Welcome to the official website of the National Bank of Moldova!

×

Do you have good eyesight and want to turn this tool off?

Welcome to the official website of the National Bank of Moldova!

You can choose one of the most popular reports from the list:

National Bank and the members of its decision-making bodies shall be independent in exercising the tasks conferred upon them by law, and shall neither seek nor take instructions from public authorities or from any other authority.

In order to ensure and maintain price stability over the medium term, the National Bank’s aim will be to keep inflation (measured by Consumer Price Index) at the level of 5.0 percent annually with a possible deviation of ± 1.5 percentage points, considered to be optimal for growth and development of Moldova's economy over the medium-term.

Financial stability is achieved by strengthening the resilience of the financial system, limiting the contagion effect and reducing the accumulation of systemic risks, thus contributing to the sustainability of the financial sector and economic growth.

National Bank shall have the exclusive right to issue on the territory of the Republic of Moldova banknotes and coins as legal tender, as well as commemorative and jubilee banknotes and coins as legal tender and for numismatic purposes.

National Bank is exclusively responsible for the licencing, supervision and regulation of financial institutions activity.

National Bank of Moldova acts as banker and fiscal agent of the State and shall receive from state bodies economic and financial information and documents, which are necessary for carrying out its tasks.

National Bank of Moldova is an autonomous public legal entity and is responsible to the Parliament.

National Bank shall inform the public on the monetary policy strategy on the results of the macroeconomic analysis, the evolution of the financial market and on statistics, including with regard to monetary supply, crediting, balance of payments and the state of the foreign exchange market.

National Bank of Moldova is responsable for the compilation of the balance of payments, international investment position and the statistics of the external debt of the Republic of Moldova.

During the year 2022, the banking sector successfully faced external challenges. The National Bank of Moldova (NBM) continued the process of prudential supervision of banks, following the legal requirements, in order to ensure the stability and viability of the banking system.

The financial situation of the banking sector, according to data submitted by banks, is characterised by growth in assets, loans, own funds, own funds ratio, deposits of natural and legal persons and deposits of banks. The profit for the year compared to the same period of the previous year increased mainly as a result of higher interest and non-interest income.

At the same time, there was an increase in the absolute value of outstanding loans, non-performing loans and, as a result, a worsening of loan portfolio quality indicators compared to the end of the previous year.

As of December 31, 2022 11 banks licensed by the National Bank of Moldova were active in the Republic of Moldova. One bank was supervised under the early intervention regime applied on 11.01.2019. During the year, AS "IuteCredit Europe" acquired qualified holding in the amount reaching and exceeding the level of 50.0 percent of the share capital of B.C. "ENERGBANK" S.A., becoming the majority shareholder of the bank. Following the changes registered in the bank’s shareholding structure, the governing body was completed. Subsequently, in January 2023, the Executive Board of the National Bank of Moldova decided, by unanimous vote, to lift the early intervention regime at B.C. "ENERGBANK" S.A.

As of December 31, 2022, the situation in the banking sector, reflected by the reports submitted by banks, registered the following trends:

