Welcome to the official website of the National Bank of Moldova!

×

Do you have good eyesight and want to turn this tool off?

Welcome to the official website of the National Bank of Moldova!

You can choose one of the most popular reports from the list:

National Bank and the members of its decision-making bodies shall be independent in exercising the tasks conferred upon them by law, and shall neither seek nor take instructions from public authorities or from any other authority.

In order to ensure and maintain price stability over the medium term, the National Bank’s aim will be to keep inflation (measured by Consumer Price Index) at the level of 5.0 percent annually with a possible deviation of ± 1.5 percentage points, considered to be optimal for growth and development of Moldova's economy over the medium-term.

Financial stability is achieved by strengthening the resilience of the financial system, limiting the contagion effect and reducing the accumulation of systemic risks, thus contributing to the sustainability of the financial sector and economic growth.

National Bank shall have the exclusive right to issue on the territory of the Republic of Moldova banknotes and coins as legal tender, as well as commemorative and jubilee banknotes and coins as legal tender and for numismatic purposes.

National Bank is exclusively responsible for the licencing, supervision and regulation of financial institutions activity.

National Bank of Moldova acts as banker and fiscal agent of the State and shall receive from state bodies economic and financial information and documents, which are necessary for carrying out its tasks.

National Bank of Moldova is an autonomous public legal entity and is responsible to the Parliament.

National Bank shall inform the public on the monetary policy strategy on the results of the macroeconomic analysis, the evolution of the financial market and on statistics, including with regard to monetary supply, crediting, balance of payments and the state of the foreign exchange market.

National Bank of Moldova is responsable for the compilation of the balance of payments, international investment position and the statistics of the external debt of the Republic of Moldova.

Starting with 2018, the Moldovan banks, on their transition to Basel III standards, have begun to realign their activity with the new legislative framework by transposing the provisions of the CRD IV package; the transition will be implemented in stages and is to be completed by 2020. At the same time, the National Bank of Moldova (NBM) continues to promote the banking sector reforms, which focus on ensuring the transparency of shareholders in order to attract new investors meeting high quality requirements, on establishing solid corporate governance in the banking sector, on identifying bank related parties as well as on recording in timely manner the non-performing loans in the balance sheets of banks.

According to data as of March 31, 2018, in Moldova operated 11 banks licensed by the National Bank of Moldova, including 4 subsidiaries of foreign banks and financial groups.

During the first quarter of 2018, the banking sector’s assets have continued to grow, banks having recorded sufficient capital and risk-weighted capital adequacy, high liquidity and profitability. At the same time, the banking sector has maintained the downward trend of lending activity, although the volume of loans extended in the first quarter of 2018 has increased compared to the same period of the previous year. During the reference period, the share of non-performing loans in the loan portfolio has decreased, although still remains rather high, therefore the banks continue to make efforts to reduce the balance of non-performing loans.

In 2017, in connection with the constantly increasing risk associated with information technologies, the National Bank of Moldova has requested the banks to have an IT audit conducted by an external audit company. Currently, the NBM is reviewing the results of the completed external IT audit and, if required, will request banks to develop measures to address identified deficiencies.

Having identified the lack of transparency in the banks’ shareholders structure as well as the banks’ engagement in high-risk credit operations, the National Bank of Moldova, in accordance with the provisions of the Law on Financial Institutions, established, on 11.06.2015, a special supervision programme over the activity of three banks: C.B. "MOLDOVA-AGROINDBANK" S.A., C.B. "VICTORIABANK" S.A. and C.B. "Moldindconbank" S.A. Once with the implementation of changes in the local legislation, a special supervision was replaced by an intensive supervision, whereas the C.B. "Moldindconbank" S.A. was moved, on 20.10.2016, from an intensive supervision to the early intervention regime. The above-mentioned banks hold 65.7% of total banking sector assets.

At the same time, in order to prevent the banks from getting exposed to excessive risks, the activity of the banks placed under an intensive supervision and early intervention regime has been monitored by the National Bank on a daily basis. Thus, the financial situation of these banks, their transactions, the agenda of the meetings of the management bodies, etc. are being constantly examined.

After an international audit firm identified that the C.B. "MOLDOVA - AGROINDBANK" S.A., C.B. "VICTORIABANK" S.A. and C.B. ,, Moldindconbank" S.A. had been involved in transactions with their related parties, the Executive Board of the National Bank of Moldova, on 26 April 2018, took the final decision on the related party presumption criteria and requested the above-mentioned banks to prepare correction plans, which would ensure the adjustment of the banks’ risk exposures towards related parties to the established prudential limits and would improve the internal control procedures aiming to identify and monitor the banks’ related parties.

