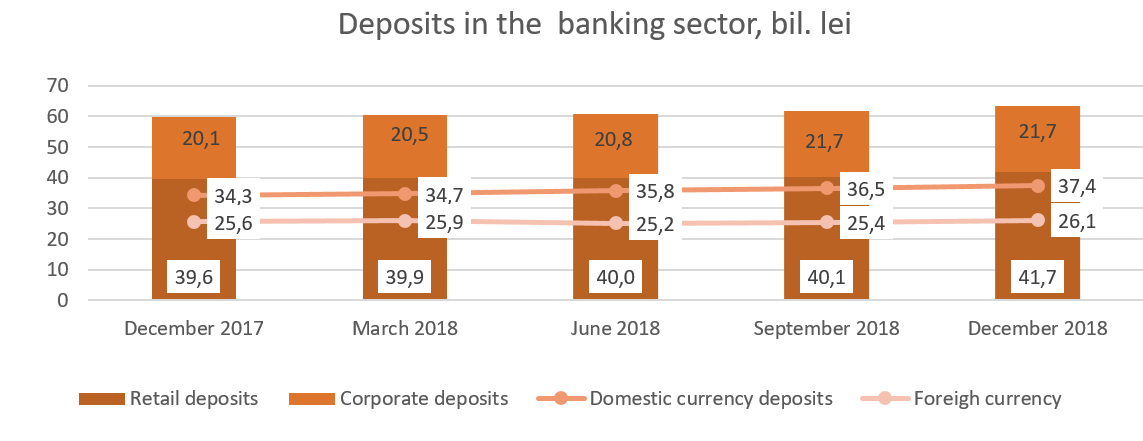

At the same time, the trend of increasing the deposits continued. According to the prudential reports, they increased by 6.0% in the reference period and amounted to MDL 63.5 billion (the deposits of individuals constituted 65.7% of the total deposits, the deposits of legal entities - 34.2%, and the deposits of banks - 0.1%). The increase in the deposits was largely caused by the increase in deposits of individuals by 2.1 billion lei (5.2%) and the deposits of legal entities, which increased by MDL 1.6 billion (7.9%).

Out of the total of deposits, 58.9% represented the deposits in national currency, that increased by MDL 3.1 billion (9.0%) amounting to MDL 37.4 billion as of 31.12.2018. The foreign currency deposits accounted for 41.1% of the total deposits, that increased by 473.7 million lei (1.8%) during2018, amountin to MDL 26.1 billion. In this way, MDL 1.2 billion foreign currency deposits were attracted, while the exchange rate fluctuation represented MDL (-739.4) million.

Income and rentability

As of 31.12.2018, the profit of the banking system represented MDL 1.6 billion, which denotes an increase of 7.0% (MDL 107.0 million), compared to the same period of the previous year.

Total revenues amounted to MDL 6.9 billion, out of which 62.1% (MDL 4.3 billion) represented interest rate revenues, and non-interest revenues - 37.9% (MDL 2.6 billion). Concomitantly, the total volume of expenditures constituted MDL 5.3 billion, including the expenditures with the interest – 27.5% of the total (MDL 1.5 billion), while the non-interest expenditures – 72.5% of the total (MDL 3.8 billion ).

The increase of the profit resulted from the increase in the non-interest revenues by 2.7% or by MDL 69.9 million, following the growth of revenues from fees and commissions, exchange rates differences, etc. Asignificant shares in the non-interest revenues is represented by the revenues from fees and commissions – 63.2%, revenues from exchange rates differences – 32.5% (revenues from currency trading and reevaluation), other operating revenues – 4.2%.

At the same time, the non-interest expenditures decreased by 1.4% or by MDL 52.5 million, following the decrease of assets depreciation due to the improvements in the quality of loan portfolio.

The expenditures with interests decreased by 21.7% or by MDL 403.1 million, as a result of the diminishing average interest rate for deposits. At the same time, the interest rate revenues decreased by 8.9% or MDL 418.5 million, as a result of the decrease in the interest rate for loans.

As of 31.12.2018, the return on assets and capital constituted 2.1% and 11.6% respectively, each with a 0.2% increase, compared to the end of the previous year.

Compliance with prudential requirements

The banks continue to have high liquidity indicators. Therefore, the value of the long-term liquidity indicator (principle I of liquidity) amounted to 0.7 (limit ≤1), increasing by 0.1 as compared to the end of 2017. The current liquidity of the banking sector (principle II of liquidity) diminished insignificantly and constituted 54.6% (limit ≥20%), more than half of the assets of the banking sector being concentrated in liquid assets. It has to be mentione that the largest share in the liquid assets belongs to the NBM deposits – 43.3%, liquid securities – 27.9% and net interbank money – 17.5%. In 2018, the share of NBM deposits increased significantly by 7.2%, following the requirement to keep the required reserves due to the increase of funds attracted by the banks and the increase of the required reserve ratio by 2.5% and share of cash – by 2.1%. At the same time, the share of liquid securities decreased by 6.4% and the share of interbank money – by 2.8%.

Principle III of liquidity, which represents the ratio between the adjusted effective liquidity and the necessary liquidity on each maturity band, that shall not be less than 1 per each maturity band, was respected by all banks.

On 30 July 2018, the new Basel III regulations came into force (based on the European CRD IV / CRR framework). The new regulations set the size of capital buffers, which if necessary, shall diminish the impact of systemic crises on banks capital.

Therefore, according to the reports presented by banks on 31.12.2018, the total own funds rate in the banking sector constituted 26.5%. At the same time, as of 31.12.2017, the risk-weighted capital adequacy ratio amounted to 31.3%. The transition to Basel III had a 5% impact, which is within the limits of the calculations conducted previously by the NBM. The regulated limit is respected by each bank and varies between 21.0% and 62.2%

As of 31.12.2018, the total own funds constituted MDL 10.8 million and recorded an increase of 2.3% (MDL 239.9 million) duringthe year. The increase in own funds was determined by the inclusion of intermediary profits obtained by banks before the entry into force of new regulations, in the calculation of own funds. At the same time, the adjustments of first level own funds decreased by MDL 473,6 million due to prudential filters, while the net intangible assets decreased by MDL 28,7 million . In 2018, the National Bank recommended to banks to direct their profits in the consolidation of capital, therefore, only two banks paid dividends in total amount of 354,9 million lei.

With respect to the Regulation on large exposures, it has to be mentioned that one bank continues to violate the prudential limit established by the NBM exceeding the required 15.0% of the total regulatory capital, however, the bank has a plan aimed to diminish the exposure, within the terms set in the plan.

At the same time, one bank violates the prudential limit of 30.0% of the indicator “Share of the sum of ten largest net credit debts in the total loan portfolio and the conditional commitments included in the ten largest debts, due to the considerable decrease of the loan portfolio. The bank submitted to the National Bank the strategy for diminishing of the above-mentioned indicator..

In 2018, following the entry into force of the Law no 202/2017 on banks’ activity, the National Bank of Moldova:

With respect to the regulatory documents of own funds and risk treatments, they were elaborated under the Directive no 2013/36/UE and Regulation no 575/2013, which implements the Basel III international regulatory framework.

The National Bank of Moldova continues to develop regulatory acts for the implementation of provisions of the Law on banks’ activity no. 202/2017.

Aligning the banking legislation of the Republic of Moldova with the international standards by improving banks quantitative and qualitative management mechanisms will contribute to the promotion of a safe and stable banking sector, to the increase of transparency, trust and attractiveness of the domestic banking sector for potential investors and creditors of banks, as well as for depositors, and to the development of new financial products and services.