Assets and liabilities

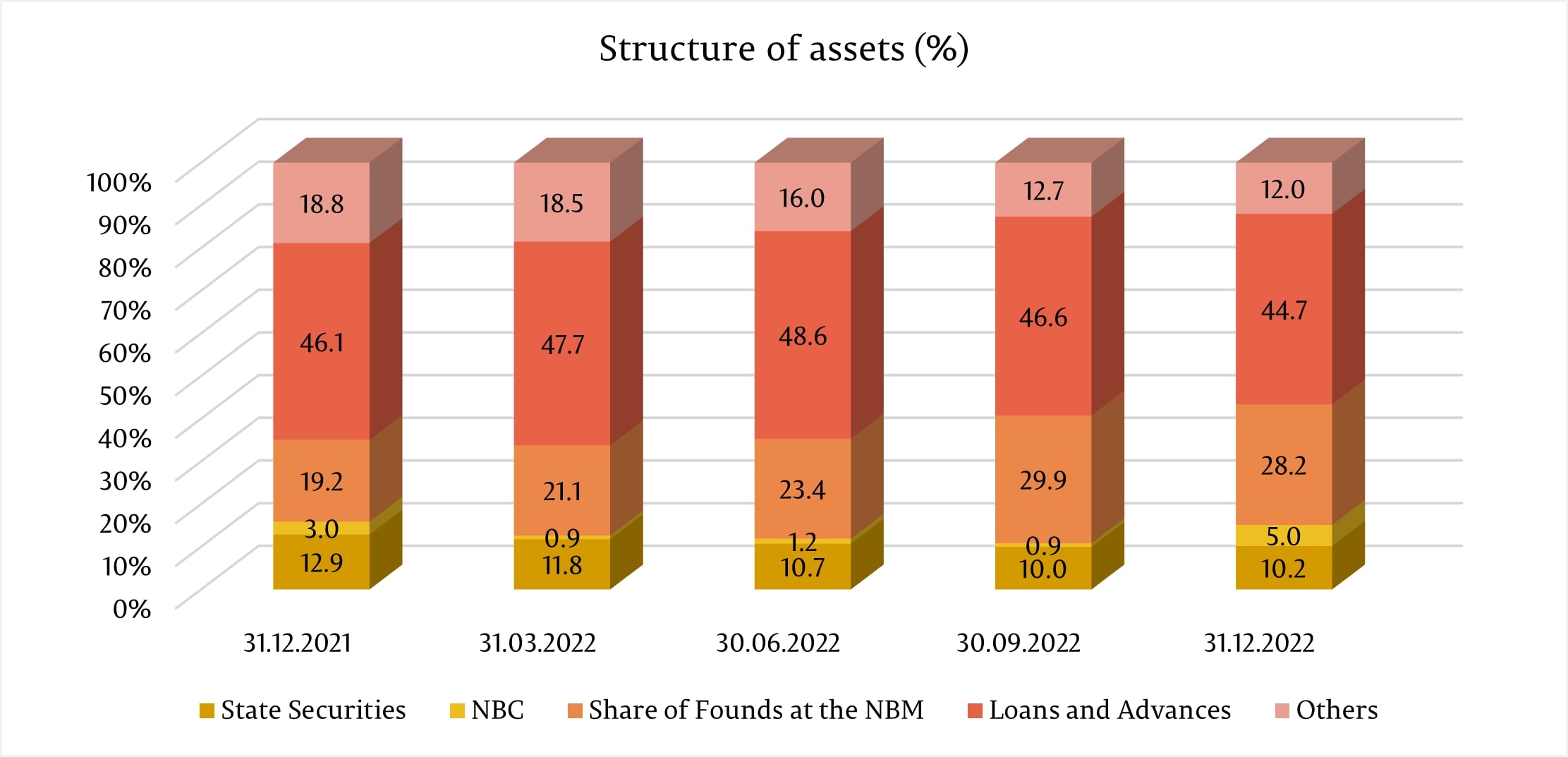

Total assets amounted to MDL 131.4 billion, increasing by 10.9% (MDL 12.9 billion) during the year 2022.

The largest share in total assets went to "Loans and advances at amortized cost", which amounted to 44.7% (MDL 58.7 billion), decreasing by 1.4 percentage points (pp) compared to the end of the previous year.

The share of funds at the NBM was 28.2% (MDL 37.1 billion), increasing by 9.0 pp, and the share of banks' investments in state securities and National Bank certificates accounted for 15.2% (MDL 19.9 billion), decreasing by 0.7 pp. The rest of the assets, which account for 12.0% (MDL 15.7 billion), are kept by banks in other banks, in cash, tangible fixed assets, intangible fixed assets, etc. Their share decreased by 6.8 pp compared to the end of the year 2021.

The gross (prudential) balance of loans accounted for 46.9% of total assets or MDL 61.6 billion, increasing during the period under review by 9.3% (MDL 5.3 billion).

In the year 2022, the largest increase in absolute value was recorded in loans granted to trade, by MDL 1 743.7 million (14.4%) up to MDL 13.9 billion, loans granted to the food industry - by MDL 978.9 million (26.6%) up to MDL 4.4 billion, loans granted for the purchase / construction of real estate - by MDL 865.7 million (7.6%) up to MDL 12.3 billion, loans granted to the non-banking financial sector - by MDL 665.0 million (36.9%) up to MDL 2.5 billion.

At the same time, the largest decrease in absolute value was recorded in consumer loans, by MDL 474.4 million (4.5%) up to MDL 10.0 billion.