C.B. „VICTORIABANK” S.A.

In January 2018, some changes occurred in the shareholder structure of the C.B. "VICTORIABANK" S.A. Thus, on 16 January 2018, an auction took place on the regulated market of the Moldovan Stock Exchange, where the 39.2% stake was sold. As a result, Banca Transilvania, the second largest bank in Romania, became an investor of the Victoriabank through the Dutch company “VB Investment Holding B.V.” Following the transaction, “VB Investment Holding B.V.”, which on 24.05.2016 became a shareholder of the bank by acquiring 27.56% of the bank’s share capital, in partnership with Banca Transilvania from Romania and the European Bank for Reconstruction and Development, currently owns 66.77% of the bank's share capital, which follows to increase further up to 72.19% once the acquisition of additional 5.42% of the bank's shares is completed. Besides, changes have also occurred in the composition of the Administrative Board of the bank, two new members of the Board being approved by the NBM.

C.B. „MOLDOVA – AGROINDBANK” S.A.

The National Bank of Moldova has identified two groups of shareholders of the C.B. "MOLDOVA-AGROINDBANK" S.A., who acted in concert and in that manner have acquired a qualifying holding of 43.1% in the bank's share capital having received no prior written approval of the National Bank for such acquisition. As a result, the shares were to be alienated within the three months’ period. As the shares had not been alienated by the established deadline, they were cancelled, new shares being issued instead. Thus, two single packages of shares were put up for sale on the Stock Exchange of Moldova, to be sold by June 2017, the sale term, however, being extended several times. Following the modification of the legal framework related to the procedure of selling the shares held by persons who have not received prior approval of the NBM, the Board of the C.B. "Moldova-Agroindbank" has decided at its meeting held on 08.02.2018 to put up for sale from 14.02.2018 the above-mentioned shares on the regulated market of the Stock Exchange of Moldova (period of auction April 17, 2018 - April 30, 2018).

C.B. „Moldindconbank” S.A.

The C.B. "Moldindconbank" S.A. currently operates under the early intervention regime. It was established on October 20, 2016 after discovering that a group of persons, acting in concert, had acquired and was holding a qualifying holding of 63.89% of the bank's share capital without having received a prior written approval of the NBM for such acquisition, thus violating the provisions of the Law on Financial Institutions.

By the decision of 20.10.2016, the NBM appointed temporary administrators of the C.B. "Moldindconbank" S.A. At the beginning of this year, the Executive Board of the National Bank of Moldova decided to extend the mandates of the bank’s temporary administrators for a period of six months, starting with January 20, 2018.

The package of shares (63.89%), acquired by the group of persons acting in concert, was seized in a criminal case. Later, in October 2017, the custodians and the Registry company informed the bank about the lifting of the seizure. In January 2018, in accordance with the legal provisions, the Administrative Board of the C.B. "Moldindconbank" S.A. approved the decision on the cancellation of the package of shares and the issuance of a new package of shares representing 63.89% of the bank's share capital, to be put up for sale. In this context, in February, the bank signed a contract with an international audit firm to provide the evaluation of the sale price of the new stocks issued. Following the evaluation, on 13.04.2018, C.B. "Moldindconbank" S.A. adopted at its meeting of the bank's Administrative Board the decision on the initial sale price for the new shares issued by the bank. On 17.04.2018 the bank published on its website the information on the sale of 3,173,751 ordinary nominal shares of Class I, the terms of their sale, as well as the Investment Memorandum containing information related to the bank's activity and a description of the bank's financial situation over the last 3 years. Thus, the shares were put up for sale as a single package, available for a period of 3 months.

Based on the report data submitted by licensed banks, as of 31 March 2018, the situation in the banking sector was characterised by the following trends:

Assets and liabilities

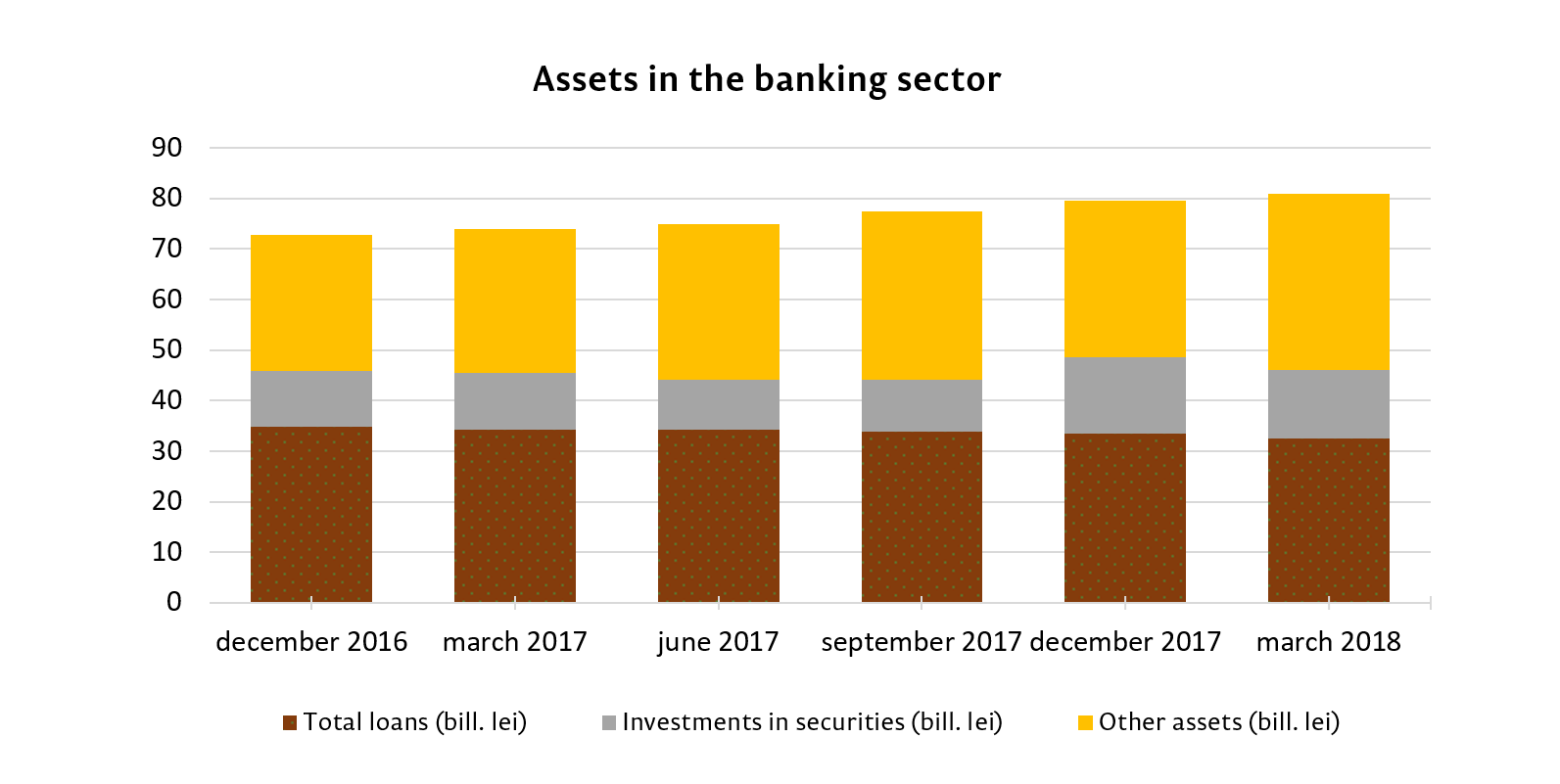

Total assets amounted to 81.0 billion lei, rising by 1.8% (1.4 billion lei) during the first quarter of 2018.

As of 31.03.2018, the balance of the gross loan portfolio accounted for 40.0% of total assets or 32.4 billion lei, having decreased by 3.3% (1.1 billion lei) during the first quarter of 2018. At the same time, against the background of the decrease in interest rates on loans, the volume of new loans extended in the first quarter of 2018 increased compared to the same period of the previous year, the growth amounting to 5.4%.

Investments in securities (certificates of the National Bank and government securities) accounted for 16.7% of total assets, having decreased by 2.3 pp. compared to the end of 2017.

The rest of the assets, accounting for 43.3%, are kept by banks in accounts opened with the National Bank, other banks, in cash, etc.

