Bine ați venit pe pagină oficială a Băncii Naționale a Moldovei!

×

Ai vederea bună și dorești să închizi acest instrument?

Bine ați venit pe pagină oficială a Băncii Naționale a Moldovei!

Cele mai populare rapoarte statistice:

Banca Naţională şi membrii organelor de conducere ale acesteia sunt independenţi în exercitarea atribuţiilor stabilite de lege şi nu pot solicita şi nici accepta instrucţiuni de la autorităţile publice sau de la orice altă autoritate.

Banca Naţională informează publicul despre evoluția inflației anuale, strategia de politică monetară,rezultatele analizei macroeconomice, evoluţiei pieţei financiare şi informaţia statistică, inclusiv privind masa monetară, acordarea creditelor, balanţa de plăţi şi situaţia pieţei valutare.

Pentru asigurarea şi menţinerea stabilităţii preţurilor pe termen mediu, Banca Naţională a Moldovei menţine inflaţia (măsurată prin indicele preţurilor de consum) la nivelul de 5.0 la sută anual cu o posibilă abatere de ± 1.5 puncte procentuale, fiind considerat nivelul optim pentru creşterea şi dezvoltarea economică a Republicii Moldova pe termen mediu.

Stabilitatea financiară se realizează prin consolidarea rezilienței sistemului financiar, limitarea efectului de contagiune și diminuarea acumulării de riscuri sistemice, contribuind, astfel, la sustenabilitatea sectorului financiar și creșterea economică.

Banca Naţională a Moldovei, are dreptul exclusiv de a emite pe teritoriul Republicii Moldova bancnote şi monede metalice ca mijloc de plată. BNM pune în circulaţie bancnote şi monede metalice, prin intermediul sistemului bancar.

Banca Naţională este unica instituţie care efectuează licenţierea, supravegherea şi reglementarea activităţii instituţiilor financiare.

Banca Națională supraveghează sistemul de plăţi în Republica Moldova şi promovează funcţionarea stabilă şi eficientă a sistemului automatizat de plăţi interbancare.

Banca Naţională este o persoană juridică publică autonomă şi este responsabilă faţă de Parlament.

BNM publică statistici privind masa monetară, sectorul bancar, balanța de plăți, situația pieței valutare, etc. pentru a asigura transparența în procesul de elaborare și adoptare a deciziilor BNM, a asigura continuitatea în comunicare și predictibilitatea BNM pe piață, pentru sporirea credibilității BNM în calitate de bancă centrală dar și pe piața financiar-bancară din Republica Moldova.