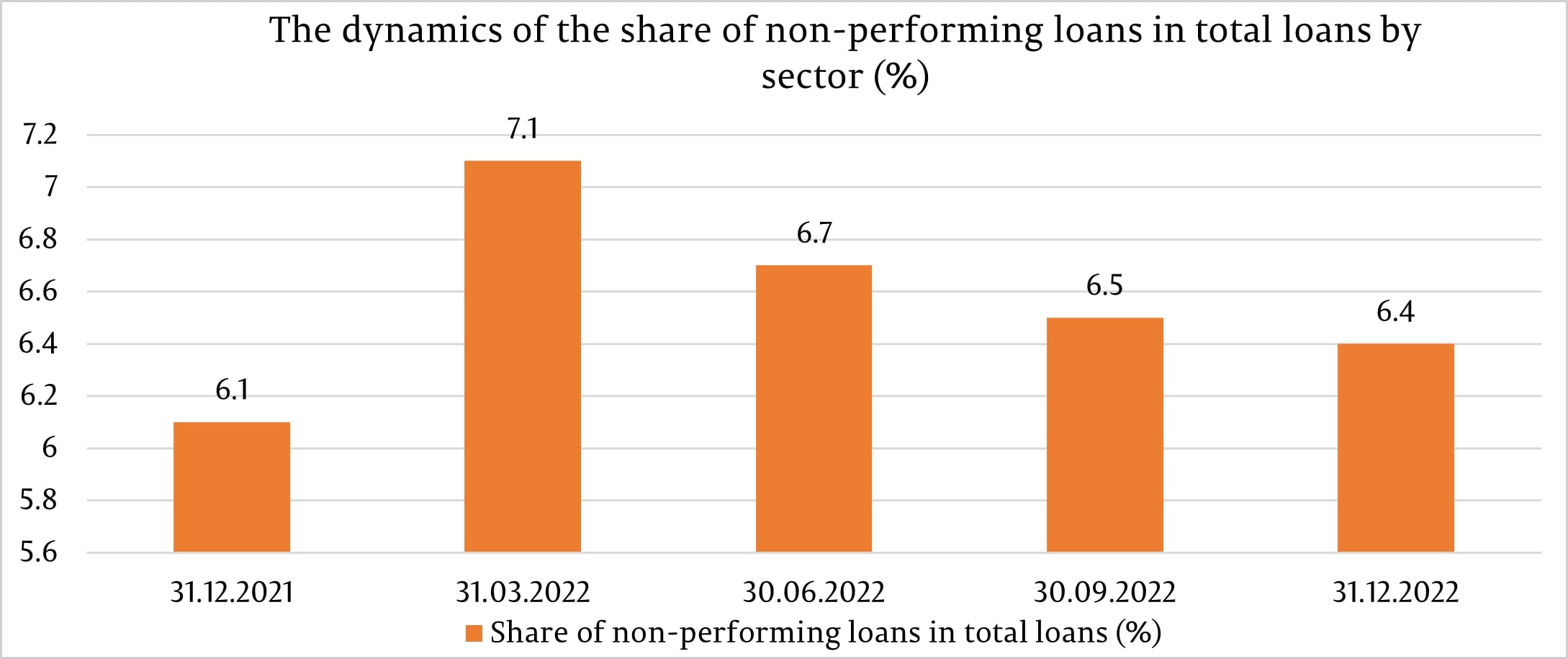

During the reference period, the share of non-performing loans (substandard, doubtful and compromised) in total loans increased by 0.3 pp, accounting for 6.4% on 31.12.2022, with the indicator ranging from 1.8% to 9.2%, depending on the bank.

At the same time, non-performing loans in absolute value increased by 14.7% (MDL 510.0 million) to MDL 4.0 billion.

During the period under review, the share of expired loans increased by 15.3% (MDL 266.7 million) up to MDL 2.0 billion. The share of expired loans in total loans was 3.3%, increasing by 0.2 pp as compared to 31.12.2021, ranging from 0.8% to 8.5%, depending on the bank.