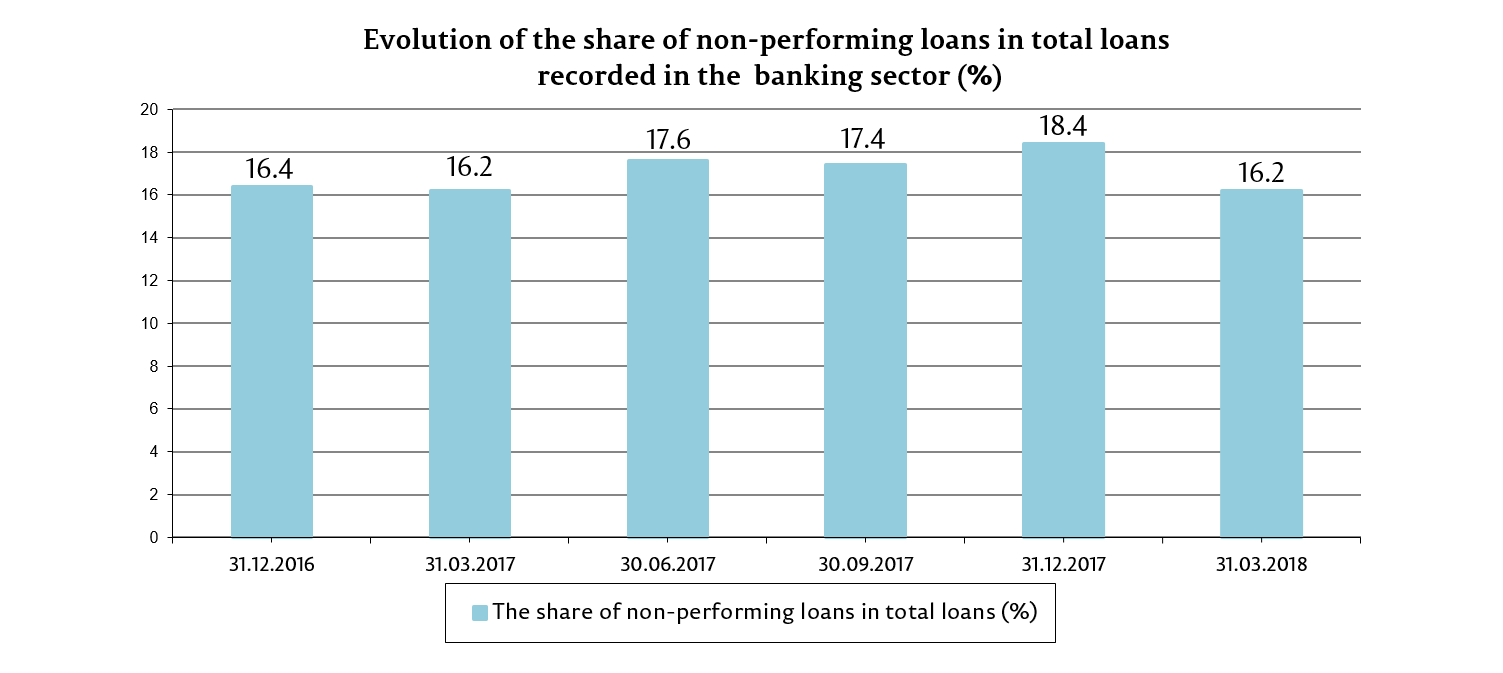

During the first quarter of 2018, the share of non-performing loans (substandard, doubtful and compromised) in total loans decreased by 2.2 pp. compared to the end of 2017, having recorded 16.2 percent as of 31 March 2018. The indicator varies across the banking sector, ranging from 3.8% to 34.9%.