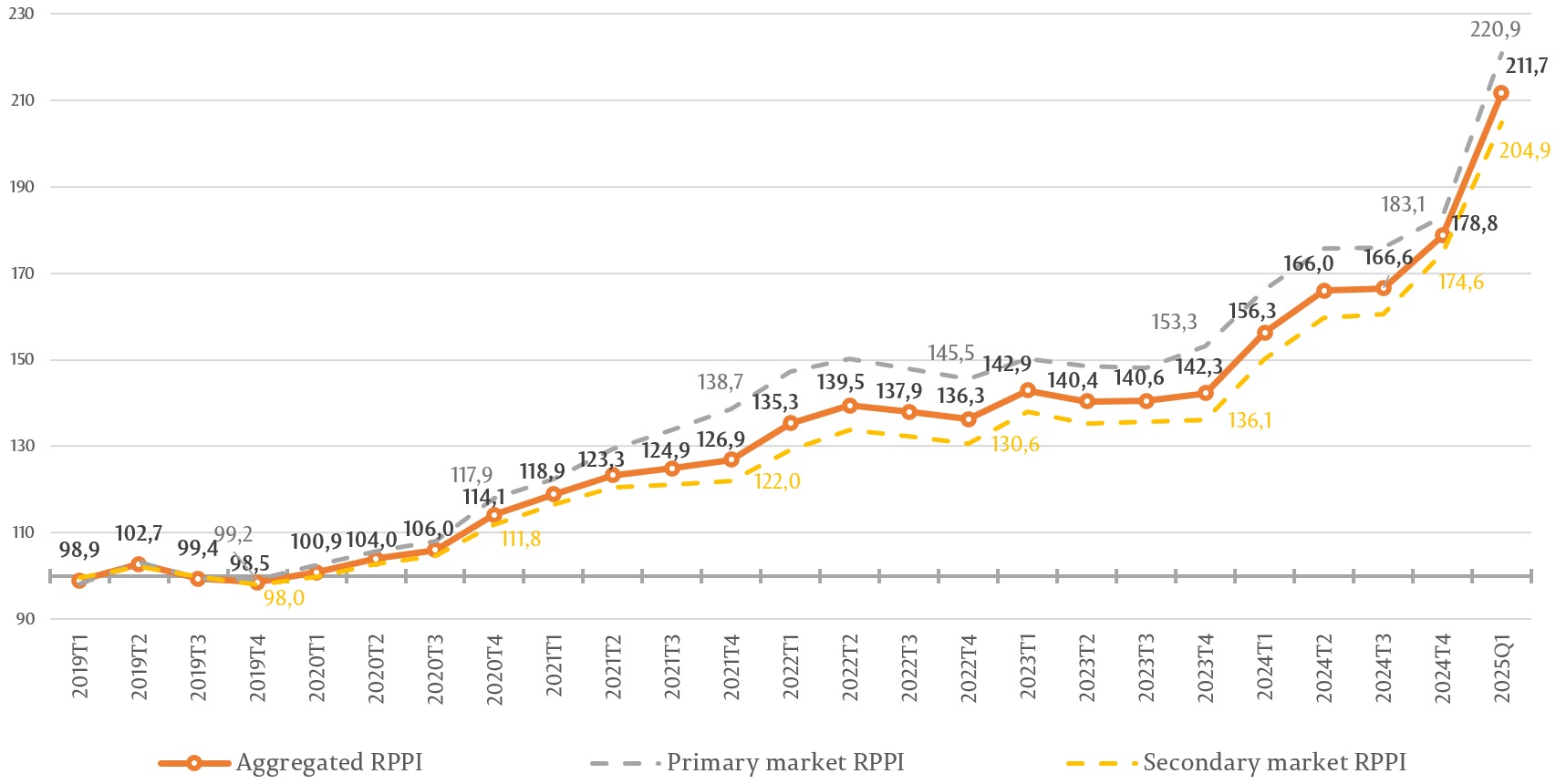

The close interconnection between the financial-banking environment and the real estate market is an important subject of studies conducted within the National Bank of Moldova, aimed at analysing the risks arising from possible shocks in the real estate market. One of the tools used by the NBM is the residential property price index (RPPI). The results at the end of the first quarter of 2025 show, for the first time, accelerated growth in residential real estate prices in both the primary and secondary segments, largely due to expanded access to financing under the government program "Prima Casă Plus", dedicated to families in the Republic of Moldova for better living conditions.

The aggregated RPPI index recorded a value of 211.7 percent, increasing by 18.4 percent compared to the fourth quarter of 2024 and by 35.4 percent compared to the first quarter of 2024.

The RPPI index for the offer price on the primary market registered a value of 220.9 percent, increasing by 20.6 percent compared to the fourth quarter of 2024 and by 32.9 percent compared to the first quarter of 2024.

The RPPI index for the offer price on the secondary market was 204.9 percent, increasing by 17.4 percent compared to the fourth quarter of 2024 and by 36.3 percent compared to the first quarter of 2024.

Figure 1. RPPI, % (average_2019=100)