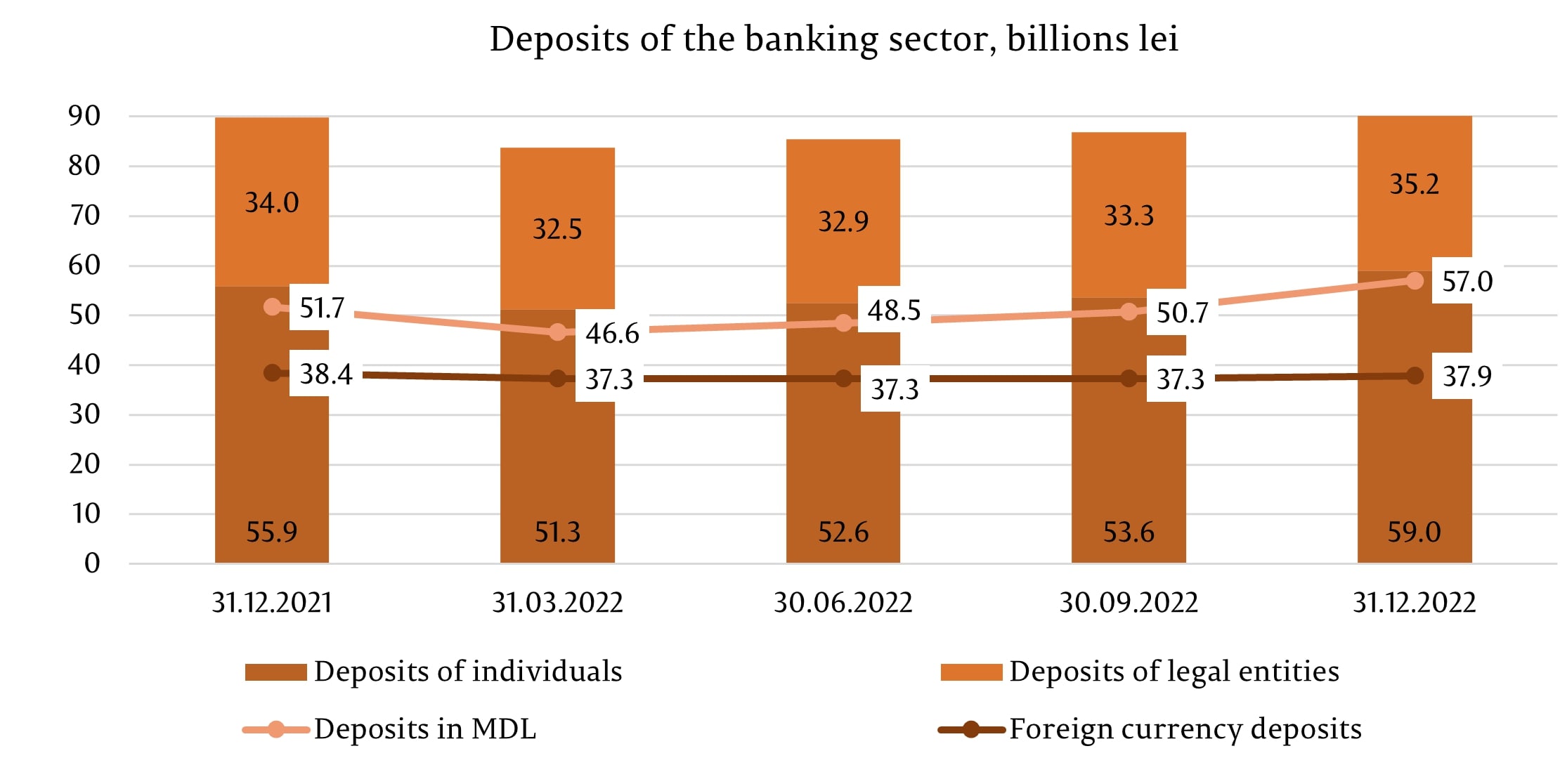

At the same time, during the reference period, the total balance of deposits increased by MDL 4.9 billion or by 5.4%, amounting up to MDL 95.0 billion (deposits of individuals accounted for 62.1% of total deposits, deposits of legal entities - 37.1% and deposits of banks - 0,8%), as a result of the increase in the balance of deposits of individuals by MDL 3.1 billion (5.5%) up to MDL 59.0 billion, deposits of legal entities by MDL 1.2 billion (3.4%) up to MDL 35.2 billion and deposits of banks by MDL 618.8 million (5.1 times) up to MDL 766.9 million.

In total deposits, 60.0% went to deposits in MDL, their balance increased by MDL 5.3 billion (10.3%) compared to the end of the previous year and amounted to MDL 57.0 billion on 31.12.2022. Foreign currency deposits accounted for 40.0% of total deposits, their balance decreased during the reference period by MDL 0.4 billion (1.1%), making up MDL 37.9 billion (withdrawal of foreign currency deposits - equivalent to MDL 1.7 billion, positive revaluation of foreign currency deposits – MDL 1.2 billion).

Revenues and profitability

As of December 31, 2022, the profit in the banking system amounted to 3.6 billion lei, increasing by 58.6% (MDL 1.3 billion) compared to the end of the previous year.

The increase in profit was due to the increase in interest income by MDL 4.5 billion (88.5%), income from exchange rate differences - by MDL 547.6 million (46.7%) and income from fees and commissions – by MDL 480.1 million (19.1%). At the same time, non-interest expenses (expenses related to fees and commissions, administrative expenses, provisions, impairment of financial and non-financial assets, etc.) increased by MDL 2.9 billion (53.8%) and interest expenses – by MDL 1.3 billion (103.3%).