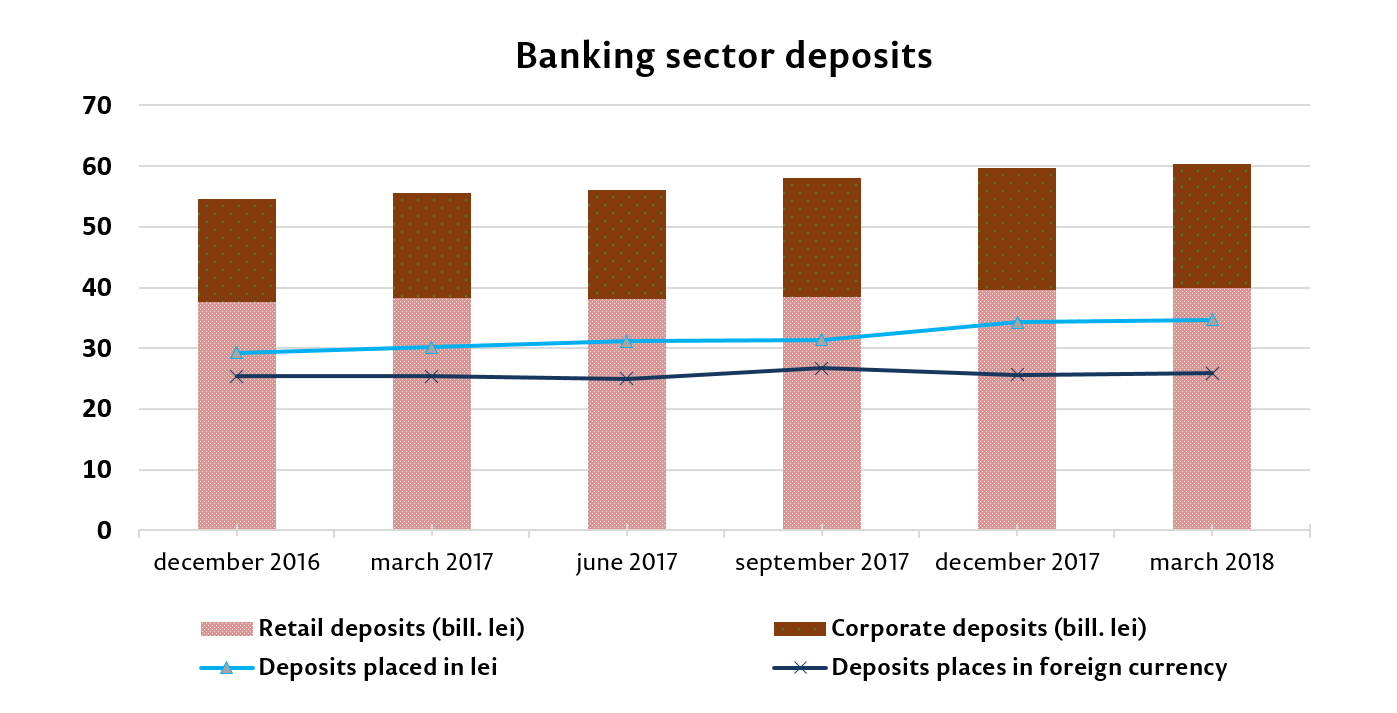

During the first quarter of 2018, the banking sector continued to record an upward trend in the balance of deposits. According to prudential reports, it increased by 1.1% in the reference period, amounting to 60.6 billion lei (retail deposits accounting for 65.9% of total deposits, corporate deposits - 33.8% and deposits of banks - 0.3%). The increase in corporate deposits by 389.2 million lei (1.9%) had the biggest impact on the growth of balance of deposits. The balance of retail deposits has also increased by 280.6 million lei (0.7%).

Of total deposits, deposits placed in MDL accounted for 57.3%, their balance having increased by 422.3 million lei (1.2%), amounting to 34.7 billion lei as of 31.03.2018. Deposits placed in foreign currency accounted for 42.7% of total deposits, their balance having increased by 258.5 million lei (1.0%), totalling 25.9 billion lei.

At the same time, in March 2018, the C.B. "EXIMBANK - Gruppo Veneto Banca" S.A. has changed its sole shareholder and has become part of the Intesa Sanpaolo Group. It should be mentioned that non-performing loans were excluded from the acquisition.

Compliance with prudential requirements

Banks continue to maintain high liquidity ratios. Thus, the value of the long-term liquidity indicator (1st liquidity principle) recorded 0.6 (the limit being set at ≤1), a level equal to the one of the end of 2017. The current sector liquidity (2nd liquidity principle) increased by 1.3 pp, recording 56.8 (the limit being set at ≥20%), meaning that more than a half of the banking sector's assets are concentrated in liquid assets. It should be mentioned that the largest share in total liquid assets is held by deposits placed with the NBM - 39.7%, these being followed by liquid securities - 29.4% and net interbank money - 20.5%. During the first quarter of 2018, the share of deposits placed with the NBM increased by 3.6% and the share of net interbank funds - by 0.2 pp. At the same time, the share of liquid securities decreased by 4.9 pp.

The 3d liquidity principle shows the ratio between the actual adjusted liquidity and the required liquidity for each maturity band, which must not be less than 1. It was determined that, following a change in its funding structure, one bank fails to comply with the prudential limit set for the 3 to 6 month maturity band and the 6 to 12 month maturity band.

The risk-weighted capital adequacy ratio for the banking sector recorded 33.2%, meaning that the limit set for all banks (≥16%) was complied with. It varied across the sector ranging between 23.8% and 89.1%.