Source: NBM

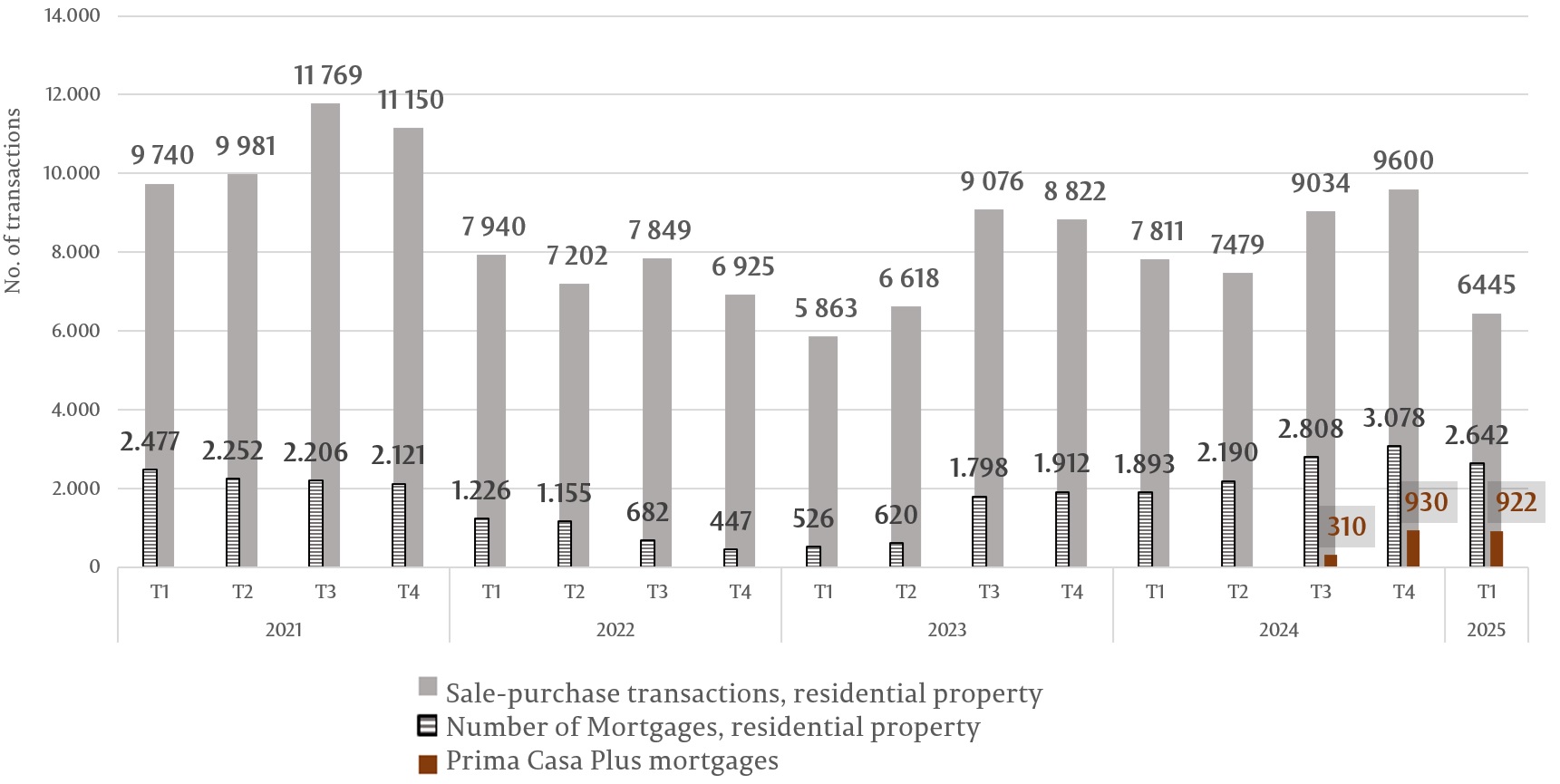

In parallel, the residential real estate market shows signs of transaction moderation (Figure 2), reflected in a reduction in the number of home sale and purchase transactions and a decrease in the number of properties purchased through mortgage loans.

Figure 2. The volume of residential real estate sale and purchase transactions in Chișinău

Source: Prepared by the NBM based on data from the IP Real Estate Cadastre

The decrease in the number of transactions shows that rising property prices have begun to inhibit demand, resulting in fewer potential buyers, given these prices. The share of transactions financed by mortgage loans increased during the analysed period, with mortgages remaining an important source of demand in the real estate market. At the end of the fourth quarter of 2024, the share of sale and purchase transactions financed through mortgages stood at 32.1%, but by the end of the first quarter of 2025, this indicator reached 41.0% (an increase of 8.9 p.p.), due to a significant decrease in the number of transactions during the first quarter of 2025 compared to the previous quarter (-32.9%).

This indicates a reduction in the population's ability to purchase from their own funds and an increasing reliance on banking solutions. The attractiveness of mortgage financing can also be explained by the "Prima Casă Plus" program, which has expanded lending capacity by increasing the financing amount and the possibility of financing the entire value of the purchased home. Since its launch in the third quarter of 2024, the number of mortgage loans granted under the program per quarter has increased from 310 loans during the third quarter of 2024 to 922 loans during the first quarter of 2025. This increase consolidated the share of these loans in the total number of mortgage contracts registered per quarter as follows: Q3 2024 – 11.0%, Q4 2024 – 30.2% and Q1 2025 – 34.9%. Thus, the increase in the share of loans granted through the "Prima Casă Plus" program could lead to the convergence of the population's entry point1 into the real estate market towards the amount financed per contract under the program (2.5 million MDL).

This level can be evaluated in comparison with the median offer prices considered for the RPPI, as it may represent a reference point towards which convergence could be anticipated in the medium term. In particular, during the first quarter of 2025, the median price for real estate in Chișinău increased from around EUR 89,000 to EUR 104,500, in line with the RPPI evolution mentioned above. Under the current circumstances, an increase in price levels can be anticipated until the median observed on the Chisinau market converges with the EUR equivalent of MDL 2.5 million (approximately EUR 127,800). As a result of median convergence, there could be a stagnation in the number of sale and purchase transactions due to a decline in the purchasing capacity of households eligible for financing services to acquire real estate, as well as a shift of trading activity to regions other than Chișinău (which would require recalibration of the RPPI, since it is currently calculated based on data from Chișinău municipality).

At the same time, the NBM carries out continuous and proactive supervision of the banking system, closely monitoring institutions that, through their sound risk management practices, already contribute to financial stability. In this regard, the authority has a comprehensive set of macroprudential tools, ranging from capital buffers to sectoral and borrower-oriented exposure limits, designed to strengthen the resilience of the entire financial sector.

1. The entry point into the real estate market is the equilibrium price level for residential real estate that can be financed by most potential buyers.