Total revenues amounted to MDL 14.5 billion, increasing compared to the end of the previous year by MDL 5.6 billion (61.9%), of which interest income amounted to MDL 9.6 billion (66.2%) and non-interest income - MDL 4.9 billion (33.8%).

At the same time, total expenditure amounted to MDL 10.9 billion, increasing compared to the end of the previous year by MDL 4.2 billion (63.0%), of which interest expenditure were MDL 2.5 billion (23.2%) and non-interest expenditure - MDL 8.4 billion (76.8%).

On December 31, 2022, return on assets accounted for 2.9%, increasing by 0.9 pp, and return on capital accounted for 16.9%, increasing by 4.6 pp compared to the end of the previous year.

Compliance with prudential requirements

During 2022, banks continued to maintain liquidity indicators at a high level, above regulated limits.

Thus, the value of the long-term liquidity indicator (liquidity principle I) was 0.67 (limit ≤1), ranging from 0.33 to 0.80, depending on the bank, and decreasing insignificantly by 0.07 compared to the end of the year 2021.

Liquidity Principle III, which is the ratio of adjusted effective liquidity to required liquidity on each maturity band and which should not be less than 1 on each maturity band, has also been complied with by all banks, ranging from 1.58 on the maturity band up to one month inclusive up to 182.33 on the maturity band between one month and three months inclusive.

The liquidity coverage ratio by sector amounted to 267.9% (limit ≥ 80% - from 1 January 2022 to 1 January 2023), ranging from 182.8% to 571.1%, decreasing by 90.4 pp compared to the end of the previous year.

According to the reports presented by the banks as of 31.12.2022, the total own funds ratio in the banking sector registered a value of 29.5%, increasing by 3.6 pp compared to the end of the previous year, ranging from 22.3% to 61.9%. All banks met the indicator "Total own funds ratio" (≥10%).

All banks also complied with the "Total Own Funds Ratio" indicator requirement, considering capital buffers.

As of December 31, 2022, total own funds amounted to MDL 18.4 billion and registered an increase of 21.2% (MDL 3.2 billion). The increase in own funds was mainly determined by the banks’ reflection of eligible profits after general meetings of shareholders and after obtaining the NBM's permission to include the profits made in 2022 in its own funds.

As of December 31, 2022, the banks complied with the prudential indicators regarding large exposures and exposures to their affiliates.

During the year 2022, in order to apply the provisions of Law No. 202/2017 on the activity of banks, the National Bank of Moldova, through Decision of the Executive Board of the NBM No. 16/2022, amended the following acts:

These amendments were made in order to bring certain NBM regulations in line with the provisions of Regulation No. 101/2020 on Consolidated Supervision of Banks, Regulation No. 102/2020 on Treatment of Counterparty Credit Risk for Banks, Regulation No. 103/2020 on Treatment of Credit Valuation Adjustment Risk for Banks, and Regulation No. 274/2020 on Leverage for Banks, which transposed the relevant provisions of Regulation No 575/2013 of the European Parliament and of the Council of June 26, 2013.

Thus, the corresponding provisions of the delegated Regulation (EU) 2016/1075 with regard to regulatory technical standards specifying the content of recovery plans, resolution plans, and group resolution plans, the minimum criteria that the competent authority is to assess as regards recovery plans and group recovery plans, the conditions for group financial support, the requirements for independent valuers, the contractual recognition of write-down and conversion powers, the procedures, and contents of notification requirements and of notice of suspension and the operational functioning of resolution colleges were transposed.

At the same time, provisions were included that will enter into force starting from April 2023 regarding the aspects to be examined in the process of assessing independent thinking, namely behavioral skills as well as conflicts of interest among members of the governing body and members of the board of the bank, which would impede the person's ability to perform their duties independently and objectively. In this regard, it was established that the bank is obliged to inform the National Bank of Moldova, no later than 5 working days, of any information and any identified conflict of interest of which the bank has become aware that may affect the suitability of the members of the governing body or that may have an impact on the independent thinking of a member of the governing body, including the mitigating measures taken.

At the same time, in order to avoid excessive risk-taking in lending, the requirements for banks' credit risk management policies have been adjusted. In addition, in order to avoid a cash flow mismatch in view of the establishment of repayment schedules with repayments only at maturity, those policies have been supplemented with requirements as to how banks should establish those schedules. At the same time, the obligation to notify the National Bank of Moldova, within one working day, on the violation of the threshold indicators and the decision of the governing body on the applied recovery actions or the reasoning in case it was decided that no recovery actions are necessary were included.

In addition, provisions were introduced in Regulation No 322/2018 in order to create the secondary regulatory framework for the management of the risk associated with excessive leverage, which is an integral part of the management framework of banks' activities.