As of March 31, 2018, the Tier I capital amounted to 10.6 billion lei, having recorded a 5.4 percent increase (542.6 million lei) during the reference period. The increase of the Tier I capital was mainly determined by the profit obtained in the first quarter, amounting to 522.3 million lei. Also, the amount of calculated unreserved losses was decreased for contingent assets and liabilities by 275.0 million lei and for net intangible assets by 2.3 million lei. At the same time, the transition to IFRS 9 has had a negative impact over the capital, the decrease totalling 226.6 million lei.

Regarding the Regulation on large exposures, it should be noted that one bank still does not comply with the prudential limit of 15 percent of the total regulatory capital, set by the NBM. However, the bank has in place the exposure reduction plan and respects the set deadlines.

Also, there is one bank which breached the prudential limit of 30 percent set for the indicator “The share of the ten largest net debts on loans in the total portfolio of loans and contingent liabilities included in the ten largest debts as a result of the considerable decrease in the loan portfolio of a bank” (loans assignments). The bank will develop a plan to address this issue, the plan following to be submitted to the NBM for examination.

Revenues and profits

As of March 31, 2018, the profits amounted to 522.3 million lei, having increased by 4.5% compared to the same period of the previous year.

Total revenues amounted to 1.8 billion lei, of which interest revenues accounted for 60.9% (lei 1.1 billion), and non-interest revenues recorded 39.1% (692.7 million lei). At the same time, total expenditures amounted to 1.3 billion lei, including interest expenses - 31.7% (396.8 million lei) and non-interest expenses - 68.3% (854.2 million lei).

The increase in profits was determined by the increase of non-interest revenues by 26.5% or by 145.1 million lei and by the decrease of interest expenses (deposit-related) by 23.7% or by 123.5 million lei. The largest shares in total non-interest revenues were held by revenues obtained from fees and commission - 45.1 percent, other operating revenues - 27.6 percent and by revenues resulting from foreign exchange differences - 27.2 percent (revenues from foreign currency trading and revaluation).

At the same time, non-interest expenses increased by 9.7% or 75.6 million lei. Interest revenues totalled 1.1 billion lei, having declined by 170.4 million lei, year-on-year, as a result of the decrease in interest rates and the reduction of the loan portfolio.

As of 31 March 2018, return on assets and return on capital accounted for 2.4% and 15.2%, respectively, having increased by 0.6 pp. and 4.2 pp., respectively, compared to the end of the previous year.

In the first quarter of 2018, after the enactment on January 1, 2018 of the Law on Banking Activity no. 202 of October 6, 2017, the National Bank of Moldova initiated public consultation regarding the 8 draft regulations focusing on the own funds requirements and the management of credit, market, operational and settlement / delivery risks in the context of own funds. Having duly examined the stakeholders' feedback, there were elaborated synthetic recommendations, based on which the final drafts of the Regulations were produced.

The elaboration of regulations was initiated under the Twinning project of the European Union aiming to strengthen the NBM’s capacity in the field of banking regulation and supervision, in cooperation with the Central Bank of the Netherlands and the National Bank of Romania in the context of the transposition of the Directive 2013/36/EU and the Regulation 575/2013, which served as instruments for the implementation of Basel III international regulatory framework in the European Union. At the first stage, the draft regulations promote new approaches to the calculation of own funds and the risk-weighted capital adequacy (which along with credit risk include other risks, such as operational, market, and other banking-related risks).

Draft regulatory acts, promulgated in the first stage, will provide for a transition period to ensure a proper alignment of banks' activity with the provisions of the new regulatory framework.

Besides, the National Bank of Moldova has initiated the process of the decision-making transparency by having developed the Guidelines on the submission by banks of COREP reports for supervisory purposes, having set out requirements on the format and the manner of reporting on the regulatory acts elaborated at the first stage of transposing the European prudential framework.

The National Bank of Moldova continues to elaborate regulatory acts that will ensure the application of the provisions of the Law on Banking Activity no. 202 of 6 October 2017 and the alignment of the legislation with the European standards (Basel III).

The alignment of the banking legislation of the Republic of Moldova with international standards by means of improving the quantitative and qualitative mechanisms of banks’ management will contribute to the promotion of a secure and stable banking sector, to increased transparency, trust and attractiveness of the domestic banking sector for potential investors and creditors of banks, as well as for depositors, etc. The new framework favours the development of new financial products and services by creating a stable financial environment that ensures a financial soundness of banks and of the entire system.